Deleveraging in a political milieu: Asia’s elephant faces a pivotal year

Despite a number of challenging setbacks this year, India looks like it is now positioned to realize its potential and rightfully retain its title as ‘the world’s fastest growing major economy’ for the next few years.

To be sure, India is building from a low base. Home to roughly one-fifth of humanity, Asia’s ‘elephant’ (as compared to Asia’s ‘dragon’ - China) is trying to reform the informal segments of its economy and build solid governance frameworks that cut across its 29 states. As always, aligning incentives and interests is no easy task in the world’s largest democracy.

I. Rescuing the banks

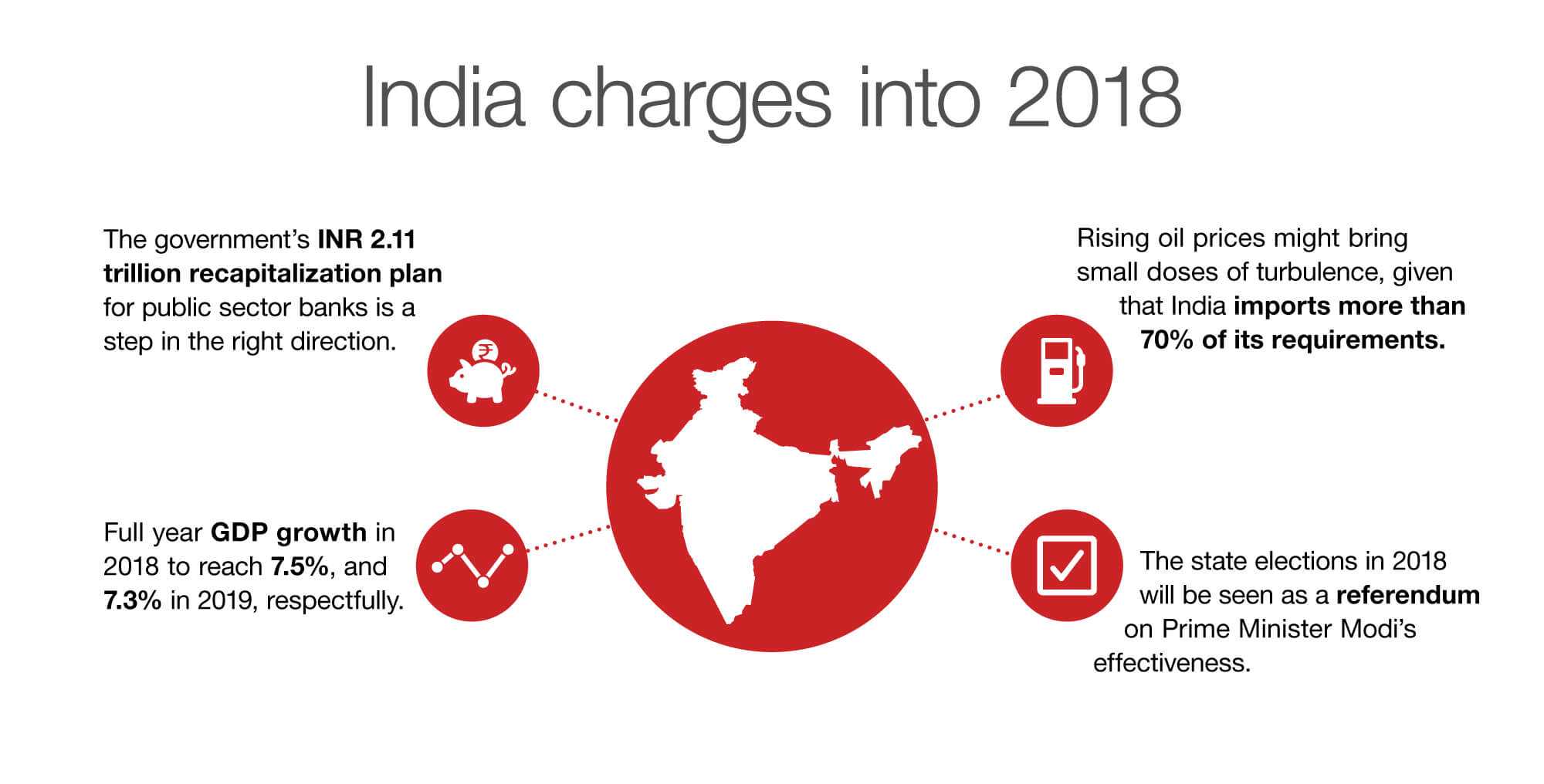

First, let’s look at the banks. India is largely a bank-financed economy, but the public-sector banks’ balance sheets aren’t healthy. On that note, the government’s comprehensive recapitalization plan for public sector banks – worth INR 2.11 trillion – is a step in the right direction and should accelerate deleveraging across the economy. In time, bad loans will be written off, improving the capex picture.

In the short term, it’s SMEs and other local drivers of growth that have been hit the hardest by the banks’ woes. However, private sector banks have better balance sheets offering some relief; and larger corporates have the resources to tap international markets for funds.

We’re still not out of the woods, but we’re getting there.

II. Goodbye informal economy?

It goes without saying the introduction of the GST was quite disruptive and painful in the short term. Many were not prepared; and its roll out was understandably challenging in a country as complex as India. But that turbulence is mostly behind us in 2018, and the economy will start to reap the benefits.

Moving forward we’ll see a level playing field, and India’s informal economy will slowly fade from the scene. This, in turn, will give the formal finance sector a more active role, and will also help to standardize governance and transparency across the economy, improving India’s risk profile.

In summary, we believe that India is transitioning towards greater formalization and higher tax compliance, and we expect S&P and Fitch to raise their outlook on sovereign ratings to ‘Positive’ from ‘Stable’ after H2 2018, and then upgrade to BBB from BBB- in 2019.

III. The hard numbers

At Nomura, we’re predicting full year GDP growth in 2018 to reach 7.5 percent, and 7.3 percent in 2019, respectfully. Inbound investment on the back of policy stabilization will be a key growth driver – supported by strong domestic consumption.

Six factors will support this growth:

1. the normalization of GST-related supply disruptions

2. the positive effects of bank recapitalization

3. a positive demonetization impulse

4. a positive fiscal impulse

5. a gradual pick up in investments led by improving corporate balance sheets

6. success of bankruptcy code-related asset transfers

IV. Black gold state elections

As always, there are a few pain points to consider. Rising oil prices might bring small doses of turbulence, given that India imports more than 70% of its requirements. That means every USD 10/bbl change in oil price adds 0.4% of GDP to the current account deficit. With rising demand, we expect the current account deficit to widen to 2% of GDP in 2018 – up from 1.5% in 2017.

As for politics, the big state elections in 2018 will be seen as a referendum on Prime Minister Modi’s effectiveness. All eyes will be watching to see if the BJP stumbles, and if populism will surge and potentially impact policy continuity and investor sentiment.

Despite these inevitable risks, however, at Nomura we’re expanding our footprint to seize the historic opportunities offered by Asia’s ‘elephant’ at this point in its development trajectory – whether that’s via growth in our ECM team or IPO underwriting business.

In this sense, time is our best asset: India is coming from a low base and that means its growth should be strong for decades to come.

For further insights to India, also read our Anchor Reports: Global EM 2018 Outlook: Enjoy the party but stay close to the door, and In an EM snapback, where do the risks lie?

Contributor

Prabhat Awasthi

Head of India

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.