Central Banks | 17 min video January 2020

Central Banks | 3 min read | February 2020

2020 US Outlook: Extending a long expansion

2020 Growth Expectations

Central Banks | 3 min read | February 2020

2020 Growth Expectations

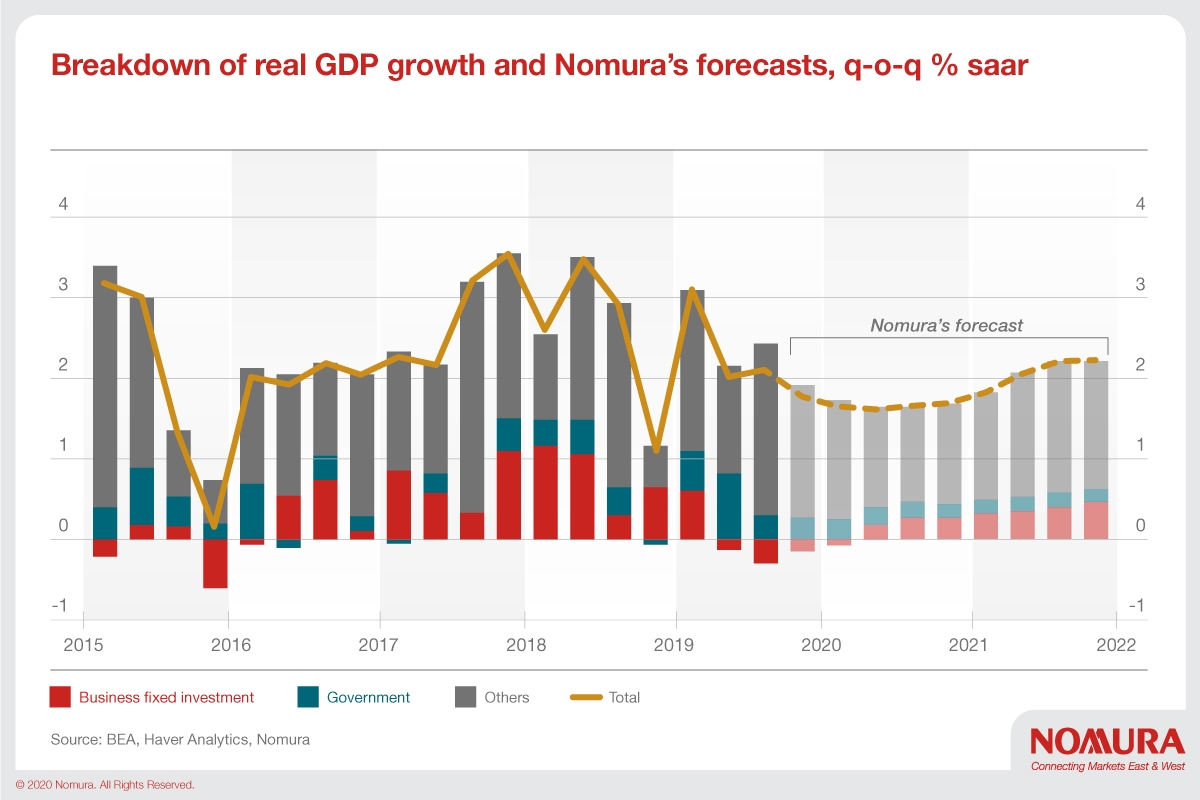

The US economic expansion is in its eleventh year. We expect growth to continue, but at a slower pace. The fiscal stimulus that boosted growth in 2018 is waning. Growth in US trading partners has slowed. Uncertainty surrounding economic policy and the business environment generally has increased and is depressing investment. Activity in the industrial side of the economy remains particularly weak.

With the US-China economic relationship in flux, the Trump administration still pursuing its broader, disruptive, trade policy, and a national election on the horizon, we think heightened uncertainty will persist in 2020. This is one key to our outlook. We think businesses will remain cautious next year, and that will depress investment and overall growth. The current circumstances are highly unusual. It is possible that businesses will pull back more than we have assumed in our forecast. This basic analytic uncertainty is one of the biggest downside risks to our outlook.

However, we also see factors that will support growth next year. Consumer fundamentals remain strong. Inflation risk seems modest, and that has allowed the Fed to support the expansion with 75bp of easing over the past six months. Recent increases in corporate borrowing pose a risk in the next downturn, but we do not think corporate credit will be the trigger for the next recession. We see little likelihood that inflation will pick up to a degree that the Fed would find unwelcome. Following the unusual underperformance of inflation late in the cycle, and associated declines in inflation expectations, we think the Fed will want to foster a period of “reflation.” This benign outlook for inflation, and the Fed’s response to it, is likely to keep interest rates, both short- and long-term, near current levels for some time.

Chief US Economist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Central Banks | 17 min video January 2020

Central Banks | 2 min read January 2020

Technology | 1 min read January 2020