The USMCA free trade agreement is now under formal review, with the US, Mexico, and Canada expected to meet on 1 July 2026 to determine whether to extend the pact. We view this joint review as the main macro event risk for Canada.

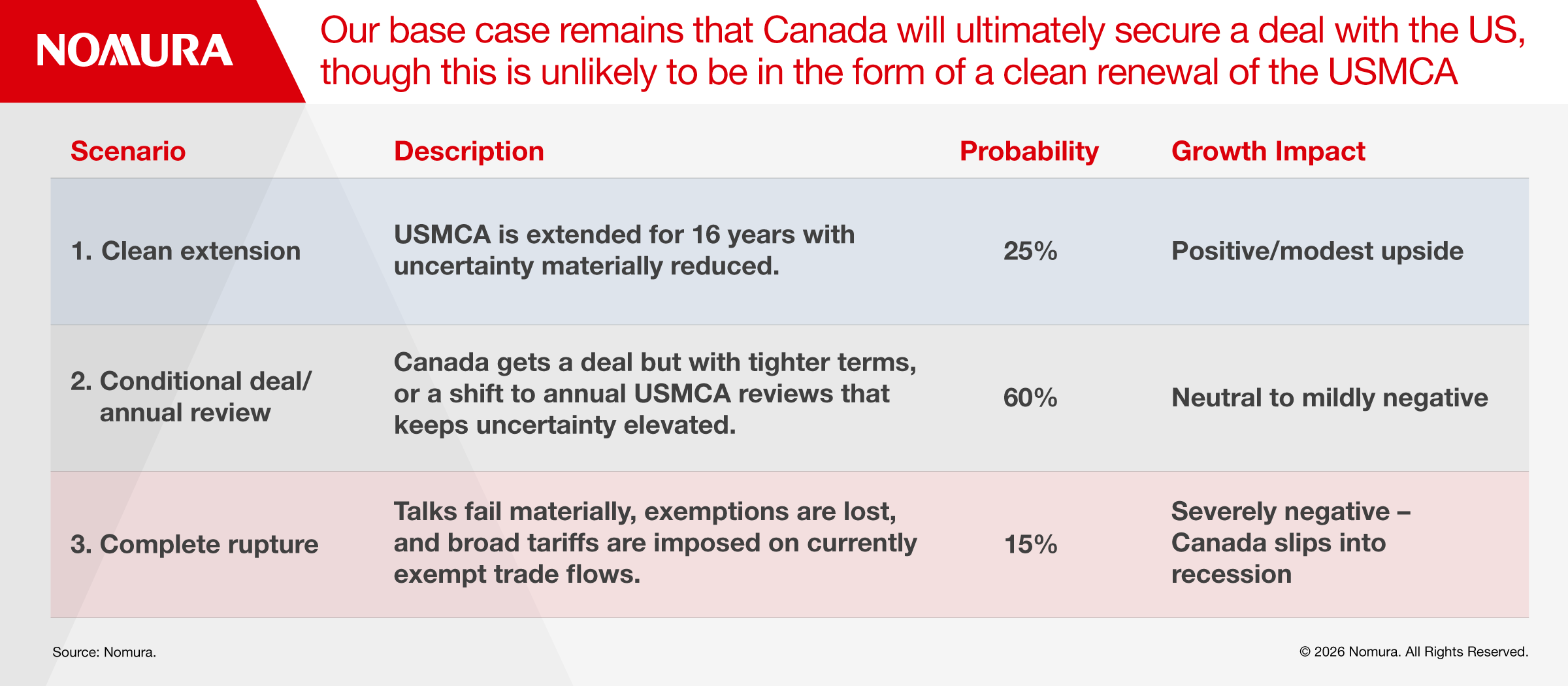

Broadly, there are three possible outcomes:

1. An extension: All three parties could agree to extend the pact for another 16 years, taking it through 2042, with the next formal review occurring in six years (2032). That would be the cleanest outcome and would materially reduce uncertainty.

2. A conditional deal: The agreement could remain in force without joint ratification of an extension, in which case the review process would be conducted annually. That would avoid an outright rupture, but it would institutionalize uncertainty and likely weigh on capex, hiring, and broader business sentiment.

3. Termination: Any member may choose to withdraw under Article 34.6, which allows termination with six months’ notice.

In our view, the most plausible outcome is a conditional agreement that preserves the core framework of USMCA and maintains North American trade integration, while leaving room for continued US leverage through tighter sectoral terms, narrower exemptions, and/or a framework with a more frequent review process.

Trade frictions not fading

The latest United States Trade Representative report on foreign trade barriers again highlighted Canadian dairy policies, agricultural supply management, pharmaceutical pricing practices, and customs-related barriers as notable non-tariff barriers. The US also reiterated concerns about Canada’s services-related measures, including the Online Streaming Act and Online News Act.

Separately, US President Donald Trump has threatened to impose additional duties on Canada in connection with any future deal involving China.

A breakdown in USMCA would severely affect Canada

One reason that a deal is more likely than not is because the alternative would be highly damaging for Canada, which remains deeply integrated with the US economy. The shock of a breakdown in North American trade integration would hit growth in different ways.

1. Lower exports to the US

Canadian exports to the US have edged lower since the start of 2025. The effective tariff rate on Canadian goods remains low because of USMCA exemptions, but elevated uncertainty and repeated tariff threats have weighed on trade volumes. Although Canada has sought to expand exports, especially energy, to non-US markets, those channels remain too small to offset the meaningful decline in US demand (Figure 1).

If USMCA were to falter and currently exempt trade flows were subjected to tariffs, we expect Canadian export volumes to the US would fall by between 5% and 10%.

2. Job losses

A sizable share of Canadian employment is linked, directly or indirectly, to exports to the US. If trade volumes weaken meaningfully, manufacturing and other trade-exposed sectors — which have faced headwinds lately — would likely see layoffs rise. In a serious downside trade scenario, we believe the unemployment rate could rise by 1 to 2 percentage points from the current 6.7%, reflecting both direct trade-related job losses and broader spillovers into domestic demand.

3. Weaker household consumption

Rising unemployment would weigh on household spending. Consumption was already tepid through 2025, and higher energy prices tied to the Iran war have also started to weigh on discretionary demand.

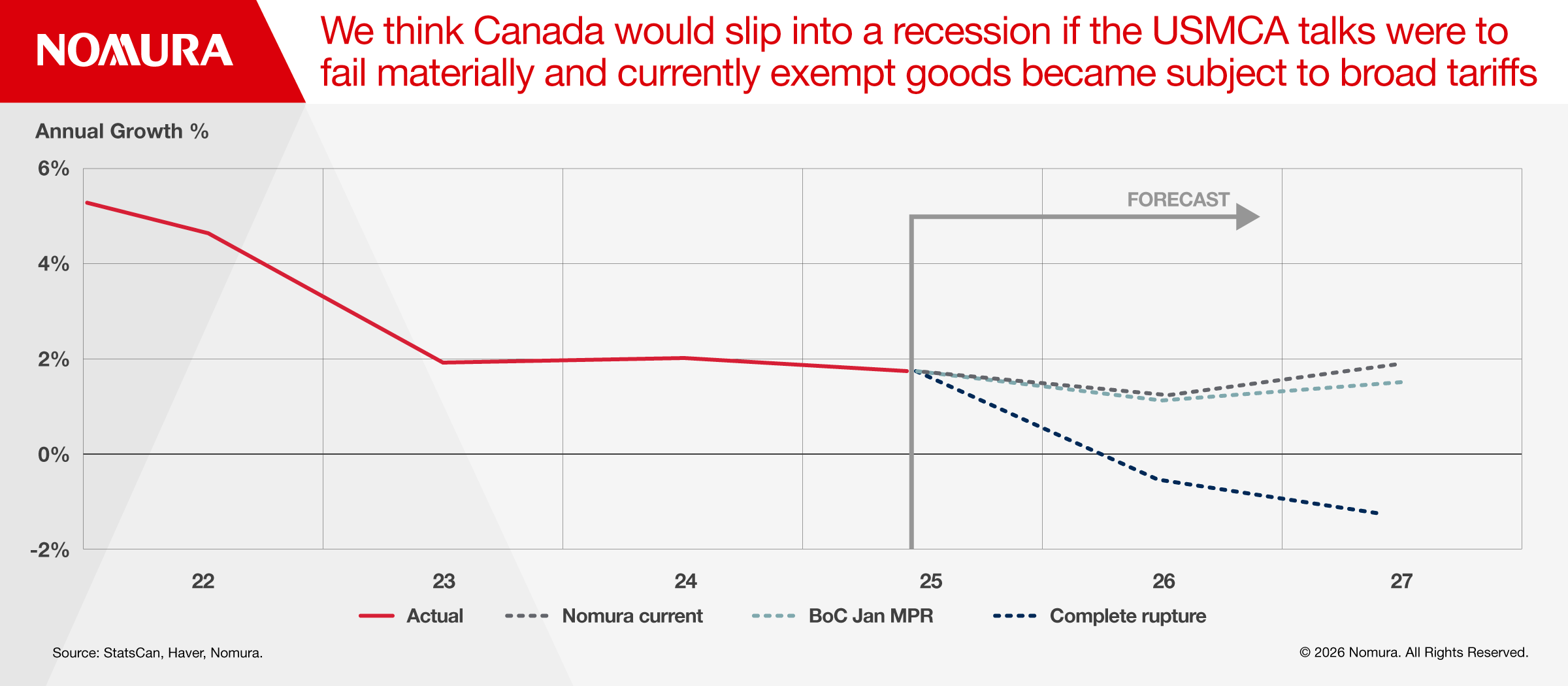

Considering these and other factors, we think Canada would slip into a recession if USMCA talks were to fail and goods that are currently exempt became subject to broad tariffs (Figure 2).

Efficacy of policy is limited

Another reason we believe a deal will be secured is that policy would have a limited ability to offset the damage.

A trade shock would put the Bank of Canada (BoC) in a difficult position. The BoC would likely ease materially if growth slowed sharply and downside inflation risks intensified. However, Bank of Canada Governor Tiff Macklem has stressed that monetary policy has limited ability to offset structural changes such as tariffs or impaired trade access.

Fiscal policy would therefore likely bear most of the adjustment burden. In a recession scenario, the federal government would need to provide interim support to businesses and households. While Canada’s fiscal position is not as concerning relative to its G10 peers on a net debt-to-GDP basis, the picture appears less reassuring when viewed through gross debt metrics, and fiscal dynamics in several provinces already look challenging.

Canada has reasons to grant some concessions given its current economic backdrop and the severe consequences that might ensue if trade relations falter.

The US also stands to gain from a deal

Given domestic affordability concerns, the US also has reason to meet Canada halfway. The majority of softwood lumber and metal imports come from Canada. Homebuilders have continued to flag concerns around rising homebuilding costs. Food prices could also rise sharply if the Trump administration decides to completely upend trade relations since Canada is the second-largest agricultural exporter to the US, with food imports from Canada roughly accounting for around 20% of total food imports.

Considering the upcoming midterms and the Trump administration’s broad focus on affordable housing policies, it is unlikely to escalate tensions.

Plausible solutions

Canada could improve its negotiating position by increasing defense spending and raising procurement from the US, as several other US partners have done. Participation in continental security initiatives such as the Golden Dome could also prove beneficial.

However, over the longer run, the more durable solution lies in addressing Canada’s impending structural problems. Greater trade diversification, investment in domestic infrastructure — particularly energy transportation — and reforms to reduce regulation and interprovincial barriers would do more to improve resilience and lift Canada’s growth potential.

To read our full report, click here.