Central Banks | 2 min read February 2019

Central Banks | 2 min read | July 2019

Central Banks | 2 min read | July 2019

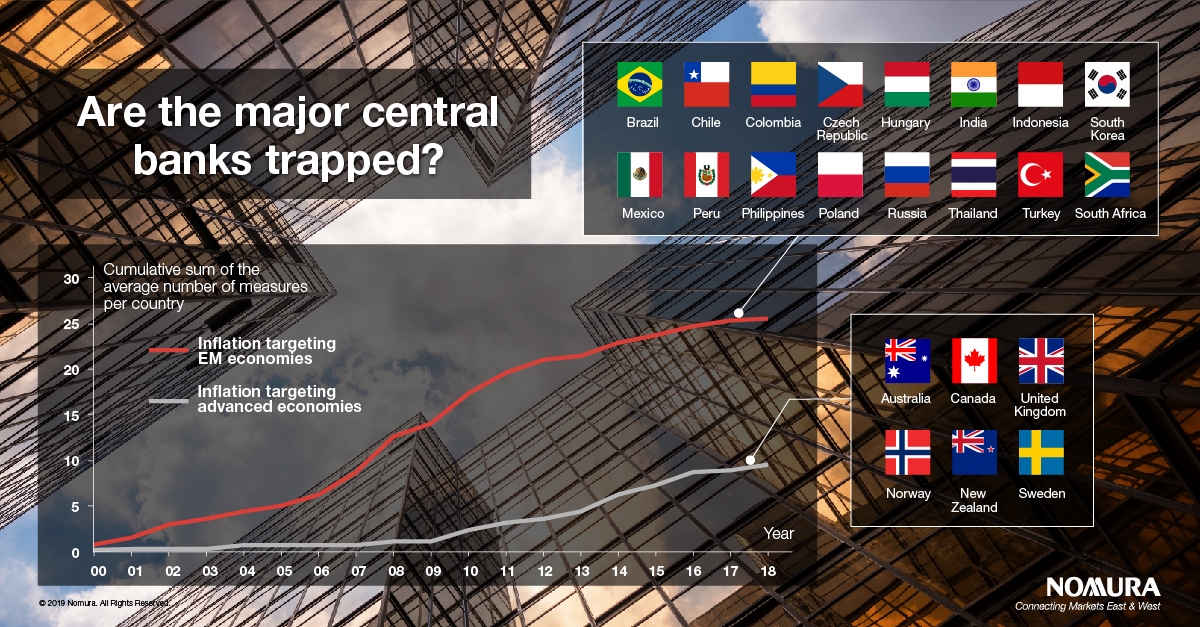

The policy reaction function of many of the world’s major central banks looks to have changed and a number have yet again made a dovish shift. We argue that these central banks could be “trapped” in an ultra-loose monetary policy stance and are losing their ability to normalize policy. Moreover, this extended period of super-low-for-long rates is bringing diminishing returns and rising costs. Financial markets and central banks are becoming increasingly and unhealthily interconnected, generating complicated two-way feedback loops and systemic risks. We conclude by considering a number of alternate policy paths.

While understandable – particularly given the inflation mandates of these central banks – we see declining benefits and rising risks from this policy path. Indeed, ultra-loose monetary policy can:

We have also observed a complicated and potentially dangerous sensitivity and interconnectedness growing between central banks and financial markets. Central banks increasingly need positive wealth effects for their ultra-loose policies to have the desired impact and are incentivized to deliver “no surprises” to markets. However, this can create moral hazard and risks excessive leverage and risk-taking.

As policy-encouraged debt levels grow over time, the economy becomes less able to handle a return to historically more normal rates; we could be trapped in a low-rate world.

Is there an alternate path; how can we get out of this?

We believe that maintaining overburdened monetary policy settings (i.e., more of the same) could be helpful in the short term but increases longer-term systemic risks. A more balanced policy mix, with less reliance on monetary policy and more focus on fiscal policy and structural reform would be a better option. At a minimum, an expanded toolkit for central banks, with more control over macroprudential policy and FX management could help too. Developed market policymakers could learn from EM, as the latter has taken the lead on the successful implementation of macroprudential measures.

For more details, read our full report here.

Head of Global Macro Research

Week Ahead Podcast Host & Australia Economist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Central Banks | 2 min read February 2019