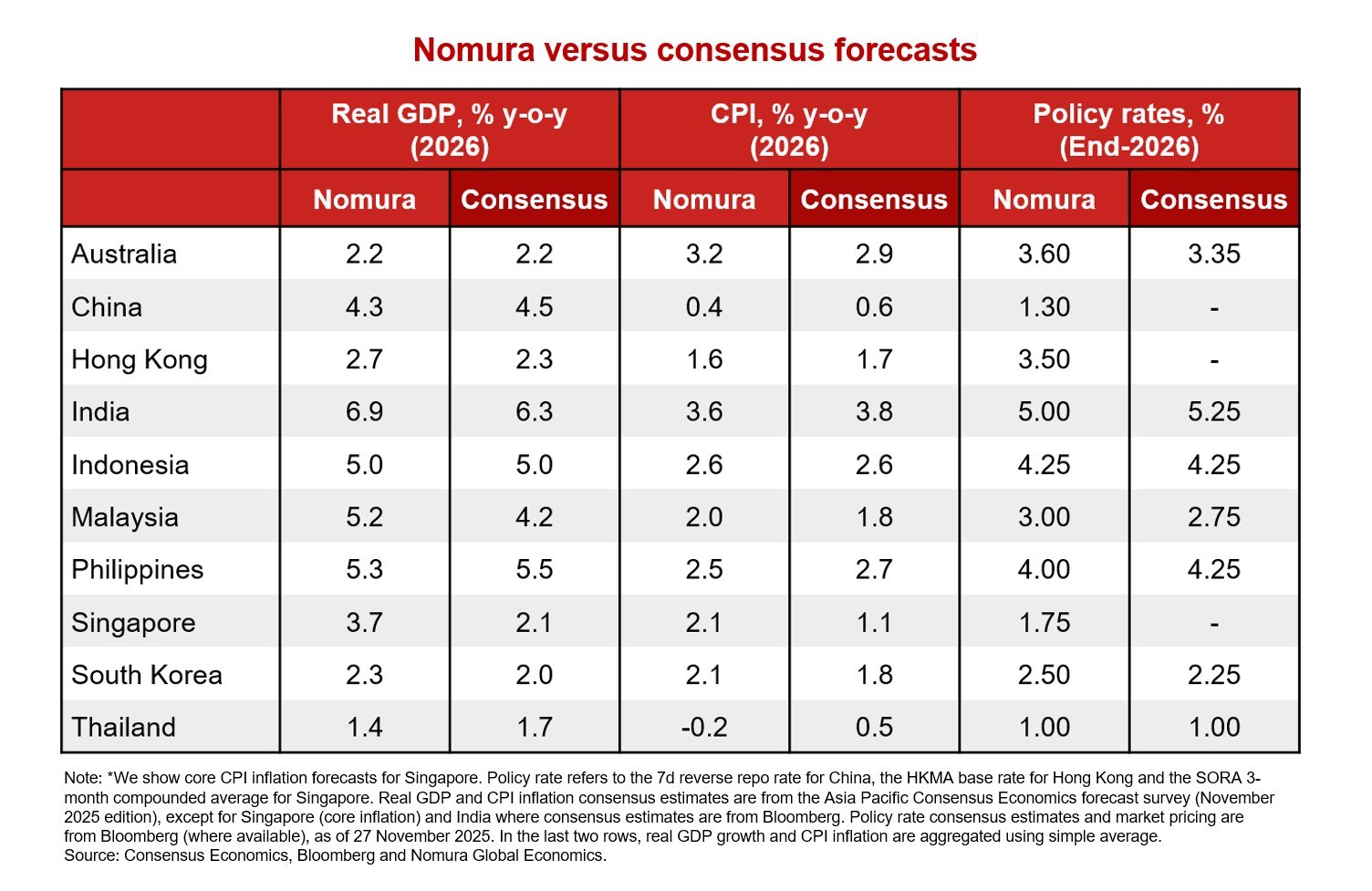

2025 can be distilled down to one word – resilience. Despite increased US trade protectionism, Asia's exports held up, supported by strong AI demand, transshipment and a gradual ramp-up in tariffs. Yet domestic demand, especially private consumption, remained soft, which helped keep inflation subdued and allowed central banks to lower policy rates closer to neutral.

As we look ahead to 2026, three key questions define the outlook. Will growth broaden beyond AI? Will inflation rebound? And is the easing cycle over? Nomura economists shared their forecasts in the 2026 Asia Macro Outlook report.

Tech exports remain in the spotlight

We expect the strong momentum of tech exports to sustain through 2026, driven by AI demand, higher memory prices and low tech inventories. Capex by major US hyperscalers will likely grow by a further 40-60% y-o-y in 2026, pushing up demand for AI chips and spilling over to data storage and server demand. Nomura tech analysts expect DRAM (dynamic random-access memory) prices to rise by 44% y-o-y in 2026 and NAND prices to climb by 61%. These price increases would generate significant terms-of-trade gains for Korea.

Non-tech exports, on the other hand, will likely remain soft in 2026 due to spillovers from China, US tariffs and elevated inventories. Weakening domestic demand in China is likely to result in lower import demand, weighing on export growth across the rest of Asia. The recent lowering of US tariffs on China will diminish the gains accrued to ASEAN through transshipment. US tariffs continue to pressure profit margins of exporters. Even though Asia is actively pursuing export diversification, the benefits will take time to materialize.

A mixed domestic demand picture

The outlook for domestic demand remains mixed, due to the tug-of-war between limited domestic spillovers from AI versus supportive policies and local idiosyncrasies. The deployment of AI investment creates a paradox: while it boosts productivity elsewhere, it also threatens routine jobs, magnifying the K-shaped recovery. Although higher memory prices will boost chip companies’ profits, firms have become more conservative on capex to prevent oversupply.

That said, we see several positive factors that should support domestic demand. Previous policy easing has created more favorable financial conditions over the past year, which should benefit rate-sensitive sectors such as housing. Lower inflation is boosting real disposable income, and fiscal policy should be growth-supportive in Korea, Singapore and Japan. In 2026, we see varied demand drivers across Asia that should create both leaders and laggards.

Korea, Malaysia, Singapore, Japan and India should outperform

In the year ahead, Korea should benefit from the twin chip-housing supercycles, which we believe will boost exports, bring positive wealth effects and drive above-trend growth. We expect growth in Malaysia and Singapore to be led by both strong tech exports and robust domestic demand; the latter due to resilient labor markets and increased infrastructure investment. Domestic demand in India should gradually recover, due to low inflation and easier financial conditions.

Inflation will likely remain benign

Despite adverse base effects in 2026, we expect inflation to remain benign. On the supply side, low input cost pressures from oil and commodity prices should cap upstream price pressures, while China's overcapacity is an additional disinflationary impulse for the region. Asian currency appreciation should also ease imported inflation starting in Q2.

On the demand front, output gaps should turn less negative, but are mostly tracking near zero, while cooling wage growth should ease service sector prices. On average, we expect CPI inflation of 1.9% y-o-y in 2026, up only marginally from 1.7% in 2025. Within Asia, we see deflation risks in Thailand and China, inflation below target in India, and within target in the Philippines and Indonesia. By contrast, we expect sticky inflation in Australia, and Singapore's core inflation to rise above 2.0%.

A monetary policy divide between the North and South

The policy easing cycle across Asia is largely complete, despite low inflation, reflecting improving growth, near-neutral policy rates and the need to conserve ammunition. Financial stability concerns (higher housing prices) are also likely to constrain some central banks. This cautious approach contrasts with our US economics team’s view of two Fed rate cuts in 2026 and suggests Asia could decouple on the hawkish side.

That said, we see a North-South monetary policy divide. We believe the easing cycle is over in Korea, New Zealand, Australia and Malaysia, where we are more optimistic on growth. We expect a rate hike in Malaysia in Q4 2026 as Bank Negara Malaysia pre-empts a buildup of financial stability risks, and rate hikes by the Reserve Bank of New Zealand in 2027. In Japan, we expect only one more rate hike in December 2025, followed by a pause for the whole of 2026, as core inflation drifts below 2%. Conversely, we expect residual rate cuts in India, Thailand, Indonesia and the Philippines, due to a mix of low inflation and/or weaker growth. In China, we expect a 10bp policy rate cut, but fiscal easing should play a larger role around spring 2026, via increased lending by policy banks to local governments.

Key upside risks to our outlook include faster global growth, stronger domestic demand in China and a sharp rise in capital inflows, which would ease financial conditions and create a positive feedback loop. Downside risks include weak US demand, an escalation of trade tensions, or a bursting of the AI bubble, which could trigger market and macro spillovers.