Volatility | 3 min read | September 2023

Bumper Gas Stores to Insulate Europe from Cold Winter Supply Shock

Europe’s efforts to build up natural gas stores look set to pay dividends and shield it from supply shortages if a cold winter sets in.

Volatility | 3 min read | September 2023

Europe’s efforts to build up natural gas stores look set to pay dividends and shield it from supply shortages if a cold winter sets in.

Europe’s efforts to build up natural gas stores look set to pay dividends and shield it from supply shortages if a cold winter sets in.

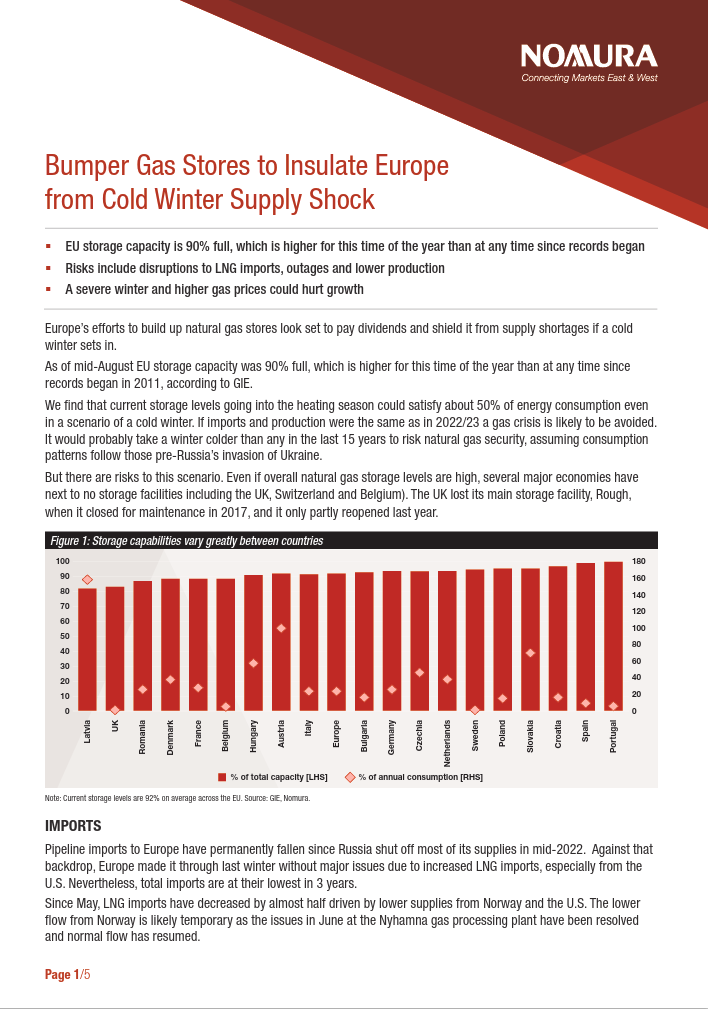

As of mid-August EU storage capacity was 90% full, which is higher for this time of the year than at any time since records began in 2011, according to GIE.

We find that current storage levels going into the heating season could satisfy about 50% of energy consumption even in a scenario of a cold winter. If imports and production were the same as in 2022/23 a gas crisis is likely to be avoided. It would probably take a winter colder than any in the last 15 years to risk natural gas security, assuming consumption patterns follow those pre-Russia’s invasion of Ukraine.

But there are risks to this scenario. Even if overall natural gas storage levels are high, several major economies have next to no storage facilities including the UK, Switzerland and Belgium). The UK lost its main storage facility, Rough, when it closed for maintenance in 2017, and it only partly reopened last year.

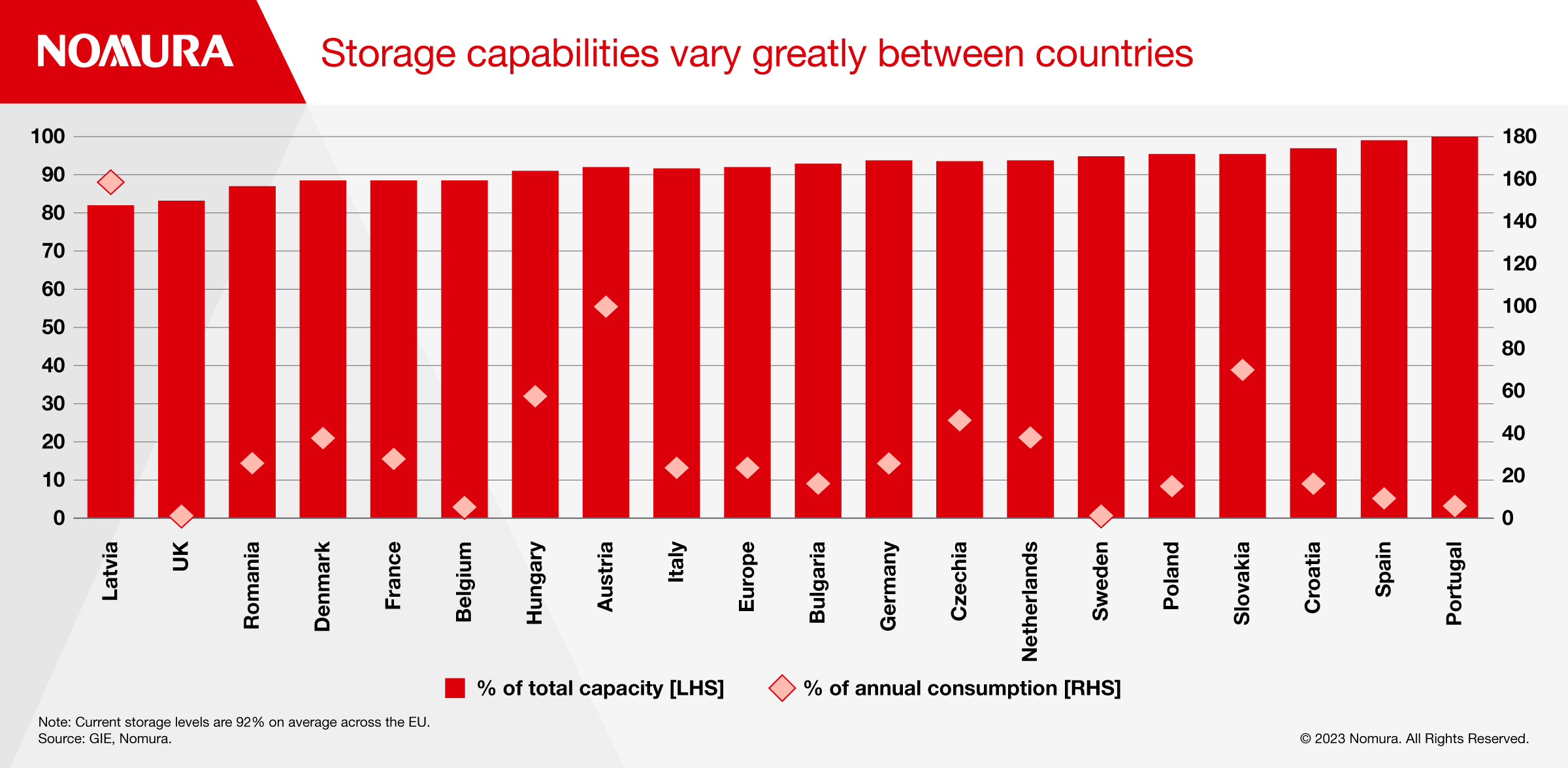

Pipeline imports to Europe have permanently fallen since Russia shut off most of its supplies in mid-2022. Against that backdrop, Europe made it through last winter without major issues due to increased LNG imports, especially from the U.S. Nevertheless, total imports are at their lowest in 3 years.

Since May, LNG imports have decreased by almost half driven by lower supplies from Norway and the U.S. The lower flow from Norway is likely temporary as the issues in June at the Nyhamna gas processing plant have been resolved and normal flow has resumed.

Lower U.S. LNG exports to Europe may be more concerning, as it could indicate a deeper shift in trading routes. Data from the most recent month (June) show a strong increase in U.S. LNG exports to Asia.

To a large extent, this represents seasonality; however, it is notable that exports to China in June were much higher than a year ago. Going forwards, weaker China growth will probably constrain its demand for LNG imports.

The price differential with Latin America suggests that if Europe needs to increase imports during the winter, it will have to pay a higher price. Additionally, the competition for U.S. LNG exports may lead to more volatile prices, as supply is relatively inelastic. There will be no additional LNG capacity in the U.S. until 2025, despite recently announced expansion plans in response to higher gas prices. Lead time can be several years.

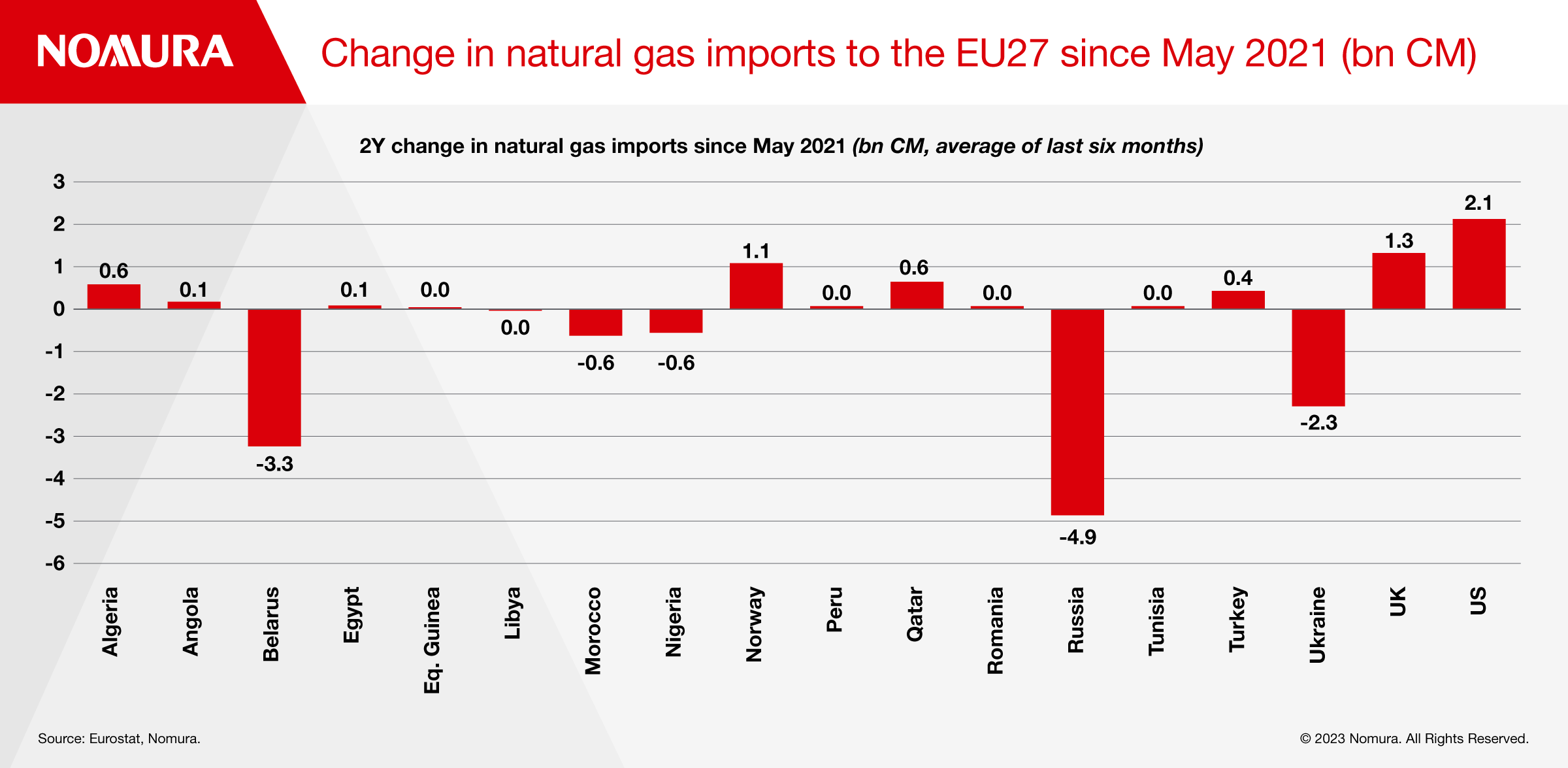

Furthermore, even if LNG imports resume at the pace of last year, Europe will have to adapt to permanently lower pipeline imports. In the last two years, there has been a significant decrease in gas imports from the countries involved in the Russian invasion of Ukraine plus Belarus.

Other countries such as Algeria, Qatar and the UK have increased their exports to the EU to fill the gap but it has been insufficient.

That said, the fall in LNG imports to Europe could also be interpreted as reflective of demand already having been satisfied rather than a supply issue. Storage is full and consumption has fallen.

Outage/sabotage to Norwegian pipeline: Norwegian gas imports are by far the most important flows for the EU so severe disruptions would be a significant risk to energy security.

Russian gas through Ukraine: Europe still receives a fair amount of Russian gas through Ukraine and the Yamal pipeline. A further deterioration in diplomatic relations between Europe and Russia may result in these supplies being cut off. Nevertheless, this has only made up about 5% of total pipeline imports to mainland Europe in the last three months, so may not be as severe a hit as the IEA suggests.

Supplies from Algeria: A flare-up in tensions between Algeria and Morocco may disrupt natural gas supplies to Europe. Both countries have been in dispute over the Western Sahara territory since the 1960s and in 2021, they broke ties, halting gas flows from Algeria to Spain through the Maghreb pipeline.

Australian strikes: Risks are growing that Australian workers in a key LNG plant (Chevron) will strike as the status of labour talks is still uncertain. Australian LNG makes up 10% of global supply, but little is sent to Europe. Regardless, Europe would have to compete with Asian countries looking for replacement shipments. However, a strike in a strategically important sector such as LNG is unlikely to last long, with suppliers and the Australian government keen to reach a quick agreement.

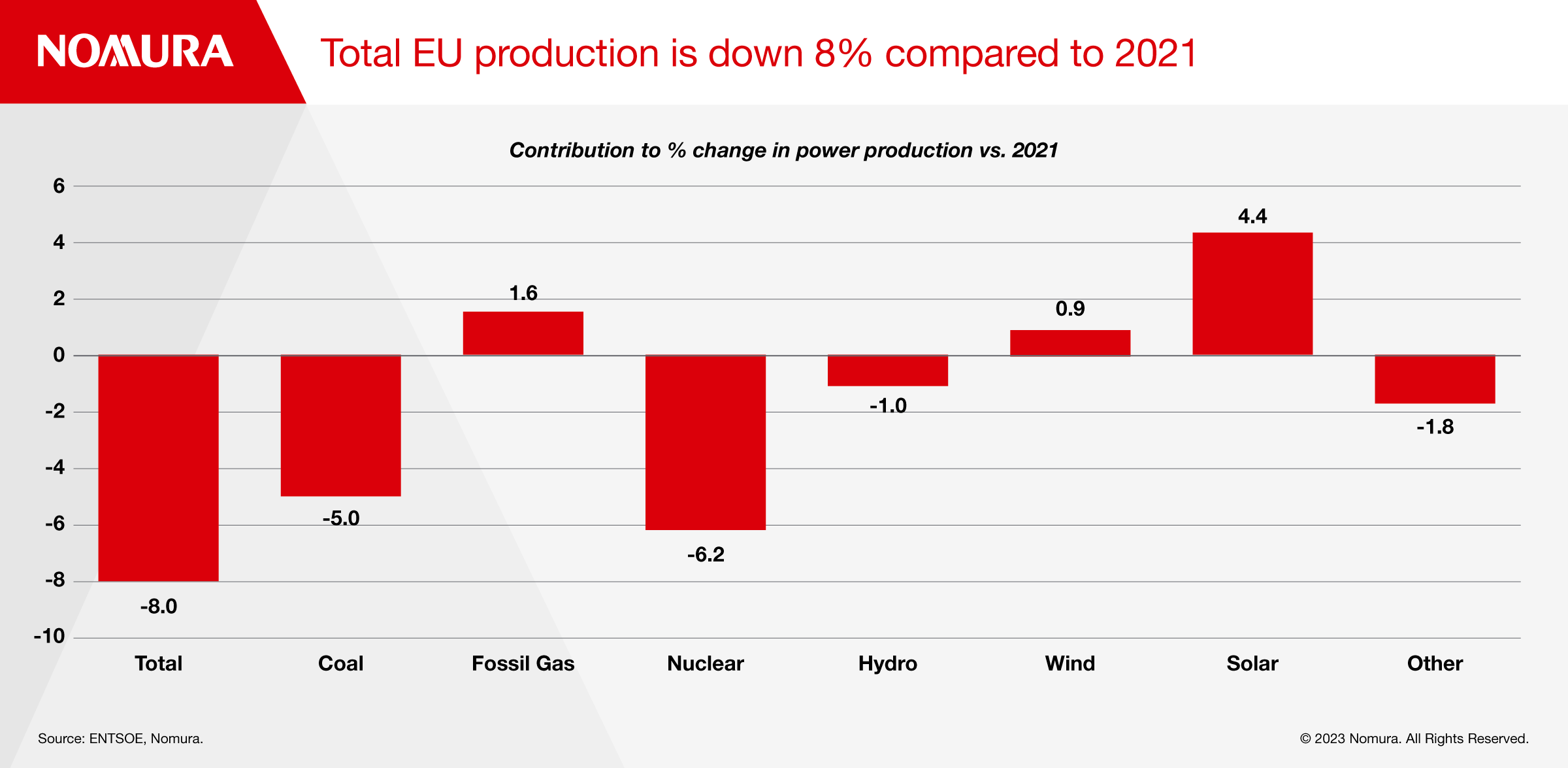

Energy production is not matching the levels of last winter, raising the prospect of gas shortages. Total power generation has dropped nearly 8% compared with the same period in 2021 which was broadly a normal year for European energy, according to ENTSOE. Coal power production is down 38% relative to 2021. There was a surge at the end of 2022 as Germany stepped up its coal production to fill the gap from lost Russian supplies, but climate considerations have since caused Germany to scale this back.

Nuclear power output is down nearly 20% relative to 2021. Germany shut its last three power plants in April 2023. There was also an involuntary reduction in French output due to signs of stress corrosion cracking and the driest summer in 500 years, creating difficulties for plant cooling systems.

More reassuring is the surge in wind and solar power generation as the EU pushes for a green transition.

Variable renewable power generation: the volatility of renewable energy production could pose a problem. The technology is not viable to store electricity efficiently, so a temporary fall in production could be enough to cause blackouts. Solar power performs poorly in the winter when it is cold and dark. Wind power and hydropower may perform better in the windy and rainy conditions of winter but again this is unreliable.

Environmental pressures: If environmental movements like “Just Stop Oil” gain a foothold on the policy agenda they could jeopardize energy security.

The IEA forecasts consumption to be down nearly 20% in 2023 compared to 2021, supporting the case against a gas crisis in 2023. In industry, many companies have switched fuel sources away from gas mainly to oil while also making efficiency improvements. For consumers, elevated prices are likely to encourage them to leave the heating off for longer.

Cold winter: There is a relatively strong negative correlation between daily temperatures and power load (consumption). In a typical German winter, consumers use about 13% more energy when the temperature is 0 degrees Celsius versus when it is 20 degrees Celsius.

Generous government support: If governments repeat the level of support seen in 2022, this risks pushing up consumption. The ECB has warned that fiscal intervention is likely to be “temporary, targeted and tailored.” This is important to control the fiscal cost of measures but also to ensure the price mechanism can bring the market to equilibrium (i.e. minimal shortages).

Growth:

There is a low-probability risk of a sharp decline in output stemming from a full-blown gas crisis. Such a scenario would require net imports, production and storage to be unable to meet winter demand. But storage alone could keep Europe going for most of the winter, and there is little evidence so far predicting tensions over natural gas imports.

If concerns over gas security increase, leading to higher gas prices, it could reduce output by encouraging firms to cut back production or in some cases push firms into bankruptcy. We saw a large shock to output in Q4 2022 as a result of higher gas prices.

Inflation:

Higher energy prices have a direct effect on retail energy prices. Severe gas shortages may reignite concerns that the disinflationary trend will not reach completion and, therefore, add fuel to the wage-price spiral.

Central bank policy:

A surge in natural gas prices may encourage European central banks to raise their rates further. This would likely be a premature pause followed by hikes, affecting rates in 2023 relatively little but having a bigger effect on rates in 2024.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.