Reducing carbon emissions by switching from gasoline-powered vehicles to electric vehicles (EVs) has become an important part of the global response to climate change.

China, which is already the world’s largest automobile manufacturer and market, is leveraging the development of its EV industry to transform itself into an automotive superpower. In 2015, China’s State Council announced its ‘Made in China 2025 Plan’ that designated EVs as one of its 10 major priority industry sectors. Since then, the government has prioritized making battery electric vehicles the majority of automobile sales by 2035.

In addition to government support, the rise of emerging private companies such as BYD and the modularization of production have provided favorable conditions for the development of China's EV industry.

Against this backdrop, China’s automobile industry is rapidly catching up with Japan. Within its own borders, Chinese brands are increasing market share at the expense of Japanese manufacturers. In the international market too, exports have overtaken Japan.

EVs in China are commonly referred to as “new energy vehicles,” and include battery EVs, Plug-in hybrids, and Fuel-cell EVs.

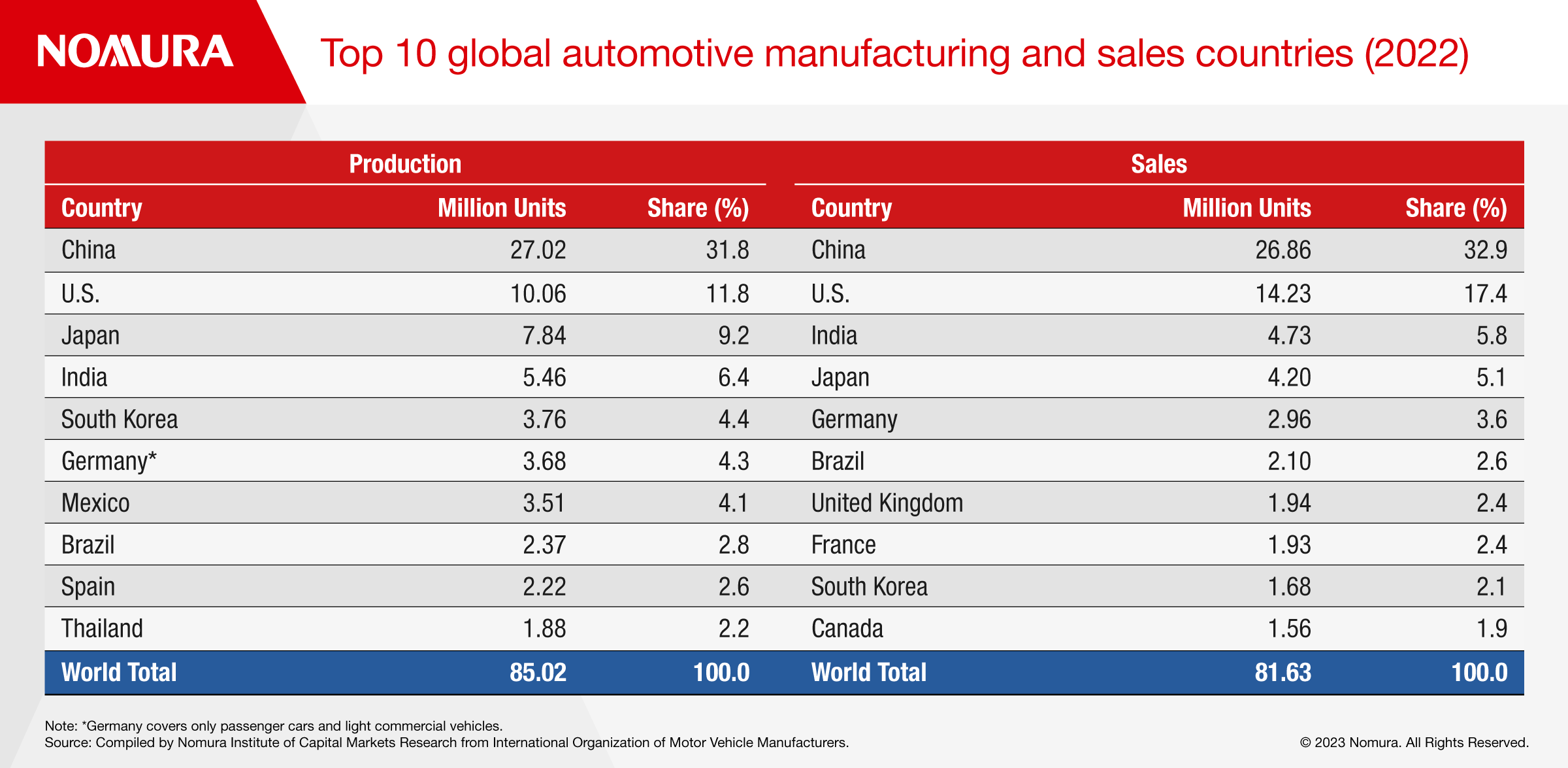

THE WORLD’S LARGEST AUTOMOTIVE INDUSTRY

Although the development of the car industry in China has long lagged western countries, it has grown rapidly over the past 15 years with production topping 10 million units in 2009. The industry entered a slump in 2017, when production and sales peaked at around 29 million units amid economic friction with the United States, followed by the fallout from COVID-19.

In 2022, China auto production rose 3.4% to 27.02 million units, and sales rose 2.1% to 26.86 million units, both exceeding 30% of the world’s total according to the China Automobile Manufacturers Association (CAAM) and beating the United States and Japan.

Following the end of the COVID-19 pandemic, cumulative vehicle production in China in January-September 2023 reached 21.075 million units, up 7.3% year-on-year, and sales reached 21.069 million units, up 8.2% year-on-year.

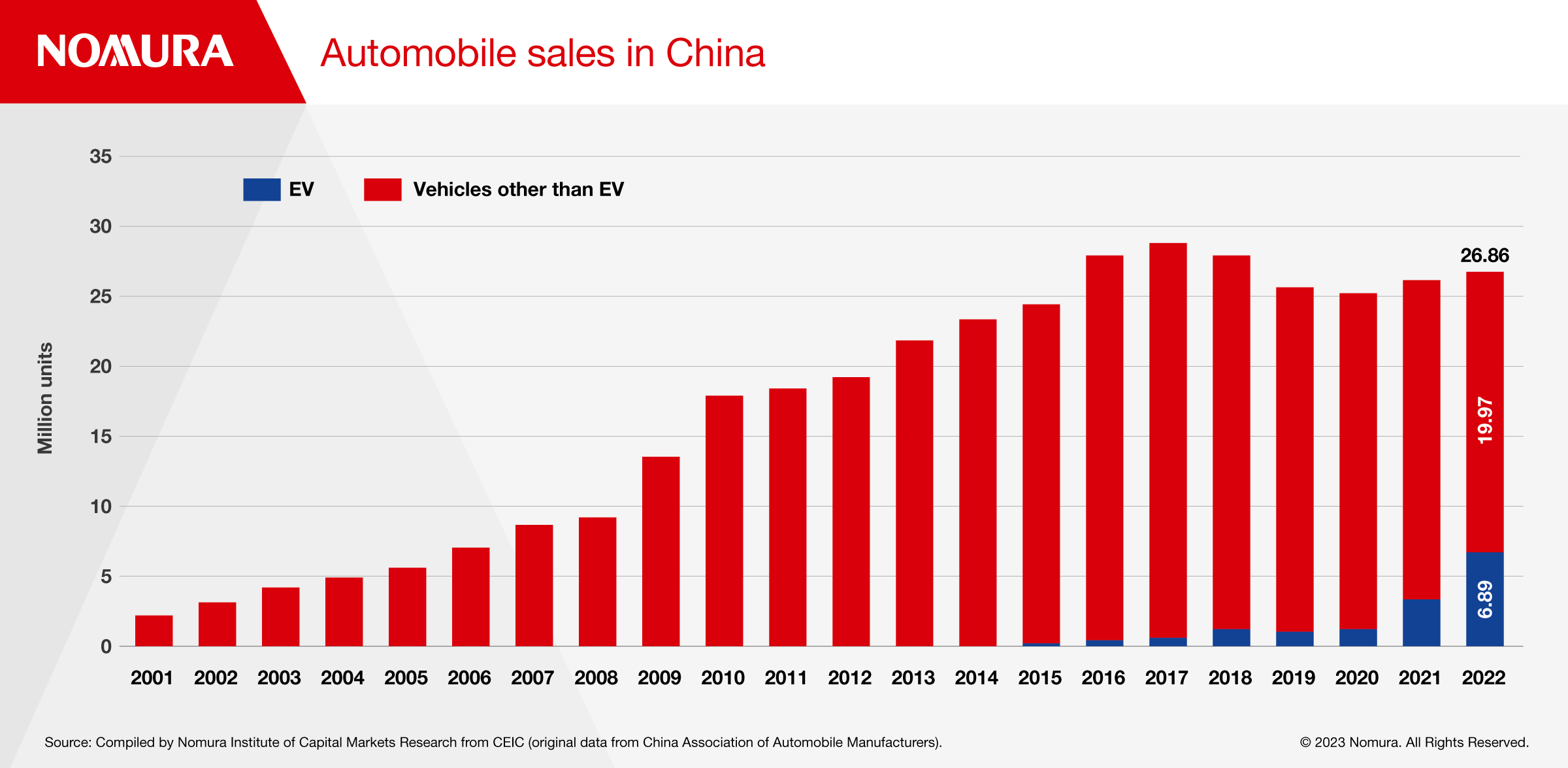

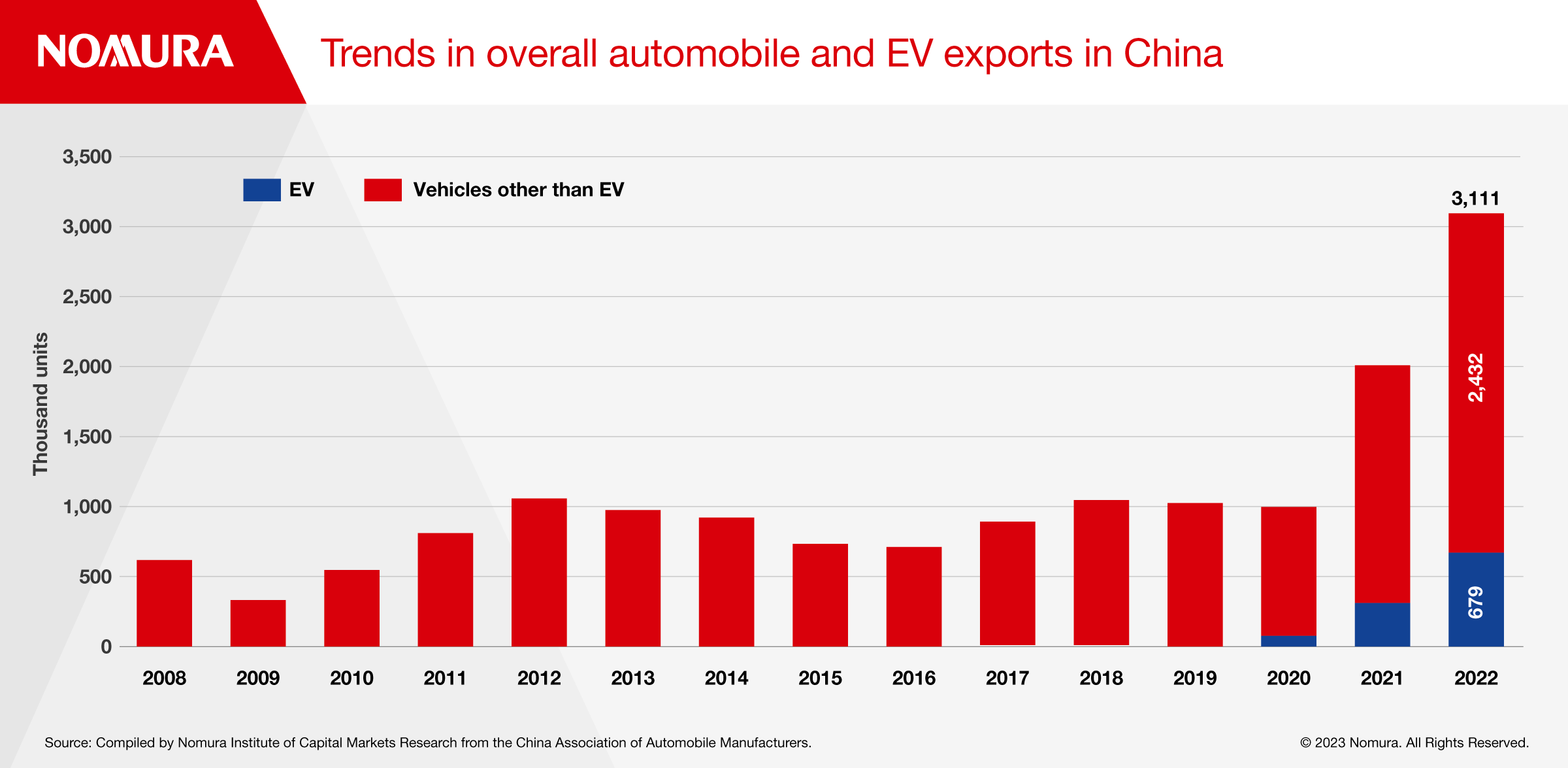

In China, auto exports are growing much faster than production and sales. Exports doubled from around 1 million a year between 2012 and 2020 to 2.01 million in 2021 and jumped to 3.1 million in 2022 according to the CAAM. In 2023, China exported 3.39 million units from January to September, up 60.0% from the previous year putting it on track to becoming the top car exporter worldwide, surpassing Japan.

THE ACCELERATING SHIFT TO EVS IN CHINA

EVs are driving the production, sales and export of automobiles in China. In 2022, EV sales increased 93.4% to 6.89 million units, accounting for 25.6% of total automobile sales. For the eighth consecutive year China has topped the global EV sales list.

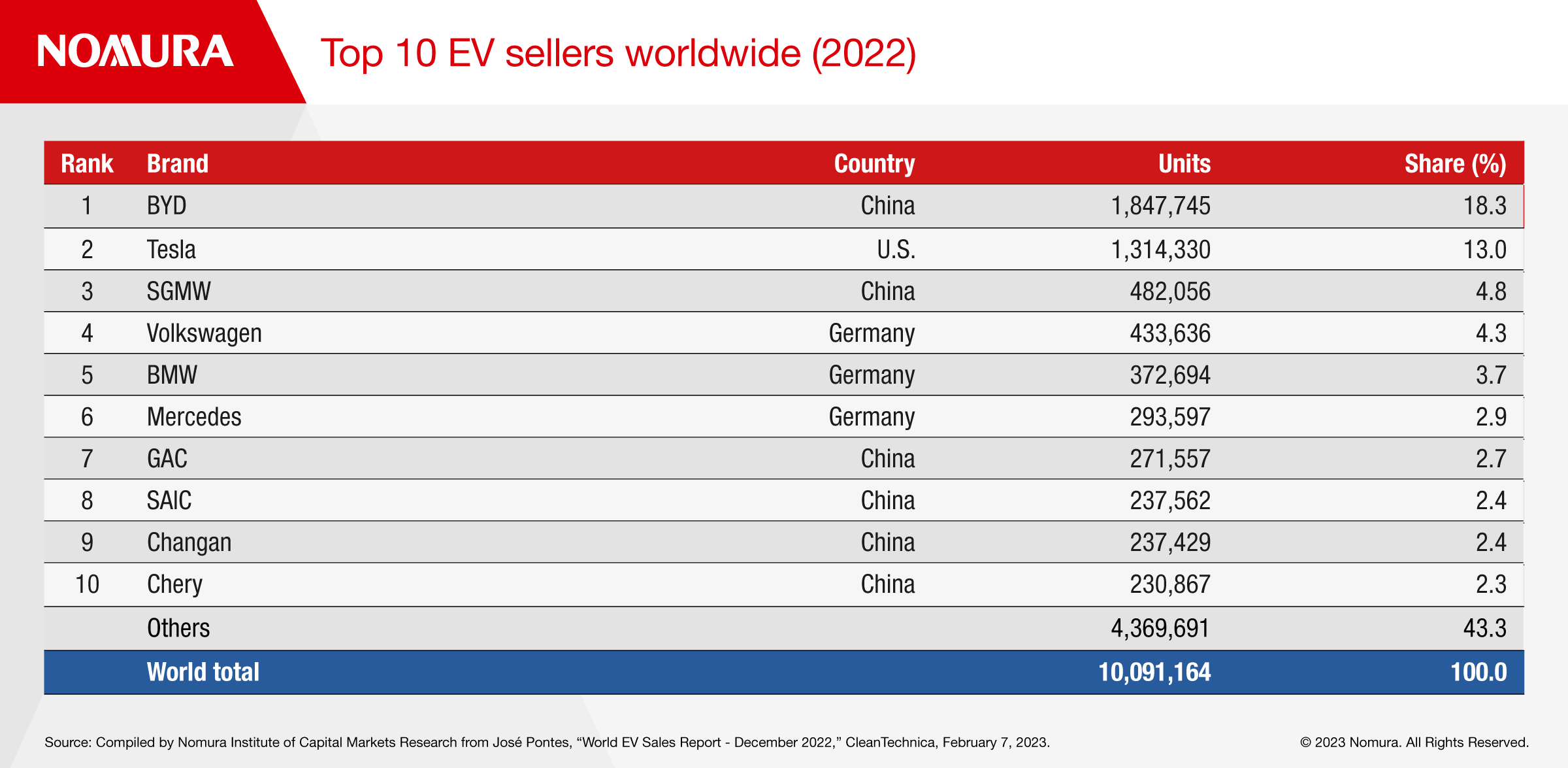

Chinese companies accounted for 6 of the top 10 global EV sales in 2022. Among them, BYD’s sales reached 1.85 million units, and its global market share was 18.3%, surpassing Tesla (1.31 million units sold, 13.0% global market share) as the world’s top seller.

In addition, EV exports from China surged to 679,000 units in 2022, 2.2 times the previous year, and reached 825,000 units between January-September 2023, 2.1 times that of the previous year, contributing significantly to the expansion of China’s overall vehicle exports.

The rapid expansion of the EV industry in China is mainly due to government support, technological innovation, cost reduction, and supply chain development.

The Chinese government is actively promoting environmentally friendly electric vehicles to counter climate change through purchase subsidies, exemptions from purchase taxes, and deregulation of license plates. EVs benefit from convenient charging through the construction of charging stations and the enhancement of charging networks. The “New Energy Vehicle Industry Development Plan (2021 – 2035)” announced by China’s State Council in 2020, called for an increase in EV sales from about 5% of total auto sales at that time to about 20% in 2025, and set a goal to make BEVs the majority of new vehicle sales by 2035.

While Chinese companies have been relatively late to enter the EV market, they have made significant progress on innovation and keeping prices down. Chinese EV companies have superior battery technology, electric drive systems, smart mobility and more. Leveraging these strengths, Chinese-made EVs have become internationally competitive in terms of cruising range, charging speed, and automated driving.

In 2022, the sales weighted average price of small BEVs in China fell below $10,000 compared to more than $30,000 in Europe and the United States, according to the International Energy Agency.

In addition, China has developed an industry-wide supply chain, including battery manufacturing, and component suppliers. China’s Contemporary Amperex Technology (CATL) and BYD are ranked first and second, respectively, in the global EV battery market, accounting for about half of the combined global market share. Highly-developed supply chains have led to increased manufacturing and R&D efficiency, reduced production costs and increased competitiveness.

THE RISE OF BYD

For a long time, Chinese automobiles were mainly produced through joint ventures with foreign companies and sold in the domestic market as foreign brands. The share of Chinese brands in passenger car sales has been around 40% for the past decade, but in 2022 it climbed to 49.9%, and exceeded half (54.2%) in the first eight months of 2023. At the same time, Japanese market share dropped from a peak of 23.1% in 2020 to 14.5% in the first eight months of 2023.

Led by EVs, BYD’s passenger car sales are expanding rapidly, and in the first quarter of 2023 it surpassed Volkswagen, which had held the top spot in the Chinese market for many years.

In the EV field, of the top 10 selling companies in 2022, except for Tesla, which is 100% foreign, and some companies that have joint ventures with foreign companies, such as Shanghai Automobile, the rest are Chinese brands. In passenger cars only, Chinese brands account for 79.9% of China’s EV market.

BYD, a privately owned company headquartered in Shenzhen, is one step ahead in the development of the EV industry in China. Founded in 1995 as a battery manufacturer, BYD operates globally in four areas: IT electronics, automotive, new energy and urban mobility. It has sold vehicles in more than 70 countries and regions around the world. Berkshire Hathaway, led by renowned investor Warren Buffett, bought 10% of BYD for $230 million in September 2008, anticipating its growth potential. The company quickly gained attention from both domestic and international media.

The company’s strength lies in battery technology and its EVs are equipped with lithium-ion iron phosphate batteries that use proprietary technology. This is superior for safety, energy density, and range per charge compared to other lithium-ion batteries known as ternary systems.

LEVERAGING MODULAR EV PRODUCTION

The shift to EV production is transforming the auto sector from an integral to a modular industry, and this provides a technological environment favorable to the development of China’s auto industry.

In modular industries, products are made by combining standardized modules that can be manufactured independently. Since each module performs a specific function and is interchangeable, they can be assembled into a variety of products. This approach is efficient and flexible, and contributes to increased productivity and product variation.

On the other hand, integral industries create products by designing components and combining them in coordination with each other. This approach is suited to creating original products, but design and production costs tend to be high because many parts and components are bespoke.

Japan is a leader in integral industries while China excels in modular industries. In Japan, the spirit of “Takumi” such as attention to detail, the accumulation of skills and experience, the pursuit of quality and reliability, the passing on of traditions and the development of technology, support integral industries. On the other hand, China is using its strengths in mass production, cost competitiveness, speed and flexibility in manufacturing to lead the modular approach.

Since EVs have fewer parts than conventional gasoline vehicles, it is easier to design and manufacture components as independent modules. The shift to EVs puts China in pole position to expand its market share in the global automotive industry while Japan will need to adapt and compete harder.