2020’s bond issuance (rather unsurprisingly) has centred around the most affected COVID sectors like travel, leisure and oil.

This however has presented both companies and investors with two opportunities:

This recent increase in issuance has brought some much-needed diversity to the convertible bond space. Especially in the US where technology and healthcare dominate.

It has also brought much needed yield payments to investors through the form of coupons paid on the bonds. Let’s take for example the US CB market where coupons were averaging 2.95% vs recent issuance where it has jumped to 10-13%, combined with the equity option, you can see why convertible bond investors are keen to take on future equity risk.

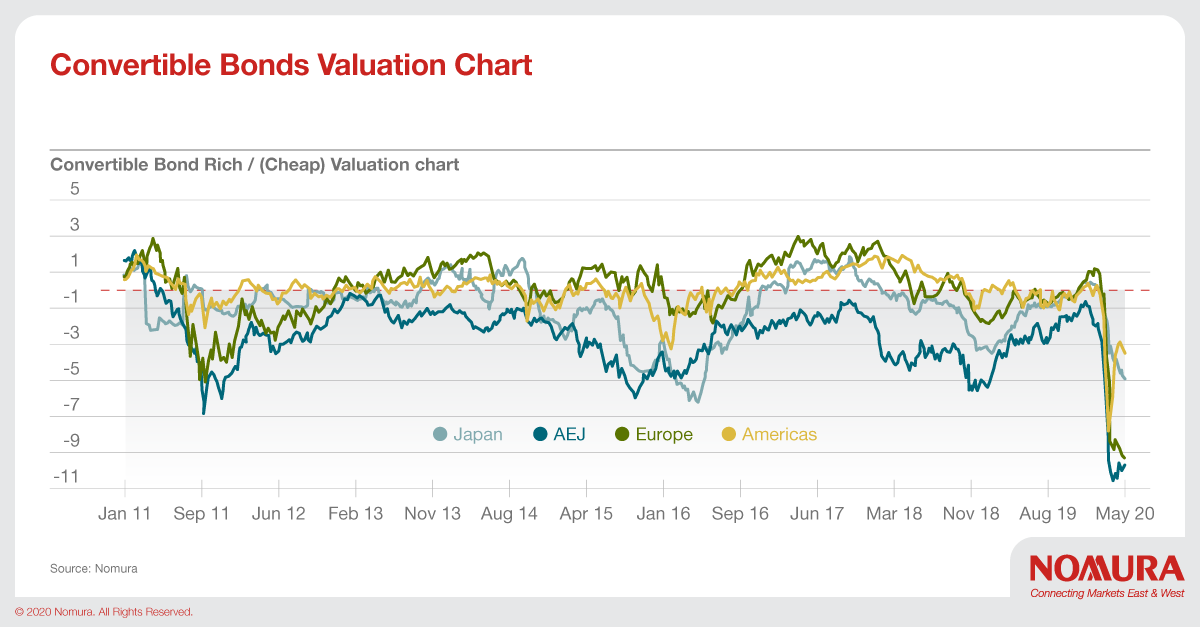

Convertibles are a bond with an imbedded equity option, and with equity volatility at high levels, the imbedded option within the convertible bond is inherently worth more.

This has meant that investors currently hold equity options worth much more, due to the ability of stocks to move into and out of the money more aggressively. Convertibles have the ability to reprice higher as equities move higher, but trade down less when equities trade down due to their bond element.

The more extreme the equity volatility, the greater the value due to the credit-equity correlation, and the convertible bond product’s tendency to reward balanced profiles with higher implied valuations.

Ultimately, the convertible bond asset class and recent issuance is providing additional embedded optionality from liability management exercises and offering generous change of control provisions.

As a result, the Convertible Bond Asset class is providing a large opportunity for investors globally across Japan, Asia Ex-Japan, EMEA and the US.

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.