Central Banks | 4 min read | April 2026

The Countries Most Exposed to De-Dollarization

Even modest repatriation of USD assets could significantly appreciate the value of their currencies and erode export competitiveness

Central Banks | 4 min read | April 2026

Even modest repatriation of USD assets could significantly appreciate the value of their currencies and erode export competitiveness

There is seemingly insatiable global demand for USD assets. This is a result of the US’s consistent global economic outperformance, its status as the epicenter of the AI revolution, and its exorbitant privilege of issuing the world’s only reserve currency.

Since the global financial crisis, foreign investors have purchased $2 trillion of US equities and, as of September 2025, total foreign holdings of US equities have skyrocketed to $21.5 trillion. According to the latest US Treasury data from 2024, foreign investors owned 33% of US treasuries, 27% of US corporate debt and 18% of US equities outstanding.

But there is a limit to this demand for USD assets. The US’s total net international investment position — the sum of its foreign portfolio, direct, and other investment assets minus liabilities — has swelled from around $2.5 trillion (16% of GDP) in 2010 to about $27.6 trillion (89% of GDP) as of September 2025.

If the US continues to run large current account deficits, at the extreme, the economy will eventually be owned by foreigners. However, markets would force a breaking point well before then, as pressures mount from increasing outflows of net interest payments, dividends, and profits — a process that could accelerate if global investors start to price in a higher US risk premium.

The prospect of “de-dollarization” is hotly debated, but the term itself seems to mean different things to different people.

The lite version of de-dollarization describes a decline in the broad USD index, fueled by a narrowing of US-foreign interest rate differentials, increased FX hedging of USD exposure, and high US market valuations that encourage diversification away from already large holdings of USD assets and into new investment allocations. This is a more cyclical decline in the USD index, and it could be argued that, before the outbreak of the Middle East conflict, this version was already playing out.

The heavier version of de-dollarization refers to a more structural decline in the broad USD index, including an erosion of the status of USD as the premier global reserve currency. Under the heavier version, foreign investors could start to de-risk from USD assets by selling existing USD holdings. De-risking could be sparked by a massive AI crash or the erosion of trust in US policies and institutions — including the rule of law and Fed independence — reaching a tipping point. However, the notion that there is currently no alternative to the depth and liquidity of US capital markets is a powerful counterargument to a sudden shift to the heavier version.

Some countries have amassed a disproportionate exposure to US portfolio assets relative to their overall holdings of foreign portfolio assets. The implication for those countries most exposed to de-dollarization is that even modest repatriation of USD assets could significantly appreciate the value of their currencies. It would also erode export competitiveness and possibly weaken domestic demand.

We look at the data on foreign holdings of US portfolio assets — equity and debt securities — to gauge which countries would be most affected should de-dollarization, whether lite or heavy, gain traction.

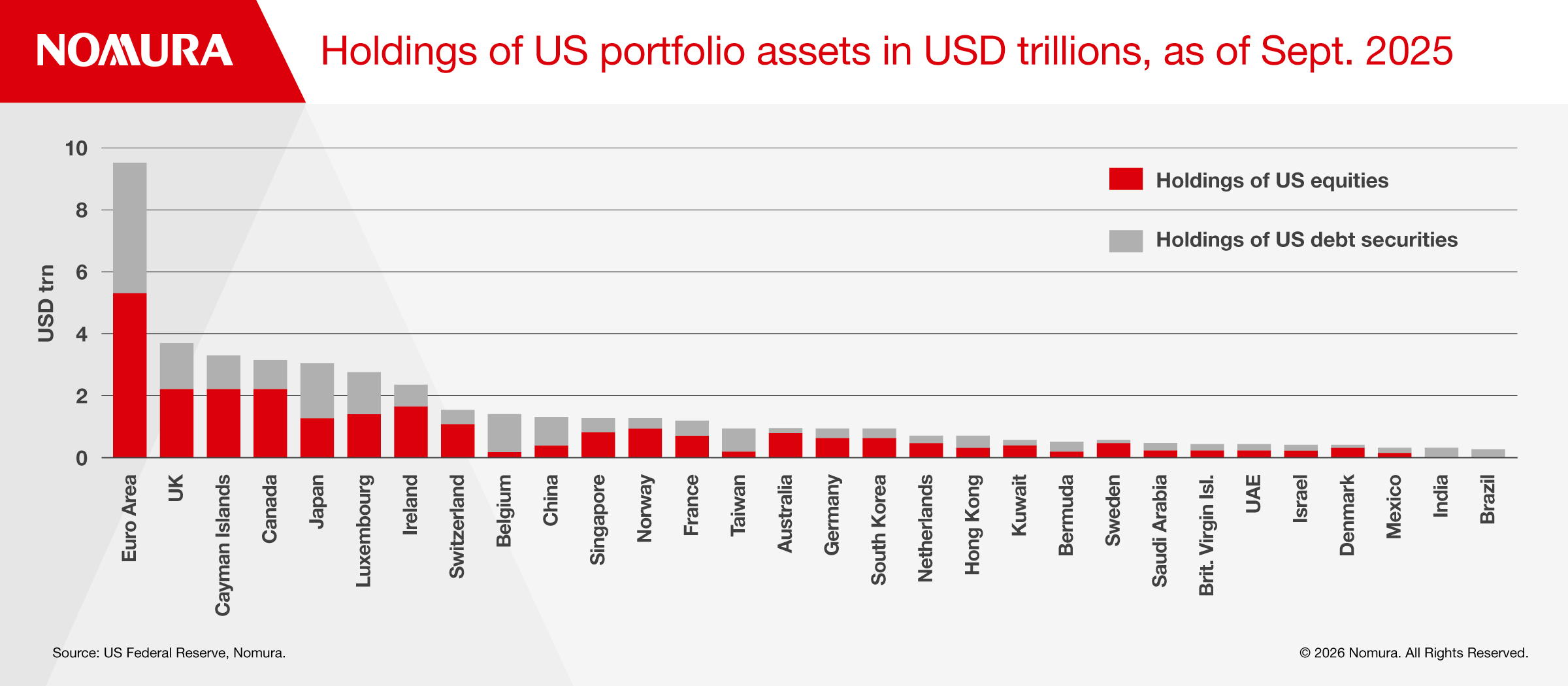

Figure 1 shows the 30 largest foreign holders of US portfolio assets, valued in trillions of dollars, as of September 2025.

The euro area is the largest holder, while the largest single country holders are the UK, the Cayman Islands, Canada, and Japan. It is worth noting that many offshore financial centers — including the Cayman Islands, Luxembourg, Ireland, and Switzerland — are among the largest holders, and the original holders could be investors from other countries.

The composition of US portfolio asset holdings varies significantly by country. For example, among the largest holders of US equities are the UK, the Cayman Islands, and Canada, while the largest holders of US debt securities are Japan, the UK, and Luxembourg.

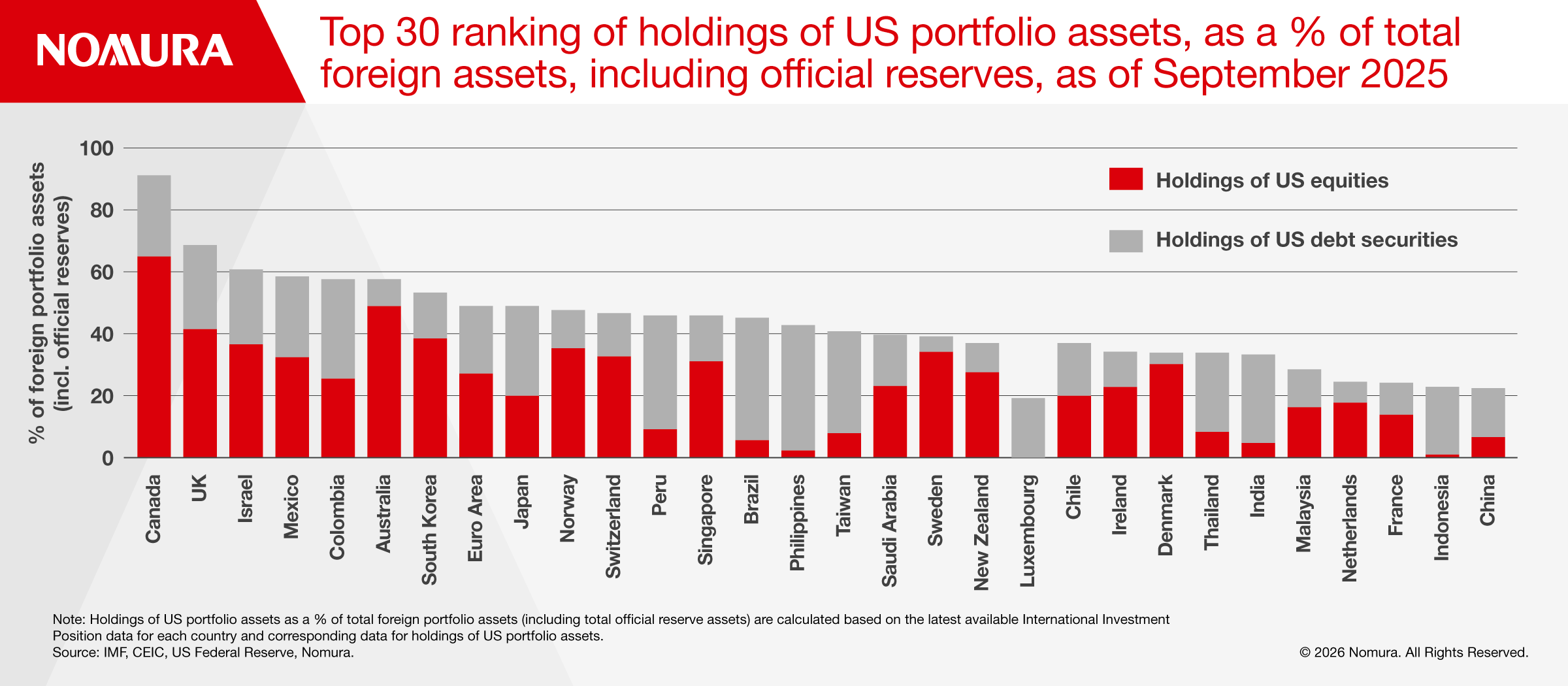

To better gauge which countries could be more affected by de-dollarization, it is important to scale each country’s holdings of US portfolio assets by total holdings of foreign portfolio assets, including reserve assets (Figure 2).

There are four interesting findings to highlight:

Many central banks are increasingly diversifying their foreign reserve assets away from US Treasury securities to gold. There are many possible explanations for this. One is that it can act as a hedge against inflation risk. Another is that US government debt may no longer be perceived as being risk free.

Based on IMF data, central banks’ total holdings of gold at market value was $5.1 trillion in January 2026, having surpassed total foreign official holdings of US Treasury securities in September 2025. Based on the current trajectory, central banks’ total holdings of gold could overtake total foreign non-official (private) holdings of US Treasury securities later this year.

However, central banks’ accumulation of gold has been far from uniform. The largest increases in absolute market value of gold holdings have been mostly in advanced economies, led by the US, Germany, and China. But in terms of the share of gold in total central bank foreign reserve assets, the largest increases are concentrated in emerging market economies. Eight of the top 10 are emerging markets.

There is little doubt that central banks in many countries — notably in emerging markets — have made a conscious effort to diversify their foreign reserve assets into gold. Whether this is a harbinger of a broader de-dollarization trend in the much larger private sector remains to be seen.

Head of Global Macro Research

FX Strategist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.