Energy Transition Shows Resilience Despite Short Term Headwinds

Investors are optimistic about the global megatrends of AI and electrification despite inflationary headwinds and multi-speed transitions on the path to a low carbon future

Europe, China and US show different levels of commitment in moving towards green transition

AI and energy security are key tailwinds for cleaner power

Multi-speed transition is playing out, but the long-term trend is unchanged to deploy $150trn in green technologies

The global megatrends of electrification and energy security are persuading investors in the green transition to look past short-term headwinds when allocating capital, according to senior executives at Nomura Greentech’s Sustainable Leaders Summit in Salzburg, Austria.

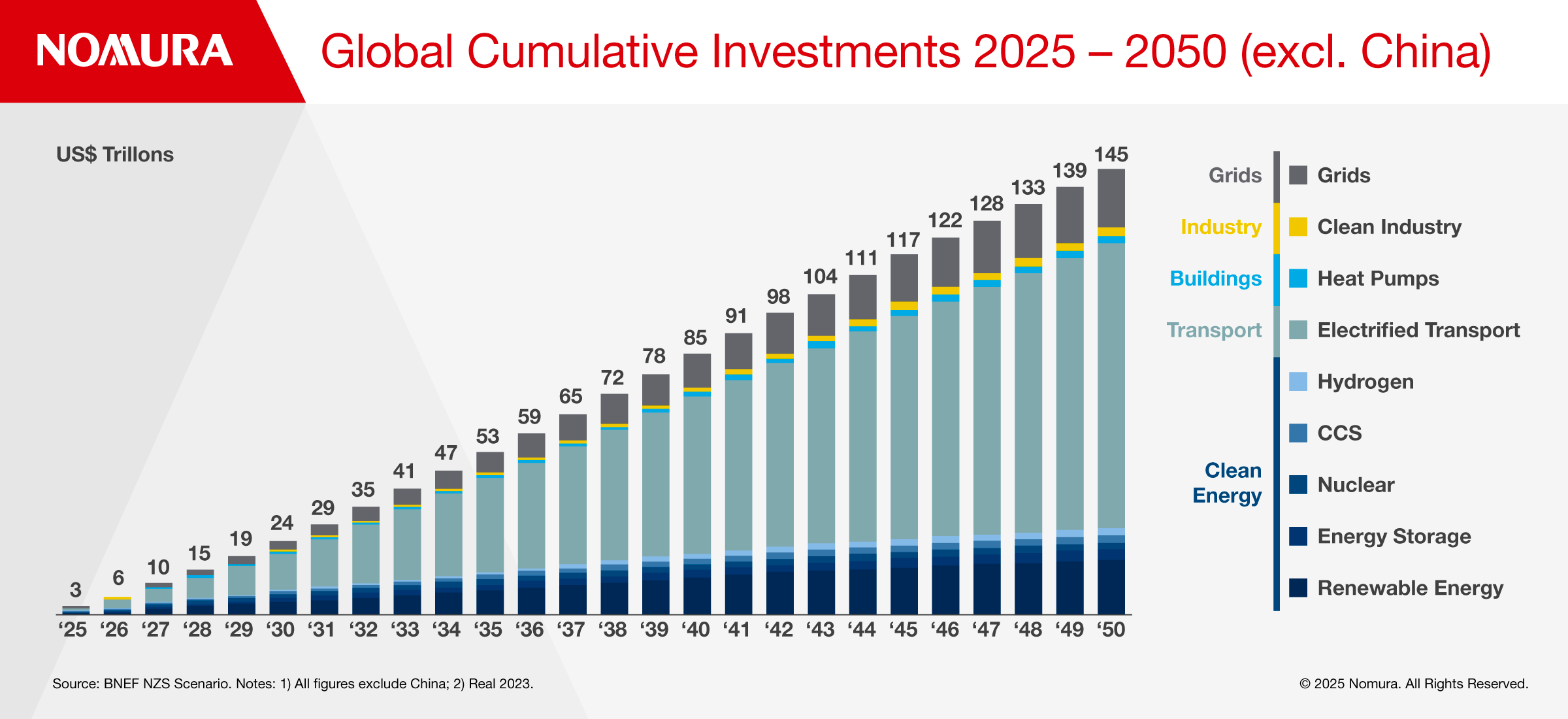

About $150 trillion of capital is required by 2050 to fund the global energy transition and despite recent inflationary challenges and slower progress from countries such as the US, there is a great deal of optimism about investing into green technologies.

While the cost of capital for renewables has reset at a higher level amid inflationary forces – a 200bps rise since 2021 with most of that increase coming since the third quarter of 2022 – executives viewed this as a sign that speculative capital is making way for long-term investors who see the inevitability of transitioning to sustainable energy systems.

There are reasons for optimism in all major markets including Europe, China and the US.

EUROPE – ENERGY INDEPENDENCE

Europe is committed to eliminating its dependence on Russian gas via its REPowerEU plan, which is accelerating the region’s decarbonization ambitions. Imports of Russian gas dropped from 150 billion cubic meters (bcm) in 2021 to 52 bcm in 2024 – with the overall share of Russian gas imports falling from 45% to 19%, according to the European Commission. This intensifying focus on energy security means that the bloc continues to roll out renewable energy more quickly, with almost half (47%) of electricity in the EU now coming from renewables. Installed wind and solar capacity has increased by 58% cumulatively between 2021 and 2024.

Russia’s invasion of Ukraine has also caused wider tremors among neighbouring countries, prompting them to prioritise defence spending in order to become more self-reliant in the event of a wider conflict. Germany has announced plans to nearly double its defence budget to €650 billion ($764 billion) over the next five years. Companies such as Fernride have spotted a trillion-dollar opportunity to create regional champions in the sphere of automated armoured vehicles in combat zones, at ports and for freight logistics on public roads. Fernride’s AI-based human-in-the-loop technology means that one driver can operate up to 50 trucks remotely to address massive shortages of commercial drivers (400k) and trained soldiers (300k).

Europe has also made considerable progress on installing electric vehicle (EV) chargers. Take Germany, - the bloc’s biggest country - where more than 145k public charge points have been installed and a forecasted slowdown in EV car sales has not materialised.

EUROPE – REGULATORY LEADER

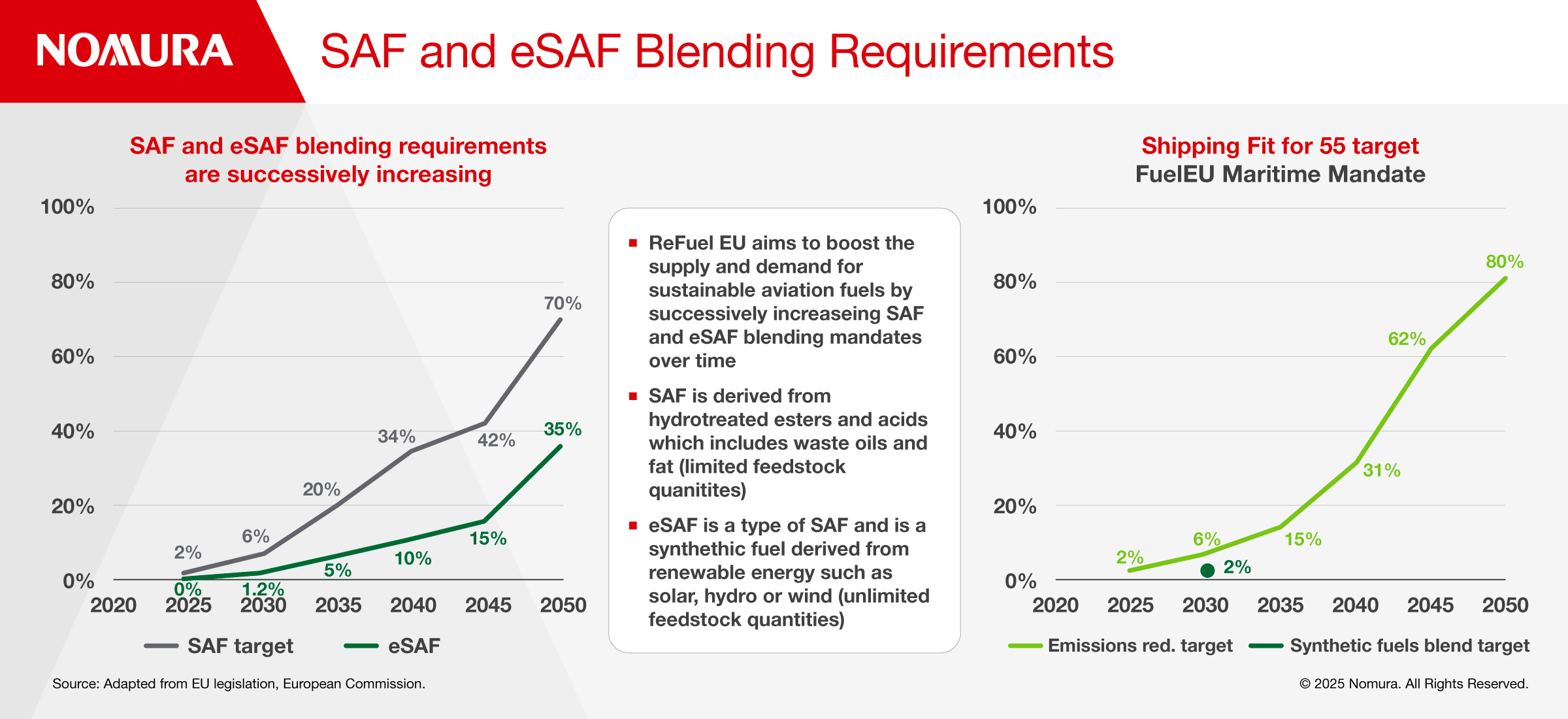

Europe has also used its strength in regulation to encourage the adoption of green technologies across multiple sectors as illustrated by ReFuel EU, which aims to boost the supply and demand of sustainable aviation fuel (SAF) by increasing SAF and eSAF mandates over time. SAF is derived from hydrotreated esters and acids while eSAF is a synthetic fuel drives from renewable energy such as solar, hydro or wind.

The FuelEU Maritime Mandate is another example of EU regulation taking a leadership role to drive change. The rules set increasingly strict limits on the greenhouse gas intensity of fuels, aiming for an 80% reduction by 2050 for commercial vessels over 5,000 gross tonnage calling at EU ports. The International Maritime Organization created its own net zero framework earlier this year encompassing a new fuel standard for ships and a global pricing mechanism for emissions.

In stark contrast to these sectors and to emphasise the powerful impact of effective regulation, summit participants cited the petrochemicals industry where regulatory drivers and subsidies are in short supply. Entrenched interests are high, and an oversupply of conventional petrochemicals is keeping prices low, meaning alternatives that carry a green premium struggle to compete with incumbents selling cheaper, higher-emission products.

CHINA – A LOW CARBON INDUSTRIAL CHAMPION

China’s decades-long investment into photovoltaic (PV) technology has paved the way for more affordable solar power across the globe. China’s share in all the manufacturing stages of solar panels (such as polysilicon, ingots, wafers, cells and modules) exceeds 80%, more than double China’s share of global PV demand, according to the International Energy Agency.

As a result, the levelized cost of PV solar power – which includes the cost of building the plant – has declined by 88% over the past 15 years; removing green premiums has been key to mass adoption.

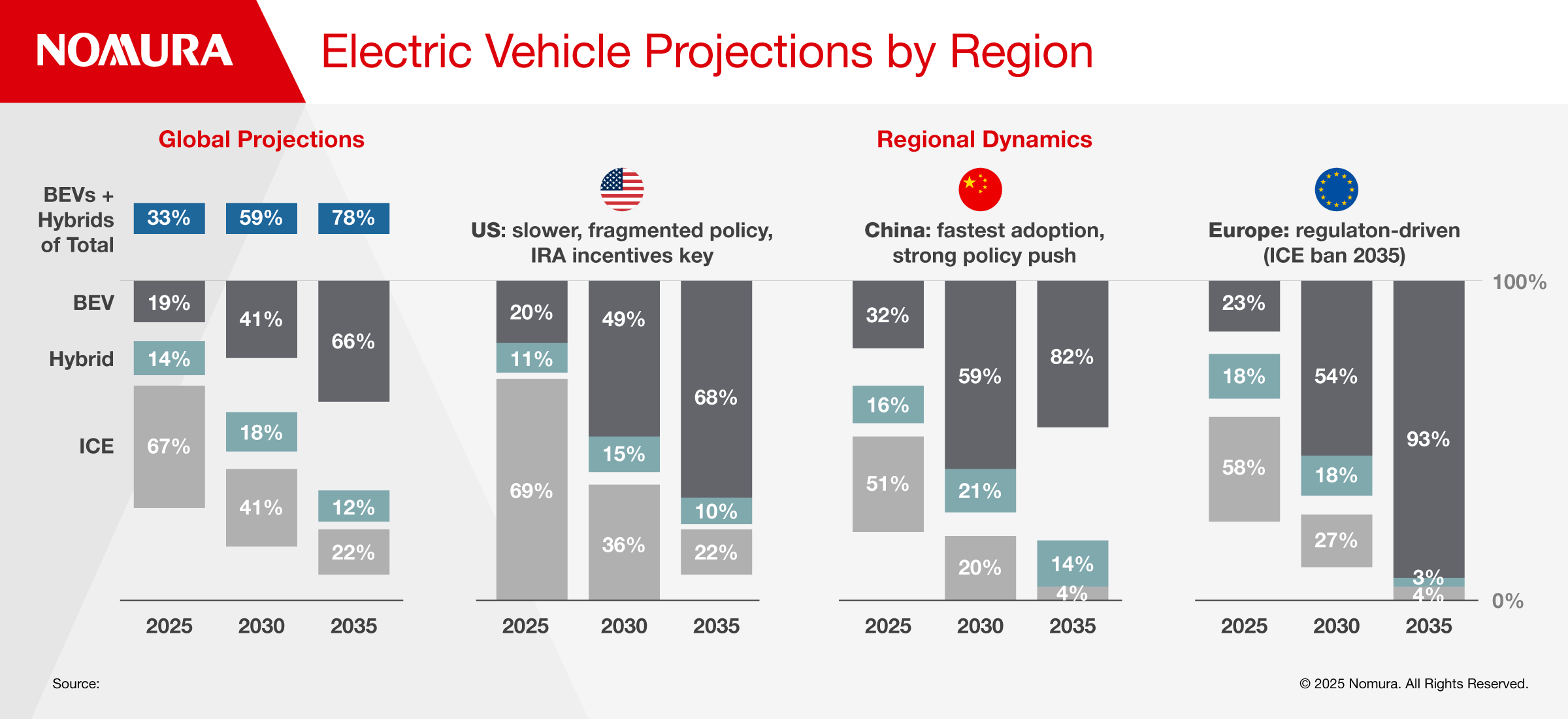

In addition, China’s rapid rollout of battery technology for EVs has accelerated adoption at home and abroad.

The chart below shows that more than half of China’s vehicles will be electric by 2030.

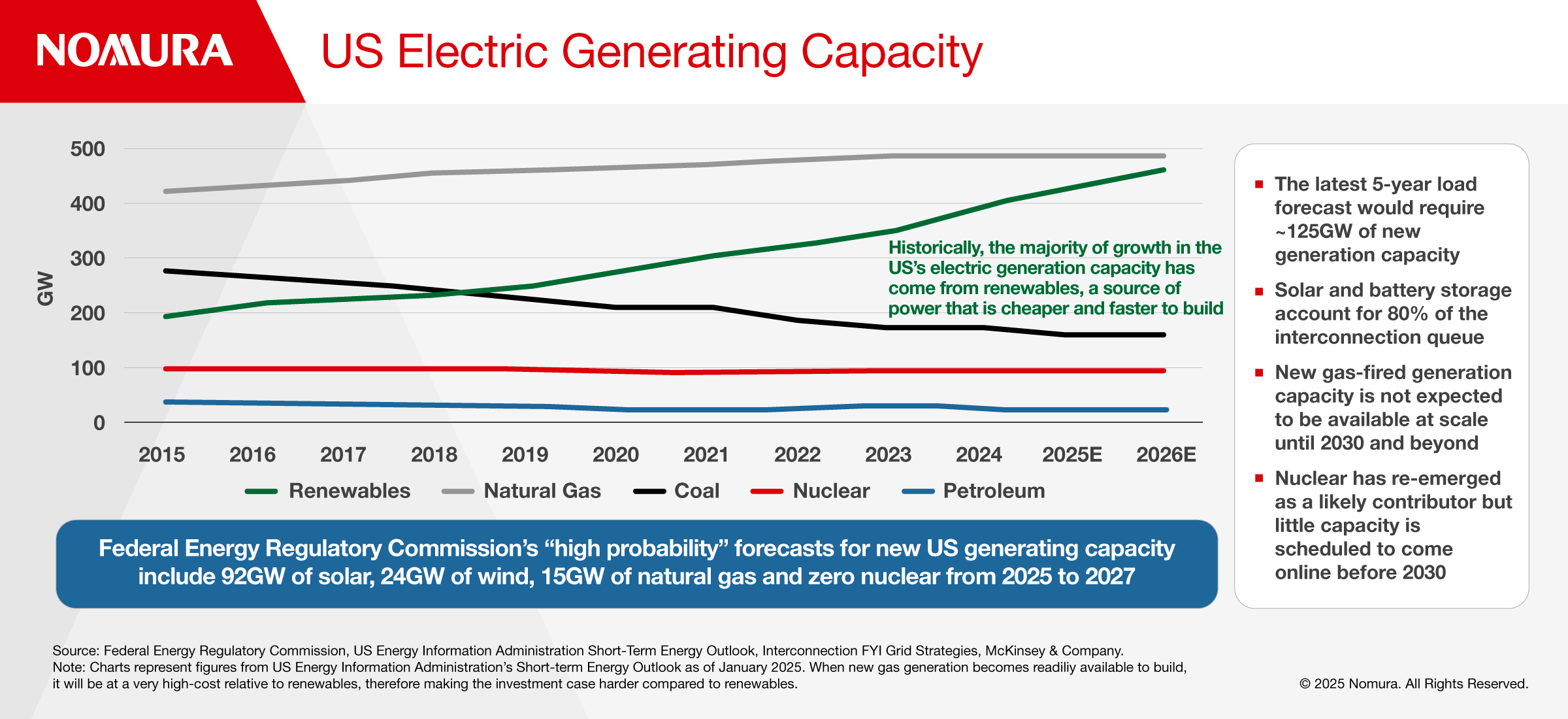

US – MARKET FORCES DRIVE CAPACITY UPGRADES

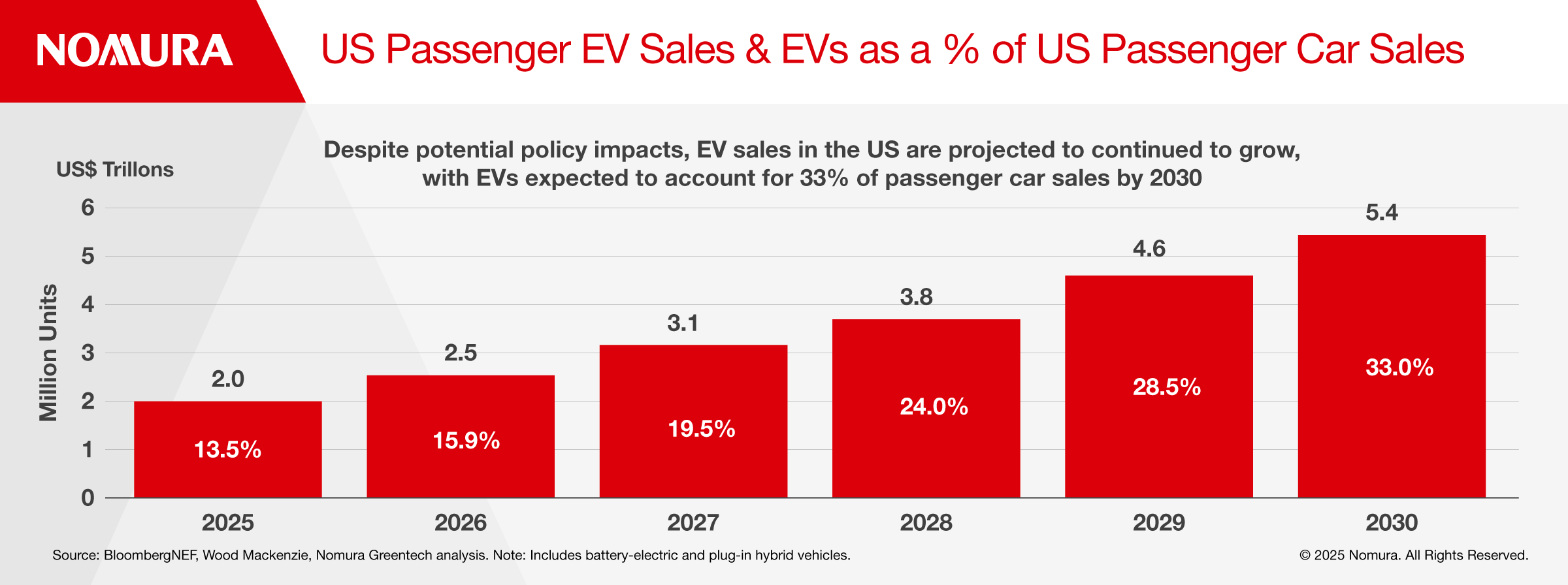

While the US renewables market is contending with political headwinds arising from President Trump’s One Big Beautiful Bill Act (OBBBA) and tariffs on imports of PV panels, aging grid infrastructure and greater power demand from investments in AI data centers could offset these negative effects.

The OBBBA reduces Inflation Reduction Act tax credits for wind and solar but preserves full credits for energy storage and clean firm technologies through 2033. Tariff escalations and geopolitical tensions have intensified supply chain challenges, but as a result, a renewed focus on domestic manufacturing and alternative sourcing has emerged, even across hard to decouple supply chains such as critical components for batteries and PV modules.

High growth in the US power market is projected over the next 15 years as demand continues to outpace supply due to significant growth in sectors requiring near-term power. Over the last two decades, improved energy efficiency for lighting, appliances and heating and cooling meant that the compound annual growth rate for energy demand was about 0.4% per year but the new era of AI, EV penetration and electrification of everything is set to substantially increase demand to 3.5% per year until 2040, according to McKinsey data.

Historically, energy has not been a constraint on computing; even as higher internet traffic increased data center workloads by nine times between 2010-2020, overall energy use stayed flat because of more and more efficient chips. But the AI era is set to turn that paradigm on its head, leading to a 17-64GW shortfall in peak power demand by 2030, which will likely require fast-built solar and battery storage to fill the gap.

Every US region is in need of energy infrastructure upgrades and replacements to minimize impacts of congestion and increase reliability. All three major components of the electric grid - generation, transmission and distribution - have an identified investment gap, which is projected to grow to a cumulative $197 billion by 2029, highlighting significant vulnerabilities in existing energy infrastructure. The US utility industry expects to see about a ~1.6x increase in capital expenditures into critical infrastructure over the period of 2026-2030 representing $1.3 trillion in capex from 2026-2030.

In short, executives increasingly see a-multi-speed transition playing out with China using its industrial scale to take the lead on renewables and EVs while Europe uses the stick of regulation and energy independence to advance the green transition. The US faces short term challenges, yet it has already laid strong foundations to build resilient systems for an electrified, digital future.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.