Economics | 3 min video December 2018

Economics | 2 min video | December 2018

Economics | 2 min video | December 2018

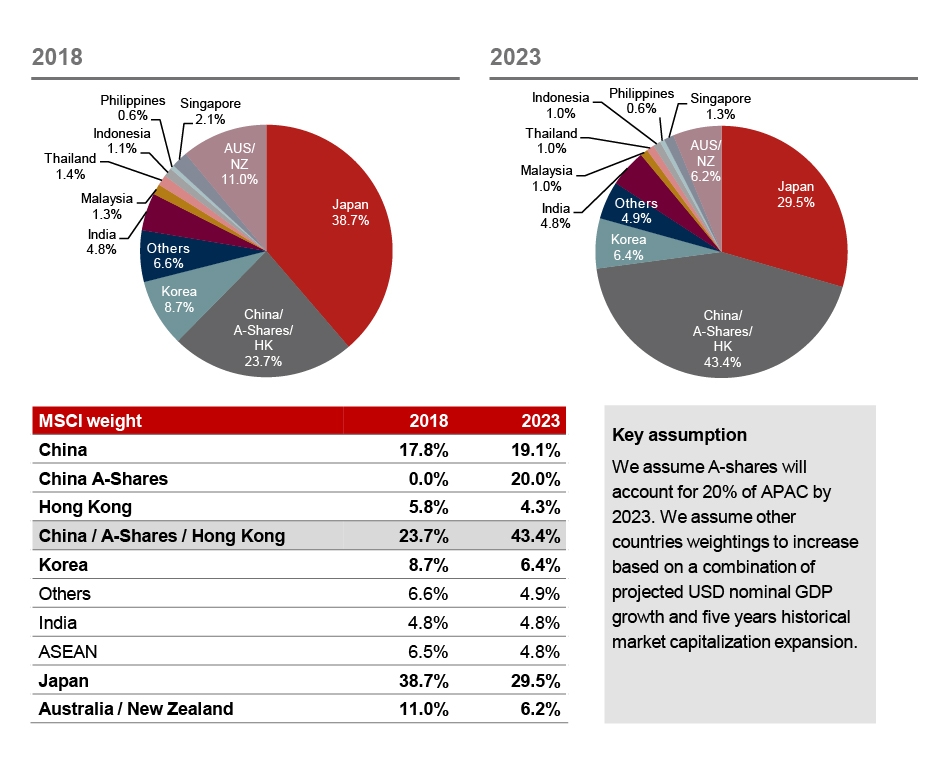

As we approach 2019, we see a slowdown in economic growth rates across the region, but we can also expect some structural changes in the way investors view Asia, such as the China market. Traditionally, investors have looked at China in the context of Asia ex-Japan. However, our projections suggest China will be the biggest component of Asia-Pacific, superseding Japan as the biggest market in the region by 2023.

Other possible changes in 2019 include how indices view China, specifically, MSCI A-Shares. Within 18 months, we expect the weighting attributed to MSCI A-Shares to go up fivefold. Simultaneously, we also expect investors to be quite defensive given the slowdown in economic growth rates. Because of this, we see investors prioritizing dividends as well as companies with strong balance sheets and corporate governance reform.

In all three big markets in Asia, namely China, Japan and Korea, we see some attractions. This is particularly visible in Korea, where one of the largest pension funds has now embraced the stewardship code. Additionally, in markets such as China, the largest dividend payer globally is China Mobile, which is surprising for many global investors. For that reason, we expect income-seeking investors will tend to favor putting money to work in Asia markets.

To read the full 2019 outlook on China strategies, click here.

Head of Asia ex-Japan Research

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Economics | 3 min video December 2018

Emerging Markets | 0 min video December 2018

Central Banks | 1 min video December 2018