As ESG investing gains momentum, we explore the factors that point toward this being more a genuine lasting shift than a short-lived fad

Momentum in ESG investing has accelerated in recent years, driving record flows into ESG investments, impressive valuations for companies in ESG sectors and thousands of new signatories to the UN Principles For Responsible Investment (PRI)

ESG investments coming from institutional investors are focused on long-term investing and many ESG focused investment funds now command a performance premium, not penalty

Governments have signaled aggressive stances toward combating climate change through incentives, infrastructure investment and regulations globally, creating tailwinds for further growth

We anticipate continued record inflows to the space and greater ESG integration in financial reporting all while improvements in sustainable technology further drive product innovation and improve quality of life

This article was produced in collaboration with

The trend over recent years is impossible to ignore: ESG investing has been gathering steam. There have been record flows into ESG investments, companies in ESG sectors have registered impressive valuations and thousands of asset managers and owners have signed on to the UN Principles For Responsible Investment (PRI). Environmental sectors are outstripping growth in the overall economy and ESG-focused funds are outperforming their counterparts. There is a convergence of driving factors that already point to this being more a genuine lasting shift than a short-lived fad.

Crossing the Rubicon

In financial markets, the notion of a performance penalty for ethical investing is now being superseded by recognition of a performance premium. And last year, three of the world’s biggest pension funds joined the ranks of managers which have decided to put ESG metrics at the heart of their strategies.

“It’s now crossed the Rubicon to become a fundamental precept of investing going forward. ESG is going to become as important as EPS in investors making decisions on public equities and fixed income securities,” says Jeff McDermott, Head of Nomura Greentech.

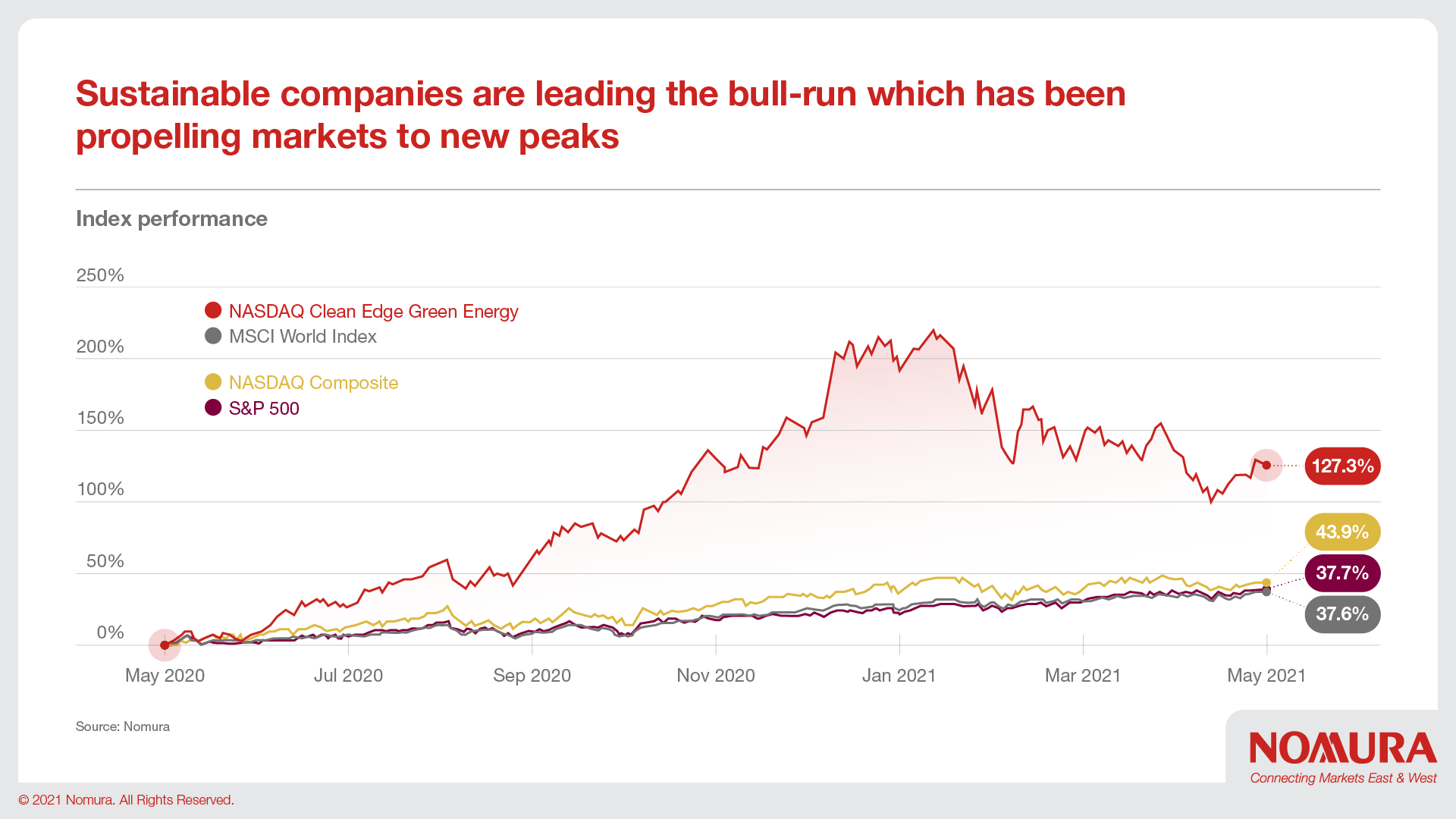

Sustainable companies are leading the bull-run which has been propelling markets to new peaks, as evidenced by the NADSAQ's Clean Edge Green Energy Index more than tripling between March 2020 and March 2021. Companies in sectors such as renewable energy have ridden the secular wave of the structural shift to sustainability and stood out with the value they have created. Further underpinning this growth is innovation, which is continuing to deliver technological advancement at lower costs.

And across the globe, there is growing policy and regulatory momentum pushing in the direction of ESG. The Biden administration has put clean energy and sustainability at the heart of its agenda and its ambitious infrastructure plan. Similarly, the EU Green Deal is the centrepiece of its economic recovery efforts from the pandemic, while Europe is also leading the way in regulating ESG investing. In Asia, Japan and South Korea have followed the US and EU in announcing plans to achieve carbon neutrality by 2050, with China aiming to reach the same target a decade later.

Support for climate action has even begun to emerge from some unexpected quarters. In March, the American Petroleum Institute announced it would back a carbon tax, and the following month, America’s largest coal miner’s union said it would back Biden’s shift to renewable energies.

From doing good to doing better

As has been the case with technological developments in a broad spectrum of arenas, initial advancements in fields such as renewables, clean energy and carbon capture were driven to a significant extent by government-led initiatives. This undoubtedly helped entrepreneurs and investors see the viability of these technologies and the potential in related industries.

The private sector is now carrying this torch forward and there are already numerous profitable companies which have built business models around the ongoing drive for sustainability. These companies and industries have continued to thrive even during times when the political and regulatory landscape has been less favourable to them.

Where ESG investing was once seen more as a hedge against the possible repercussions of a policy shift or a willingness to give up some returns for the sake of the greater good, it has transformed to an imperative that makes economic sense.

There is growing recognition that inaction on the ‘E’ of ESG is simply not an option and would have devastating economic consequences. When Japan’s $1.56 trillion Government Pension Investment Fund, the $275 billion California State Teachers’ Retirement System and the UK’s $90 billion Universities Superannuation Scheme issued a joint statement in March 2020 committing to a partnership on sustainable investing, they did not mince their words.

“If we were to focus purely on short-term returns, we would be ignoring potentially catastrophic systemic risks to our portfolios,” they declared, pointing to Moody’s Analytics estimate that climate change alone could destroy $69 trillion in wealth worldwide by 2100.

However, this suggests they are willing to forego a certain amount of near-term gains for the sake of a sustainable economic system that could still deliver returns in the future. The evidence is increasingly clear that this is no longer an either-or choice that needs to be made.

Indeed, top-performing ESG companies in their sectors are producing superior risk-adjusted returns and alpha, and fund managers who screen for top-performing ESG companies in their portfolios are outperforming those who don’t.

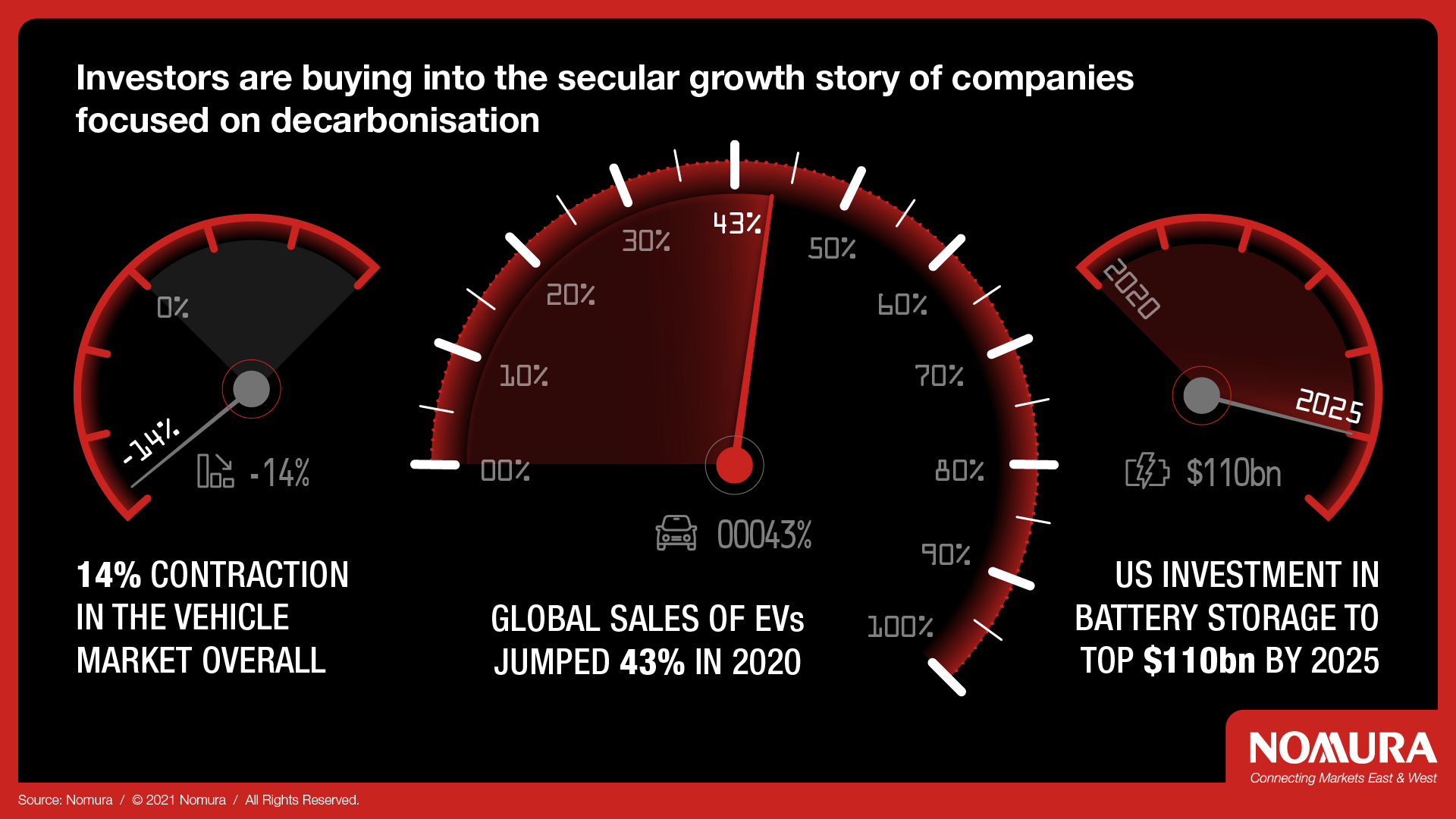

One of the reasons for this outperformance is that investors are buying into the secular growth story of companies focused on decarbonisation. And the evidence underpinning the story is strong. Globally, sales of EVs jumped 43% in 2020, compared to a 14% contraction in the vehicle market overall. Meanwhile, investment in battery storage in the US alone is predicted to top $110 billion from 2020 to 2025.

McDermott suggests that there may also be other factors at work, “It may be that management teams focused on having a diverse workforce and treating their staff well will have a more productive workforce. A company that looks at environmental risk and stakeholder issues is probably one that has greater brand value. It may also be good at capital allocation, talent acquisition, M&A deals and other drivers of profitability.”

Genuine corporate commitment or greenwashing?

Nevertheless, sustainability-driven industries and ESG-driven investing are still in their nascent stages; there remains much wood left to chop. Despite moves afoot towards creating universally recognized definitions and standards, for now, ESG remains a very broad church. Investing strategies run the gamut from avoidance of fossil fuel and high-carbon companies, to selecting only ventures engaged in fields such as renewables or other specifically green tech that will ride the wave of sustainability. Currently there is nothing preventing a company or fund from using the term ESG or issuing a grandiose mission statement declaring their sustainable credentials, but taking little or no quantifiable action to make that a reality. But that is beginning to change.

Progress is being made on rules and standards for ESG investments and companies, which will be important elements in maintaining momentum and preventing greenwashing, and there is more on the cards.

An EU directive mandating greater transparency from ESG funds came into effect in March. And in the US, the SEC has determined that carbon emissions and climate risks are a material concern for investors and, much like a company’s financial condition and operating performance, should be disclosed to investors. The Biden administration views investor cooperation as paramount for its net-zero emissions goals, and increasing disclosure requirements for carbon emissions is aimed at making investor cooperation easier and more transparent. Mandatory disclosures would replace a voluntary system that some companies participate in, but others shun or only partially participate in, and make for easier comparisons between firms for investors. The SEC is moving quickly to implement this rule change, including by soliciting feedback from industry over the past month, and could finalize rule changes by October, 2021.

Meanwhile, five of the major organizations involved in setting standards for sustainable investing - CDP, the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board (SASB) – issued a “Statement of Intent to Work Together Towards Comprehensive Corporate Reporting” in September.

It is worth remembering that standardized accounting reporting requirements are less than 50 years old. It will likely take time until universally-accepted standards for ESG are recognised and enforced, but current trends point to them being on their way.

Once data on ESG metrics are standardised, it can be measured and companies compared to their peers on environmental attributes such as carbon emissions and water usage as they are now ranked on total five-year returns. The day may be nearer than we think when management compensation is linked to those metrics.

In the immediate future, it is probable that there will be more moves like that from food group Danone, which last year began publishing its “carbon-adjusted EPS,” based on its estimated cost per share of its emissions subtracted from its standard EPS.

And technological advancement is already a game changer for sustainability. Ten years ago, few imagined that renewable energy would by now be cheaper than that generated from fossil fuels. As the technology and systems required for de-carbonisation continue to progress and become cheaper, ESG investments will in turn become increasingly profitable and help improve quality of life.

Government policy: pandering or addressing climate change?

Much of the initial enthusiasm around ESG was triggered by public initiatives such as the American Recovery and Reinvestment Act (ARRA) of 2009, and the subsequent establishment of state-level green banks, an idea that spread to the UK, Australia, Japan and other nations. Those programs, while ground-breaking at the time, are dwarfed by the Biden administration’s potential $2 trillion clean energy-focused stimulus program and the €1 trillion European Green Deal.

Meanwhile, the global pandemic delivered a sharp reminder of our interconnectedness, and the damage it wrought on the economy gave a glimpse of some of the perils that lie in wait if decisive measures are not taken to address climate change.

The UN Intergovernmental Panel on Climate Change estimates that limiting global warming to 1.5°C above pre-industrial levels requires annual investment of approximately $2.4 trillion until 2035 in the energy system alone. That represents about 2.5 percent of global GDP and does not take into account the action necessary in a myriad of other sectors, including construction, manufacturing, mining, air travel and agriculture.

The combination of governments now prepared to walk the walk on combating climate change and the need for huge amounts of private capital to address this era-defining challenge point the future of ESG investing in a clear direction.

No turning back

Record flows into ESG investments are set to continue and the number of companies operating in the space to keep growing, while momentum over the last year for greater integration of ESG metrics into financial reporting and product innovation will carry on building. Just as nobody could have foreseen the myriad of ways ESG has developed and diversified in recent years, the precise nature and path of its progress in the years to come is nigh on impossible to predict. What seems more certain is that this is a shift that will not easily be reversed; a future trend that has already arrived.

Global Co-Head of Investment Banking at Nomura Holdings

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.