Since the start of the Iran war, markets have been focused on whether this energy shock is similar to the 2022 European energy crisis.

Following Russia’s invasion of Ukraine in 2022, European central banks raised rates at an unprecedented pace. This was to combat both rising inflation and, more importantly, the large and persistent second-round inflation effects that were becoming apparent, as the initial energy price shock propagated through the economy.

However, there are fundamental differences between now and then in the euro area and the UK that mean, in our view, the central banks may respond differently to the war in Iran.

The starting points are different

First, the shocks are fundamentally different. The shock from the Iran war is currently only a price shock, whereas in 2022 Europe also faced a supply shock because it had been heavily dependent on gas from a Russian pipeline that was shut off.

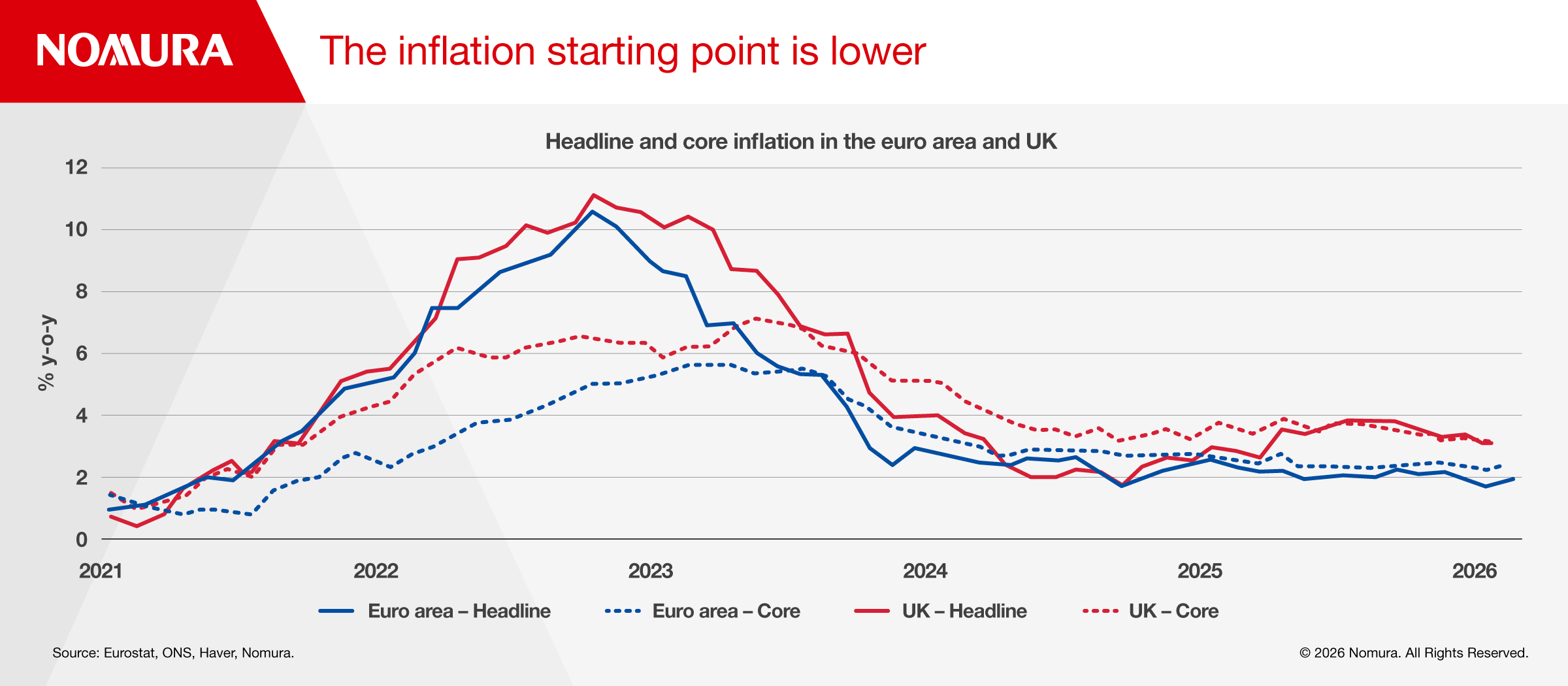

Second, the inflation rate is different now than in 2022, and inflation momentum is also different (Figure 1). In February 2022, HICP inflation in the euro area was 5.9%, and CPI inflation in the UK was 5.5%. Inflation is now lower at 1.9% in the euro area and 3% in the UK as of February 2026, immediately before the start of the Iran war.

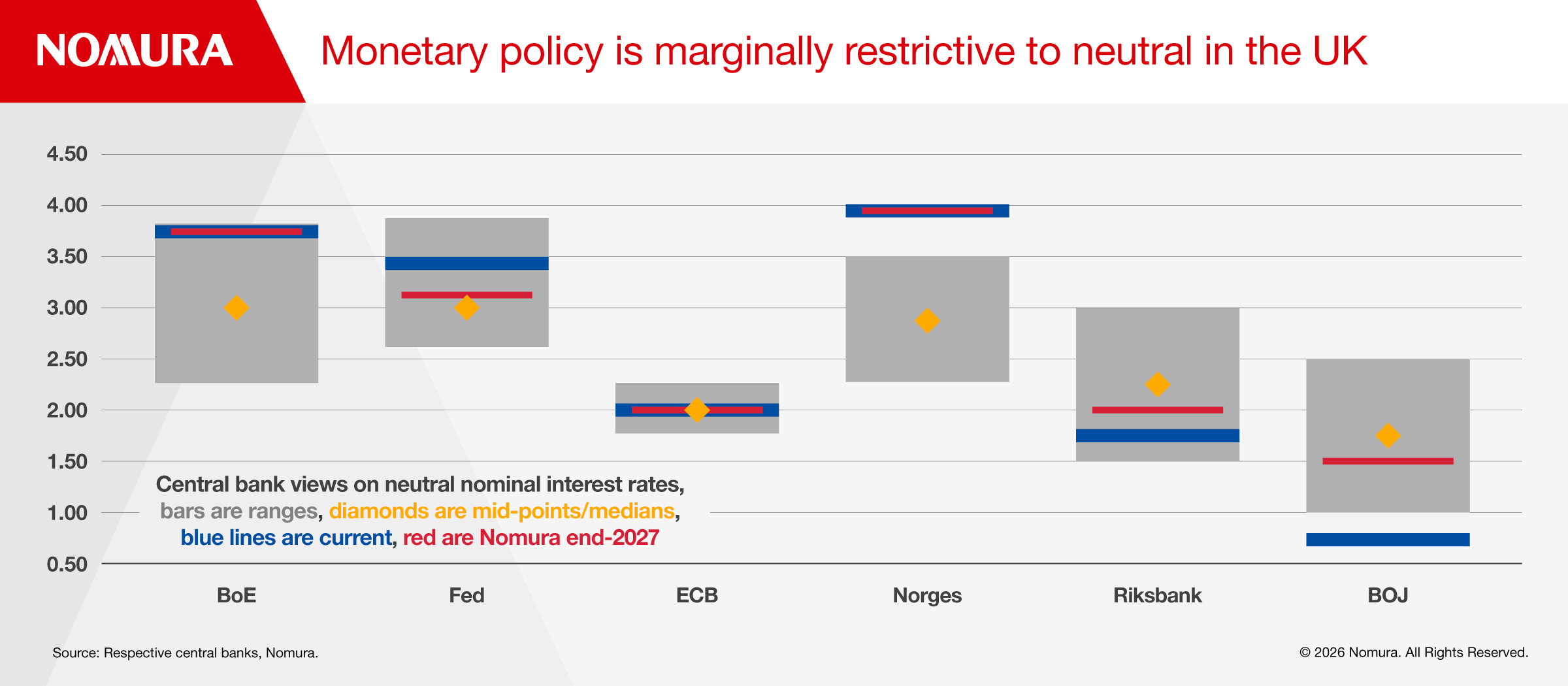

Third, monetary policy in the euro area and the UK is now in a very different place relative to 2022. Monetary policy is neutral in the euro area and marginally restrictive to neutral in the UK, whereas it was meaningfully accommodative in both in 2022. Also, the ECB and BoE were undertaking quantitative easing in 2022. Both are now embarking on quantitative tightening.

It is natural to question whether the ECB and BoE may react differently this time around. Markets are pricing both central banks to respond almost identically to the energy shock from the Iran war, and front-end rates for both banks have tracked one another closely. The ECB is widely expected to hike rates two or three times and the BoE one or two times by December 2026.

However, in our baseline, both the ECB and BoE are likely to leave rates unchanged through the fourth quarter of 2027. This assumes that events will unfold in such a way that the energy shock from the war in Iran will have a limited impact over the medium term.

That said, in a scenario where the spot price for Brent crude oil were to remain in the $95–$100 per barrel range until the ECB’s June meeting, we believe the ECB would raise rates by 25 basis points in June and then again in September. We would also expect the BoE to hold at 3.75% through the fourth quarter of 2027, as concerns over fragile GDP growth are likely to take center stage.

Energy price pass-through

Across European nations, the first stage in the pass-through of higher oil and gas prices to inflation is via prices at the pump. The vehicle fuel weighting in the UK’s inflation basket is smaller than in the euro area (2.6% versus 3.8%), so higher pump prices affect inflation less.

A second direct impact of higher energy costs is via household energy bills. Here, too, the impact on UK households may be smaller, and more delayed, than the typical household in the euro area.

Following these direct effects (which monetary policy can do very little to affect) come indirect effects on high-energy intensity components of non-energy inflation — such as food (partly due to fertilizer costs), transportation (airfares, for example), hotels, and restaurants — where higher input costs tend to be passed through with lags that depend on the degree to which energy prices have been hedged.

Although the UK may fare better than the euro area for direct inflation effects, indirect effects are more of a concern in the UK.

After direct and indirect inflation effects come second-round effects. These are what central banks are most concerned about, and they are also more influenced by central banks’ interest rate policy. In the March monetary policy meetings, both the ECB and BoE expressed that second-round effects would be monitored closely.

The state of the labor markets

When people think of second-round inflation effects, the focus is often on the wage channel, where higher spot inflation pushes up inflation expectations and compels workers to demand higher wages. The risk is that we enter a wage–price spiral, as was the case in 2022. As far as the ECB and BoE are concerned, the persistence of services inflation following the 2022 European energy crisis was largely due to second-round inflation effects from higher wages.

The strength of the labor market is therefore an important determinant for second-round inflation effects. However, there are important differences this time.

The underlying fundamentals of the labor market suggest workers have less bargaining power to demand higher wages, so we are potentially less at risk of entering a wage–price spiral.

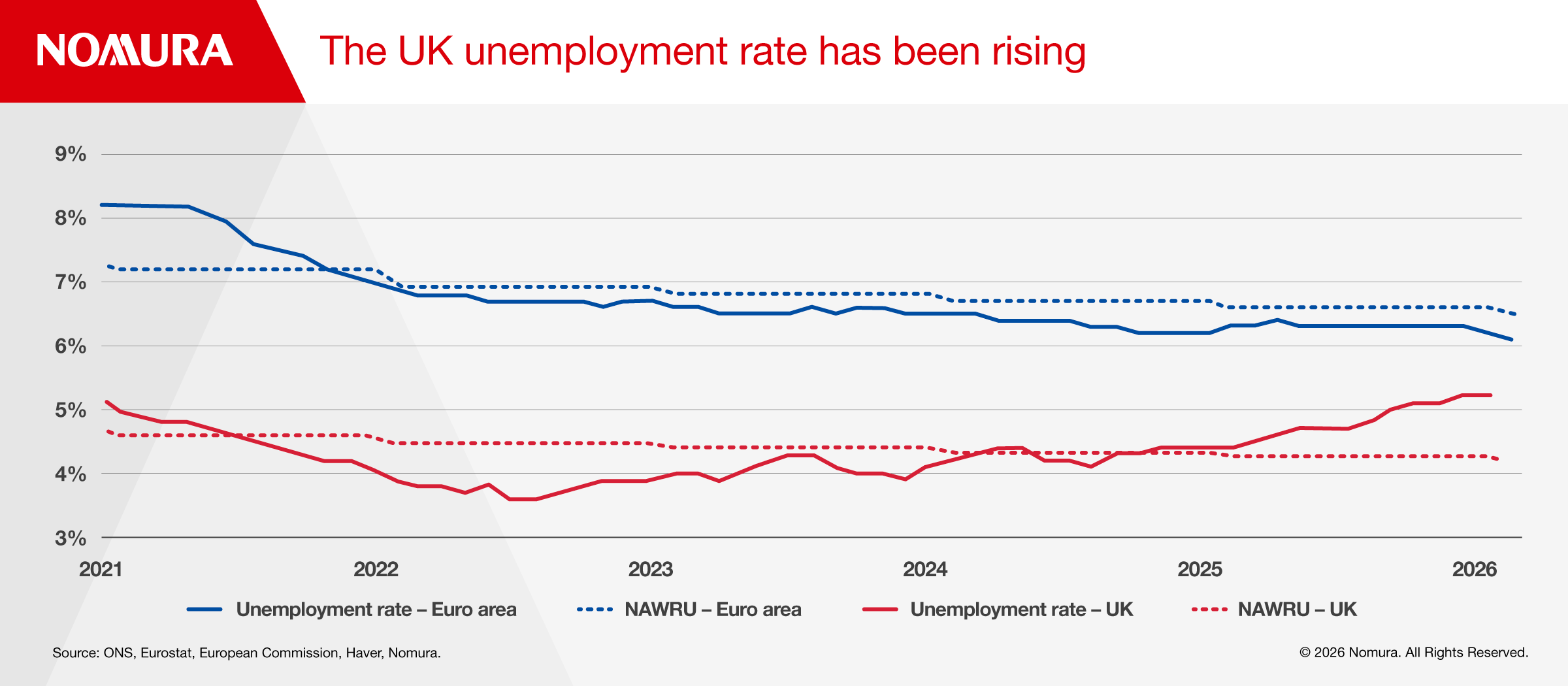

In the euro area, the unemployment rate was 6.2% in February 2026 (Figure 2), the lowest recorded in the bloc since the introduction of the euro. In the UK, meanwhile, the unemployment rate was 5.2% in January 2026, up 1.6 percentage points since a recent low of 3.6% in July 2022. This would suggest that the euro area labor market is tight now, as it was in 2022, whereas the UK labor market is exhibiting meaningful slack, unlike in 2022.

Although the labor market in Europe is looser than it was in 2022, the data also indicates that the labor market is, at present, tighter in the euro area than in the UK, so the bargaining power to demand higher wages is likely higher in the euro area than in the UK. Therefore, the risk of second-round inflation effects through the wage channel are slightly stronger in the euro area than in the UK.

The ECB is more likely to raise rates

Compared with the euro area, the UK has a marginally restrictive-to-neutral monetary policy (Figure 3), a softer labor market, and softer economic growth.

Also, consumer inflation expectations appear higher in the UK than in the euro area, possibly because CPI inflation in the UK has still not returned to target, whereas euro area HICP inflation has hovered around the ECB’s target since May 2025. Therefore, inflation expectations in the UK appear most at risk of de-anchoring.

Despite market pricing for both the ECB and BoE that suggests they will respond in practically the same way, we believe that, if either is to act, the ECB is more likely than the BoE to raise rates in response to the energy crisis from the Iran war.

To read the full report, click here.