The US auto industry and related supply chains have borne the brunt of President Trump’s tariff fusillade, with the full effects on the industry’s global sourcing model yet to completely manifest. Reviewing global auto sales in 4Q24-1Q25, volume growth has run ahead of Nomura’s earlier estimates. The outperformance was almost entirely led by China, where government scrappage schemes and local original equipment manufacturers (OEMs) prioritized volumes over margins, leading sales volume to overshoot estimates by 8%.

Automakers are adapting as they face tariff headwinds in the US

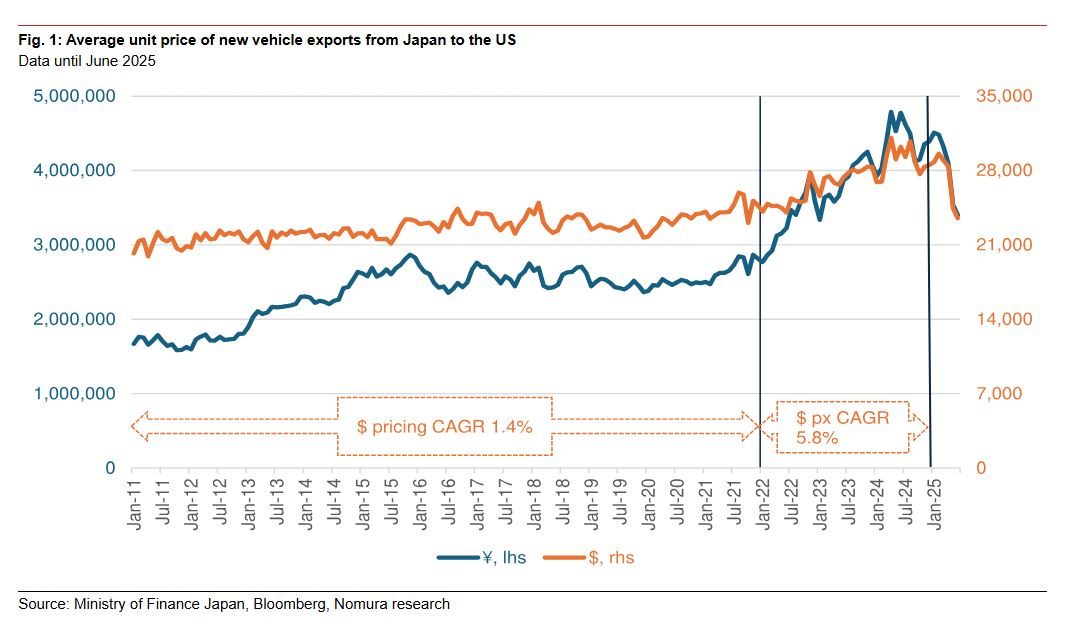

Unsurprisingly, most of the key changes to our views compared to six months ago are centered on the US. US auto sales saw an early boost in 2025 as buyers rushed to avoid expected tariff driven price hikes, but this demand pull-forward will likely slow sales later in the year. Automakers face ongoing challenges from new and higher tariffs, potential supply chain disruptions, and rising input costs, especially as President Trump’s policies emphasize US-centric reshoring and higher barriers for imports, even from Mexico and Canada. But, Japan’s export data show early signs that automakers are starting to adjust to this new reality by offering less expensive versions of their models, so they can pass some of the extra costs to buyers while still keeping cars affordable overall.

Auto loan delinquencies are rising, particularly among lower-credit-score, used car buyers, as higher prices and interest rates strain affordability. Meanwhile, the rollback of EV incentives and potentially looser emissions standards may stall EV adoption, though it may benefit traditional automakers that are struggling to keep up with federal emissions rules. Trump’s focus on reshoring supply chains to the US specifically makes a full-fledged US-Mexico-Canada Agreement deal less likely.

EV momentum drives China auto market

OEMs’ focus on shipment and market share in exchange for increasing demand will likely drive further volume growth for China’s auto market in 2025. In a fiercely competitive market, price cuts and technology upgrades, such as smart driving functions, are the levers OEMs are pulling to gain market share.

Considering EV players are now setting pricing benchmarks for China’s overall auto market, actively pursuing evolution and delivering new models, we believe they will gain market share from ICE players. The trend of trading price for market demand is expected to continue, and the sector will see further growth.

While market leaders enjoy competitive advantages and further strengthen their positions, smaller players struggle and face more challenges. Further EV penetration is likely, and competition will remain intense. We expect more M&As and partnerships within the China auto market over the next 1-2 years.

Hybrids and EV lead South Korea demand

In Korea, we continue to believe the country’s auto demand will be flattish at 1% in 2025E. However, momentum will likely weaken for the rest of the year on a normalizing base. Supplies of hybrid vehicle (HV) models, which represent 34% of Korea’s new vehicle sales YTD 2025, will lead the country’s auto industry with a 20% projected sales growth in 2025E. EVs are also expected to post high sales growth similar to that of HV in 2025, in light of the series of new models and price discounts.

Mixed prospects for auto markets in Indonesia, Thailand, and India

Indonesia’s auto market outlook remains weak due to tight lending standards, limited policy support, and new local taxes. Despite a brief 5% uptick in April 2025, overall auto sales have contracted sharply since mid-2023, and new government policies offered little direct support for the sector. With fiscal priorities focused elsewhere and new local taxes dampening sales in key provinces, a significant market recovery in 2025 appears unlikely.

We expect Thailand to witness its third consecutive year of decline. Although the pace of decline has slowed, ongoing weakness is driven by strict auto loan lending standards and a high ratio of nonperforming auto loans, dampening prospects for a near-term recovery.

India is expected to see improved 5% growth in FY26/3E, supported by lower taxes and interest rates, strong SUV demand, and rising EV adoption. While near-term demand is weak due to underlying slow consumption demand and some financing challenges for lower-end consumers, factors such as lower income taxes and reduced interest rates will support demand in FY26/3E and the improvement will be evident by September.

For more on our sector projections, read our full report.