Humanoid robotics is entering a transition phase from technical demonstration toward early commercialization, driven by advances in physical artificial intelligence, declining component costs, and expanding industrial deployment. While public attention often centers on AI capability, we believe execution economics – manufacturing scale, supply-chain integration, and deployment readiness – will ultimately determine the winners.

As a result, the competitive landscape favors system integrators with capital endurance, industrial testbeds, and cost-down discipline, rather than pure-play technology innovators alone.

Competitive landscape: industrial scaling archetypes

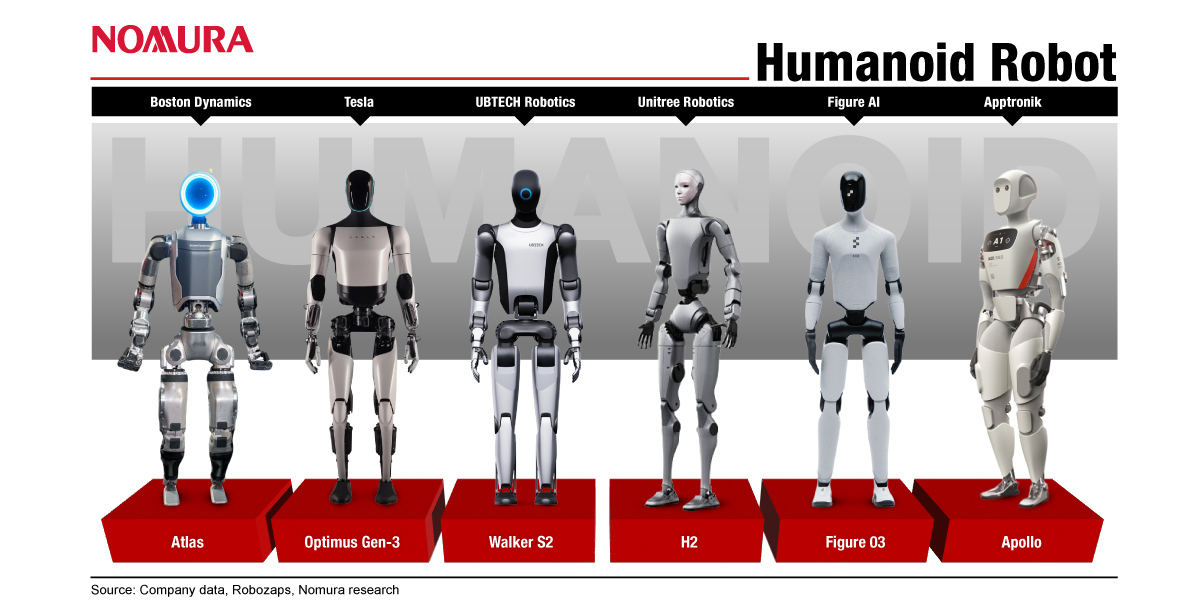

The global humanoid landscape is consolidating around three distinct player groups – automotive original equipment manufacturer (OEM) system integrators, Chinese cost- and deployment-led manufacturers, and humanoid specialists focused on frontier AI and control innovation.

As the industry transitions from prototype demonstration to industrial rollout, we expect consolidation around platforms that secure system-level integration, manufacturing discipline, deployment access, and capital endurance. We believe competitive advantage will be determined less by AI novelty and more by the ability to standardize hardware, compress costs, and scale repeatable production – structurally favoring players with existing manufacturing infrastructure and internal deployment ecosystems.

The 50/50 hardware-software paradigm and pivot to Robot-as-a-Service

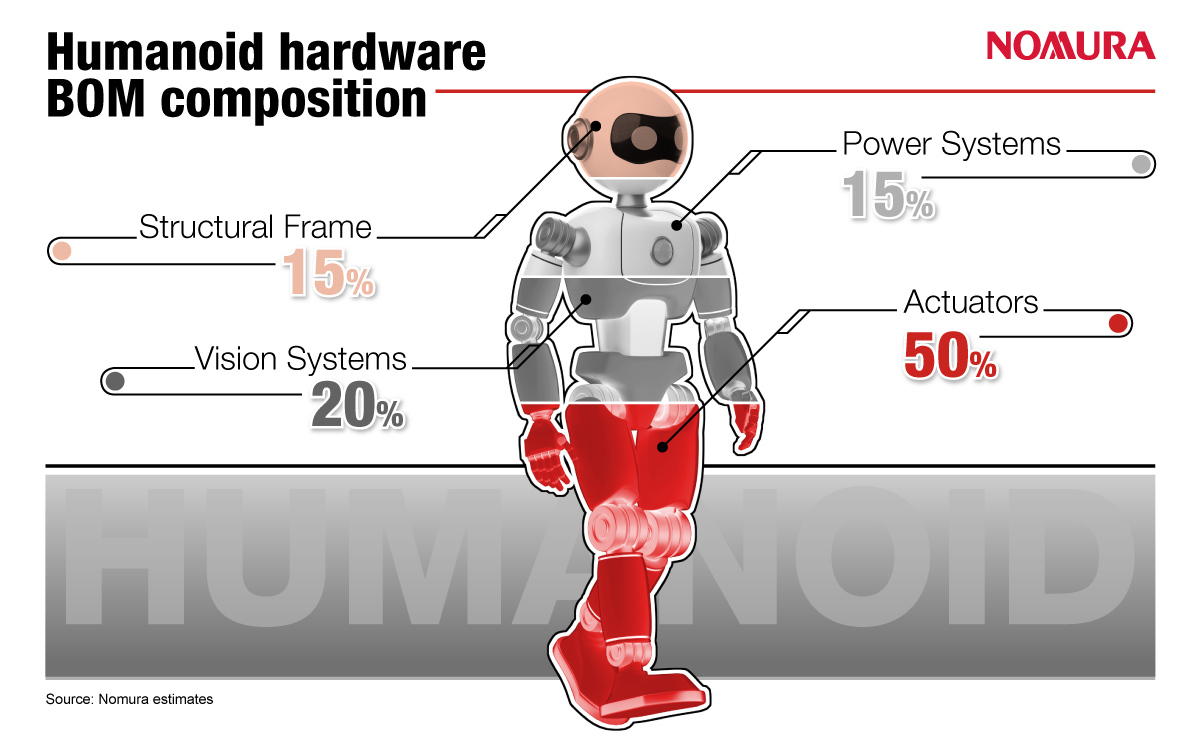

Humanoid economics remain dominated by the execution layer, where actuators and motion systems account for about half of total hardware bill of materials. This hardware segment is strategically prioritized toward mobility, with actuators serving as the primary cost driver while vision systems, power systems and structural frame follow faster commoditization trajectories due to automotive and consumer electronics spillovers. As degrees of freedom (DoF) increase, the non-linear complexity of high-torque motors and harmonic drives solidifies hardware, becoming the initial economic bottleneck.

Conversely, the long-term value proposition is shifting toward a 50/50 hardware-software parity, as the “intelligence” segment increasingly dictates total system lifecycle costs. The rise of Physical AI – requiring continuous large-scale data processing and model maintenance – is driving the industry toward Robot-as-a-Service (RaaS) models. This transition allows manufacturers to offset front-loaded hardware expenses with high-margin, recurring subscription fees, effectively monetizing the software stack through ongoing “intelligence” updates rather than one-time sales.

The three key players

In the early stage of the humanoid product cycle, we believe OEMs are structurally better positioned than component suppliers, as value creation is driven by system integration, deployment access, and balance-sheet capacity rather than standalone component performance. Consistent with past technological transitions such as early EVs, pricing power and learnings benefits are accrued first to platform owners, alongside internal demand and manufacturing scale, while suppliers face a slower volume ramp-up and delayed margin expansion.

Chinese robot manufacturers are backed by strong manufacturing capability and policy-driven tailwinds, enabling them to accelerate product development. We believe Chinese humanoid players will lead in mass-production timing in 2026, primarily because many designs intentionally trade off full anthropomorphic fidelity – such as adopting wheeled bases or simplified, non-dexterous hands – in favor of architectures that are easier to manufacture, scale more quickly, and achieve lower unit costs. However, we see increasing constraints on their overseas penetration amidst rising US-China tensions, which limit access to leading-edge AI chips.

Humanoid-focused specialists play a critical role in advancing Physical AI, partnering through rapid software iteration and early integration of frontier AI models. Their organizational agility allows them to move quickly across perception, planning, and task-specific autonomy. They leverage flexible partnerships with frontier AI and compute leaders such as OpenAI, NVIDIA, and Microsoft to integrate next-generation models into robots on short iteration cycles and increasingly collaborate with European automotive OEMs to deploy robots in industrial environments. However, unlike automotive OEMs, they typically lack manufacturing infrastructure, balance-sheet capability, and long-cycle quality control systems required for large-scale deployment in industrial environments.

While competition is currently fragmented, we believe the landscape will ultimately consolidate around a small number of players that secure the “Operating System and platform layer” of Physical AI.

Scaling trajectories: validation vs industrial ramp

The global humanoid race is entering a transition phase from pilot validation (2026F) to structured industrial ramp (2027-28F). While most leading players target initial mass production between 2026 and 2027, the credibility of long-term volume targets diverges materially depending on manufacturing infrastructure and deployment access.

We think 2026-27F represents the proof-of-manufacturability phase. The inflection toward meaningful cost-down and margin expansion will likely occur only once platforms demonstrate stable actuator standardization, yield improvement at scale, and sustained utilization within industrial environments. We believe platforms with internal factories and balance-sheet capacity are structurally better positioned to navigate this transition from validation to scalable industrial production.