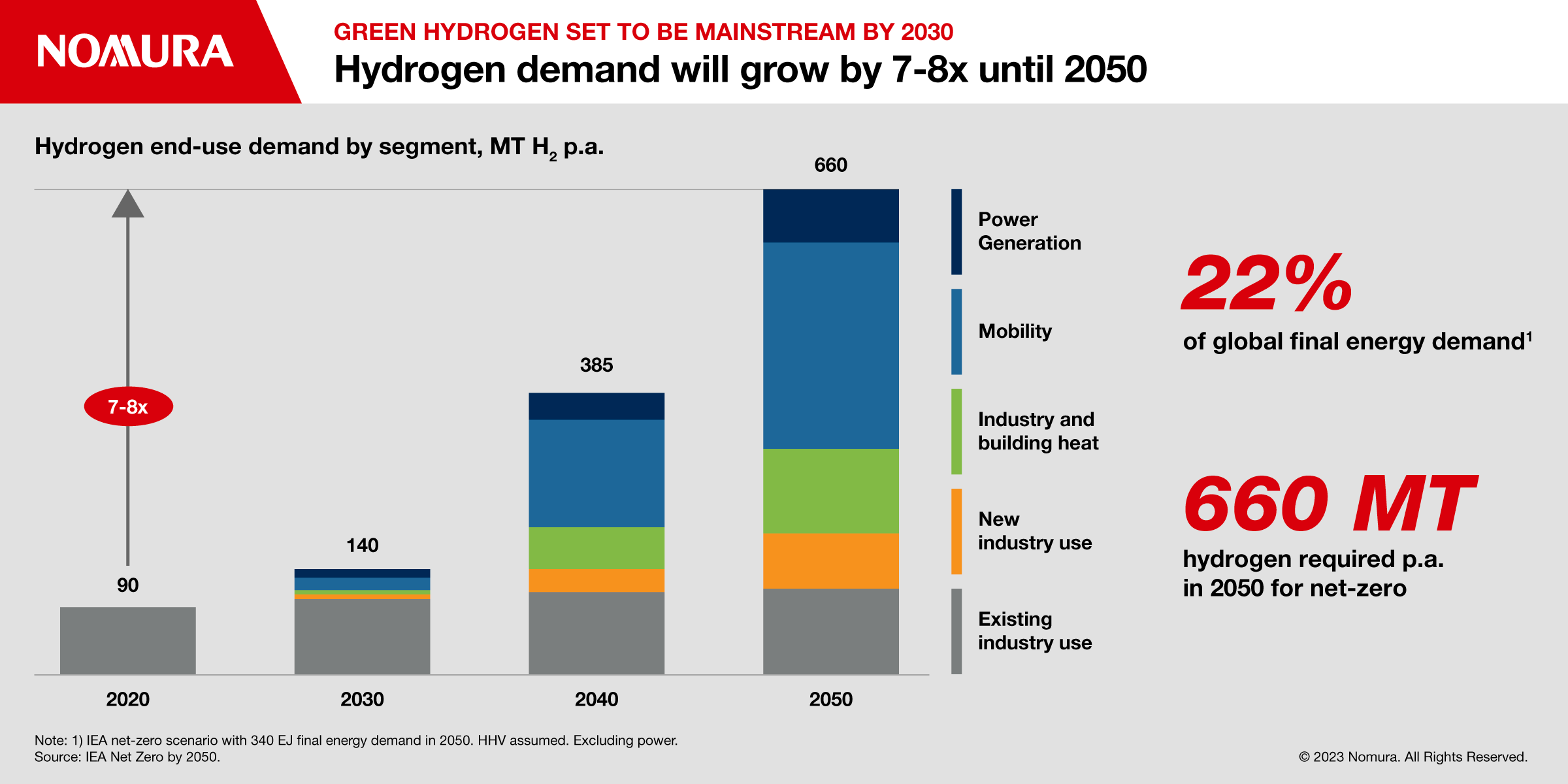

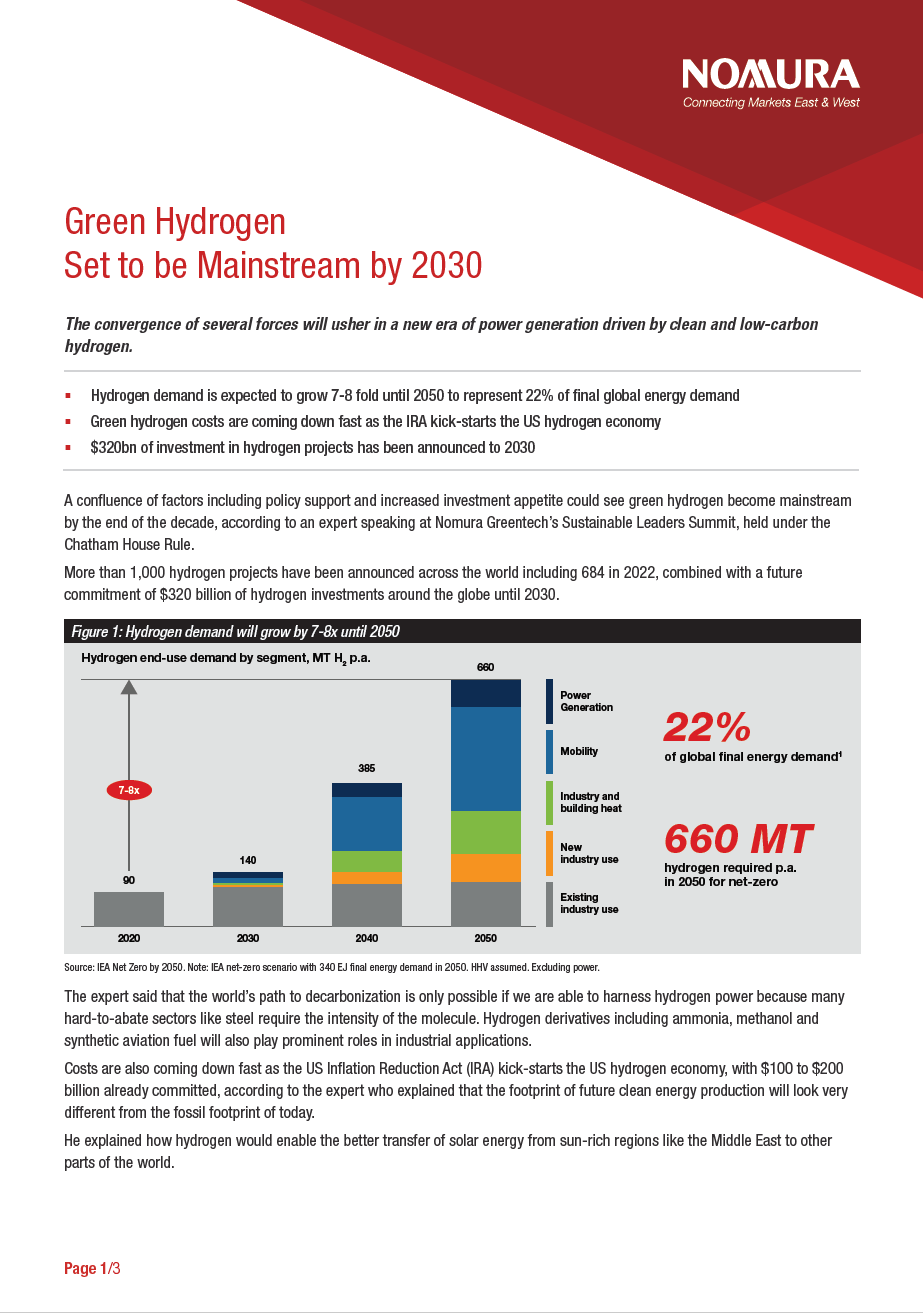

A confluence of factors including policy support and increased investment appetite could see green hydrogen become mainstream by the end of the decade, according to an expert speaking at Nomura Greentech’s Sustainable Leaders Summit, held under the Chatham House Rule.

More than 1,000 hydrogen projects have been announced across the world including 684 in 2022, combined with a future commitment of $320 billion of hydrogen investments around the globe until 2030.

The expert said that the world’s path to decarbonization is only possible if we are able to harness hydrogen power because many hard-to-abate sectors like steel require the intensity of the molecule. Hydrogen derivatives including ammonia, methanol and synthetic aviation fuel will also play prominent roles in industrial applications.

Costs are also coming down fast as the US Inflation Reduction Act (IRA) kick-starts the US hydrogen economy, with $100 to $200 billion already committed, according to the expert who explained that the footprint of future clean energy production will look very different from the fossil footprint of today.

He explained how hydrogen would enable the better transfer of solar energy from sun-rich regions like the Middle East to other parts of the world.

“We cannot export Saudi Arabian sunshine to Europe via electrons but hydrogen provides the answer. We can use the molecule as a proxy energy carrier to be able to tap into these new renewable resources that otherwise would be stranded.”

He said that it was better to incur a third of energy losses via the conversion into molecules than not being able to tap into the resource at all.

The expert explained that while the cost of hydrogen spiked 30% last year to between $4 and $6 dollars per kilogram of production driven by higher natural gas prices, costlier renewable inputs and higher raw material costs like steel and iridium, in future the cost is likely to fall dramatically.

He forecast being able to produce green hydrogen – using renewables as the electrolyzer – at about $2-$3 by 2050. Dark blue hydrogen – from a natural gas base plus carbon capture – could be produced at about $2.

The IRA industrial policy is bringing down the cost curve for electrolysis and all of the other infrastructure related components in the US, which will eventually benefit the global hydrogen market. The IRA incentives offset current prices by up to $3 for clean hydrogen. Blue hydrogen also benefits from some of the incentives using a mixture of renewables and natural gas in the process.

The bipartisan IRA bill means that a change in government won’t change the outcome, the expert said. If a new administration decided to ‘sunset’ the IRA it would only happen in 2032 by which time even if we then flip back to a pre-IRA world, we are in the corridor where it has been sufficiently scaled to be viable.

“It is like an accelerator. It brings us faster to the point where we can more or less match demand and supply.”

He said that while some countries might be more dogmatic when it comes to green versus blue or nuclear as a society globally we should be pragmatic and embrace these different pathways.

He said that the dominant hydrogen companies of the future will be determined by early movers who will form the ecosystem and use a lot of existing gas pipelines that are retrofitted to move hydrogen around instead of transporting it by vessels, which is costlier.

Japan, Korea and Europe will be among the big importers. In Europe, the Netherlands has stranded pipeline assets that used to transport natural gas from the North Sea, which could be repurposed as well as the Nord Stream 2 pipelines.

To be sure, a series of headwinds will pose challenges for the industry in the short to medium term. The biggest obstacle in getting the project bankable is the offtake, which has only led to a small number of long term agreements so far.

The expert explained that hydrogen infrastructure has more project risk as the industry is so nascent. Of the $320 billion of investments, only 10% are at the final investment decision (FID) stage. He said that it is more complex to progress a hydrogen infrastructure project to FID in the boardroom as there are more players along the value chain: renewable developers, hydrogen developers, an electrolyzer company, several off-takers, ammonia and steel refining players.

But he said that as these companies need to move in sync the time they reach the ‘FEED’ or design phase they are already committed, making it more difficult to pull out.

The expert said that he believes hydrogen combustion will also be used in mobility driven by energy dependence concerns in the electric value chain as China has cornered 96% of lithium refining capacity.

The US Environmental Protection Agency recently reclassified hydrogen combustion for zero emission vehicles even though a small amount of lubricant is burned in the process. Europe has increased the 1-gram threshold to be considered zero emission to 5 grams, which also paves the way for hydrogen combustion in vehicles.