India's M&A market is demonstrating resilience and depth, with deal activity maintaining steady momentum despite tariff uncertainties. It has evolved significantly over the past decade, with new players entering the market and sector dynamics shifting in response to changing economic conditions.

Deal volume for the first eight months of 2025 was about $70 billion, marginally higher than the same period a year ago. The absence of explosive expansion can partly be explained by the strong activity in India’s equity capital markets where transactions that traditionally might have been privately funded are now pivoting to public markets. However, the stability of the M&A market is noteworthy given global economic headwinds and tariff-related uncertainties. India's M&A market reflects a maturing of the country's corporate landscape with increasing depth, sophistication, and diversity of participants.

The composition of M&A participants has undergone a significant transformation. The early part of the last decade was dominated by large buyout funds, but since the pandemic we have also seen the emergence of Indian conglomerates as selective acquirers seeking domestic consolidation within their industry verticals. Furthermore, over the last few years, mid-cap companies with market capitalizations of $5-10 billion that were virtually absent in this type of consolidation, have also entered the M&A arena.

The shift is exemplified by transactions such as JSW Paints’ acquisition of Akzo Nobel, Dabur’s acquisition of spices and seasoning brand Badshah, and Hinduja Group’s acquisition of Reliance Capital and Invesco Mutual Fund. Indian assets that previously might have gone to buyout funds are now also being sought by domestic corporates. This trend represents a maturing Indian corporate landscape, with domestic companies increasingly viewing M&A as a strategic growth tool.

As global uncertainties persist, M&A appears well-positioned to maintain its steady trajectory in India, supported by strong domestic fundamentals and an increasingly sophisticated corporate sector ready to pursue strategic growth through acquisitions, alongside strong interest from buyout funds.

The key to success in this environment will be the ability to identify and execute transactions that create genuine scale and strategic value, whether through domestic consolidation or carefully selected international expansion opportunities.

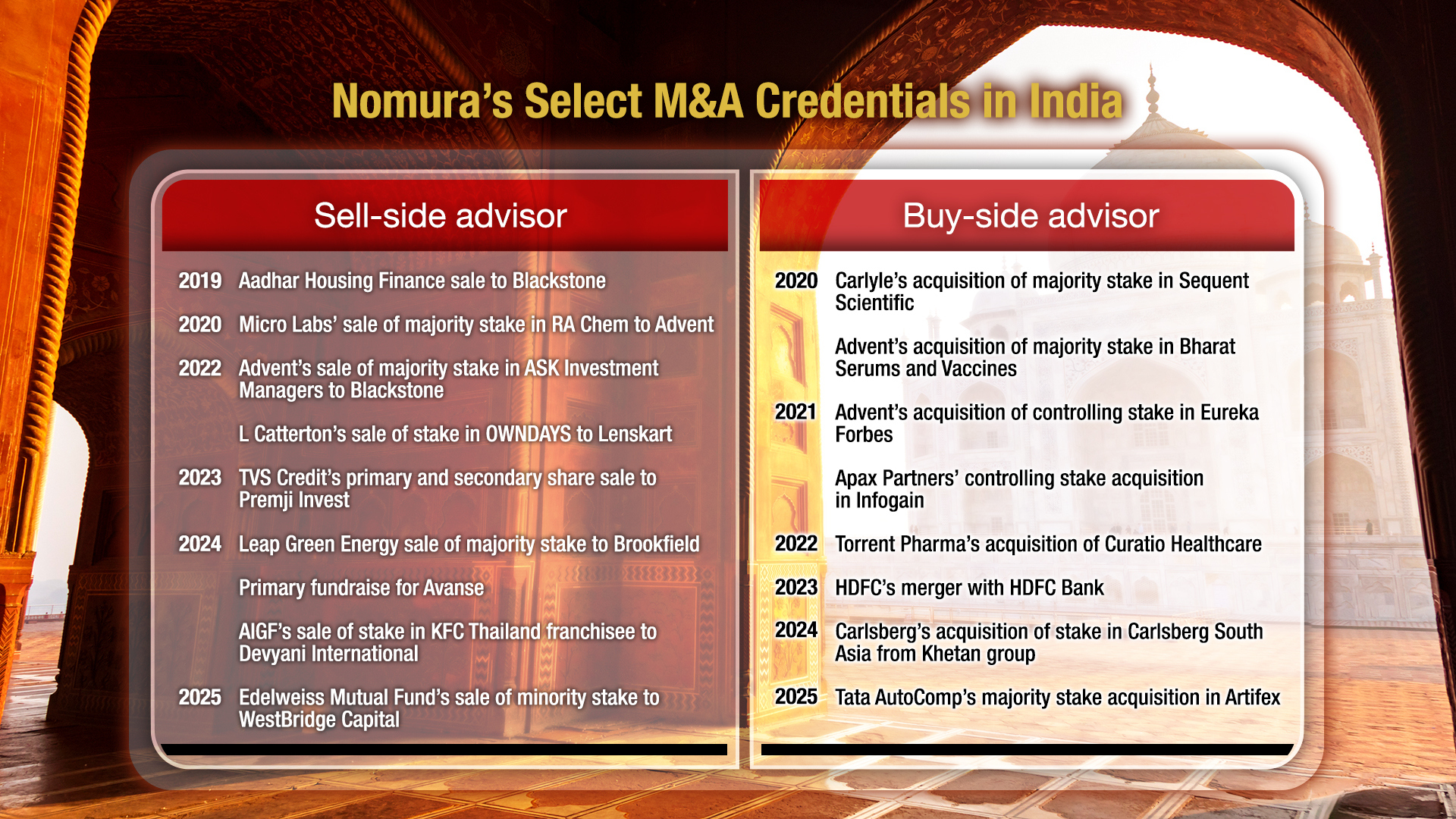

Nomura continues to be an active participant in Indian M&A by providing holistic strategic advisory services and innovative solutions to our global and Indian clients. We have advised on 33 M&A transactions including 20 sell-side mandates since 2020, demonstrating strong execution expertise across all sectors.

Financial Services: The Cornerstone

The financial services sector remains a cornerstone of India’s M&A activity, with momentum across both lending and non‑lending businesses. Recent transactions in the lending segment include Sumitomo Mitsui’s strategic acquisition of a stake in Yes Bank and Bain Capital’s investment in Manappuram Finance, reflecting sustained interest in banks and non-banking financial companies. On the non‑lending side, notable deals include Bajaj Group’s consolidation of its general and life insurance joint ventures by buying out Allianz’s stakes.

Younger lending platforms such as Vistaar, Avanse and SK Finance have also raised private capital ahead of their prospective IPOs, and asset and wealth management transactions have been picking up. Together, these deals underscore broad-based growth and continued investor appetite across diversified financial services.

Periodically, special situations and large transactions emerge, including entries and expansions by international strategic players. These episodic deals add scale and visibility, often setting valuation benchmarks for the broader market.

Healthcare and Pharmaceuticals: Awakening Giants

The healthcare sector presents a tale of two markets. On the one hand, Indian pharmaceutical companies are showing early signs of renewed M&A interest after a relatively quiet period. Torrent Pharma’s acquisition of JB Chemicals and Mankind Pharma’s acquisition of Bharat Serums and Vaccines exemplify this shift, with cash‑rich pharma companies leveraging robust market capitalizations and increasingly using stock as acquisition currency.

On the other, healthcare services continue to attract substantial private equity investment as the market becomes more organized. Key deals include KKR’s acquisition of HCG and General Atlantic and Kedaara Capital’s investment in ASG Eye Hospitals. There is also a clear wave of consolidation with sponsor‑backed platforms like Manipal Hospitals and Quality Care pursuing inorganic expansion, while listed hospital chains pursue both organic expansion and targeted acquisitions. Together, these dynamics signal a broadening of deal activity across the healthcare value chain.

Consumer: Multinationals and Renewed PE Interest

In the current landscape, we observe multinational corporations strategically divesting a portion or complete stakes in their Indian operations as part of global portfolio optimization and business restructuring initiatives. Domestic conglomerates are actively pursuing inorganic growth opportunities with a specific focus on complementary businesses that offer synergistic value. Recent examples include Tilaknagar’s acquisition of the Imperial Blue whisky brand from Pernod Ricard and Reliance Industries’ acquisition of the Kelvinator consumer durables brand from Sweden’s Electrolux.

Furthermore, with the Indian consumption story taking centerstage over the last few years amid a burgeoning middle class, we see renewed interest from the financial sponsor universe highlighted by Temasek’s acquisition of a minority stake in confectionary company Haldiram’s, ChrysCapital’s acquisition of a majority stake in premium bakery chain Theobroma and Multiples Private Equity’s stake acquisition in luggage maker VIP Industries.

Technology: Navigating Global Headwinds

The technology sector faces a more complex environment. Enterprise tech, historically a significant component of M&A activity, has been experiencing headwinds related to global uncertainties. It is expected to return to its traditional pattern of sponsor-driven activity once conditions stabilize.

New‑age tech companies are maturing, with market-tested business models and improving profitability. Many will look to access public markets, while others may opt for private capital to fund growth. Digital engineering and services platforms have attracted substantial private funding, exemplified by Multiples Alternate Asset Management's recent acquisition of a controlling stake in QBurst Technologies.

Industrials and Infrastructure: Scale and Consolidation

The Indian manufacturing sector has also attracted significant interest in recent times from both domestic strategic buyers and financial sponsors. Auto and auto components have witnessed increased levels of M&A activity including the strategic acquisition by Tata Motors of Iveco, and multiple acquisitions by the Motherson Group and Tata AutoComp in the auto components space. Its strong prospects are also reflected in multiple financial sponsors building positions and platforms in the sector.

The infrastructure sector, particularly renewables, has attracted interest from domestic strategic buyers and infrastructure funds as they actively seek inorganic portfolio expansion. Examples include acquisitions of Ayana Renewable by NTPC Green, and O2 Power by JSW Energy, leading to consolidation in the sector. Looking ahead, the key would be to manage bid-ask expectations as platforms actively evaluate public listings as an alternate avenue for funding growth plans and unlocking value.