With clear signs that the US economy has slowed, growing trade tensions rising, and new signs that global growth is slowing, is a US recession around the corner?

Clear evidence indicating that the US economy has slowed, along with declines in short and long term interest rates, highlight the potential for a recession.

An inverted yield curve has often been and adverse signal for other financial asset prices and it has often preceded previous recessions.

Financial shocks have led to recessions in the past, and the recent rise of non-financial corporate debt could prove to be a catalyst.

Where is the US at now?

“Recession” is being searched on Google as many times now as it was in the days just after the start of the Global Financial Crisis in 2008.

It’s easy to see where concerns are coming from. Trump’s trade dispute with China has been escalating for more than a year. The initial round of tit-for-tat tariff increases started in July 2018. The political landscape in Europe, particularly in the UK – the world’s fifth-largest economy – is causing unease, while Germany seems to be bracing for a technical recession. Asian markets have also seen some sharp sell-offs in recent weeks, with investors spooked both by the ongoing China-US trade dispute and civil unrest in Hong Kong. Times certainly look uncertain.

Aside from these headwinds, there is one major indicator which keeps flashing red, apparently telling us the US is set to tumble into a recession – the inversion of the US yield curve. To oversimplify, this is when yields for long-term bonds fall below short-term interest rates. The “inversion” is important because it indicates investors are pessimistic about the medium-term outlook for the economy – i.e. they fear a recession.

Thousands of column inches have already been spent on this topic. Should we be worried?

Our US Economic Team’s Monthly Momentum Indicator, shown in figure 1, suggests that over the last year GDP growth has slowed back to trend. Although slowdowns are not unusual, it can mean economies are more vulnerable to negative shocks – and, as mentioned, there are plenty of potential shocks bubbling under the surface.

Figure 1 - Nomura's Monthly Momentum Indicator

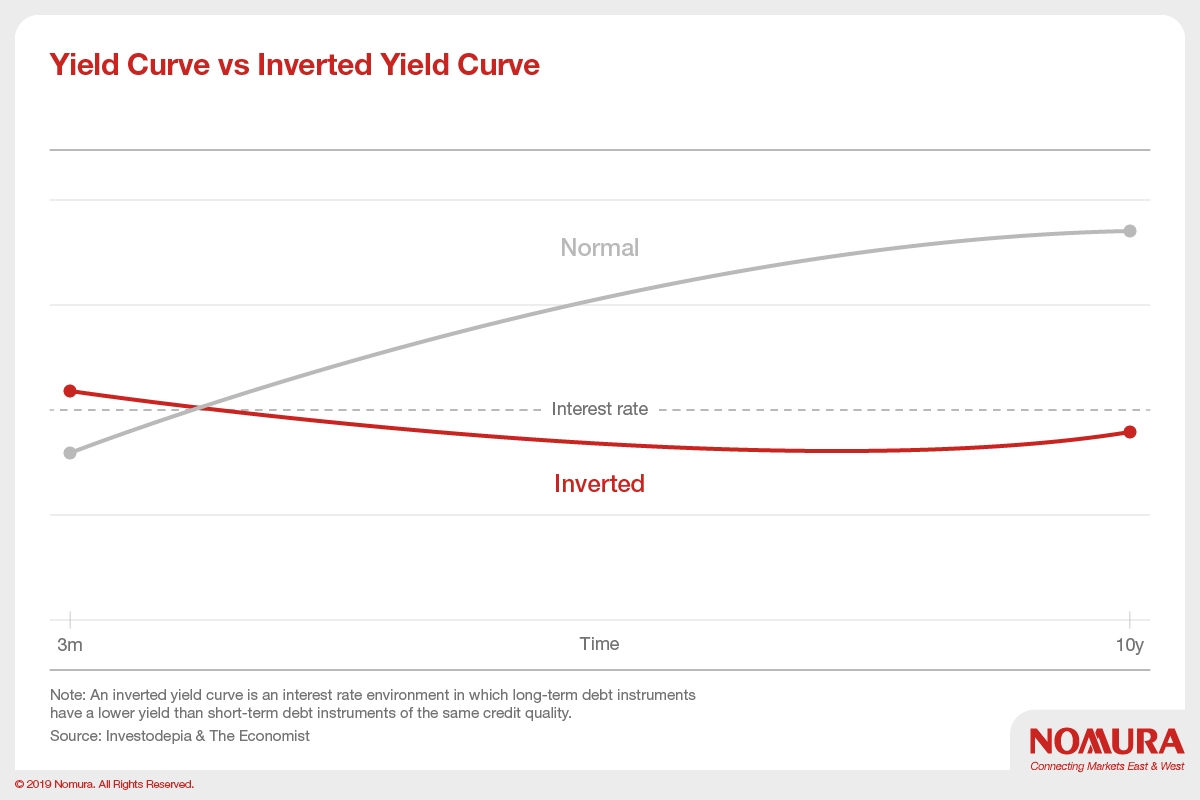

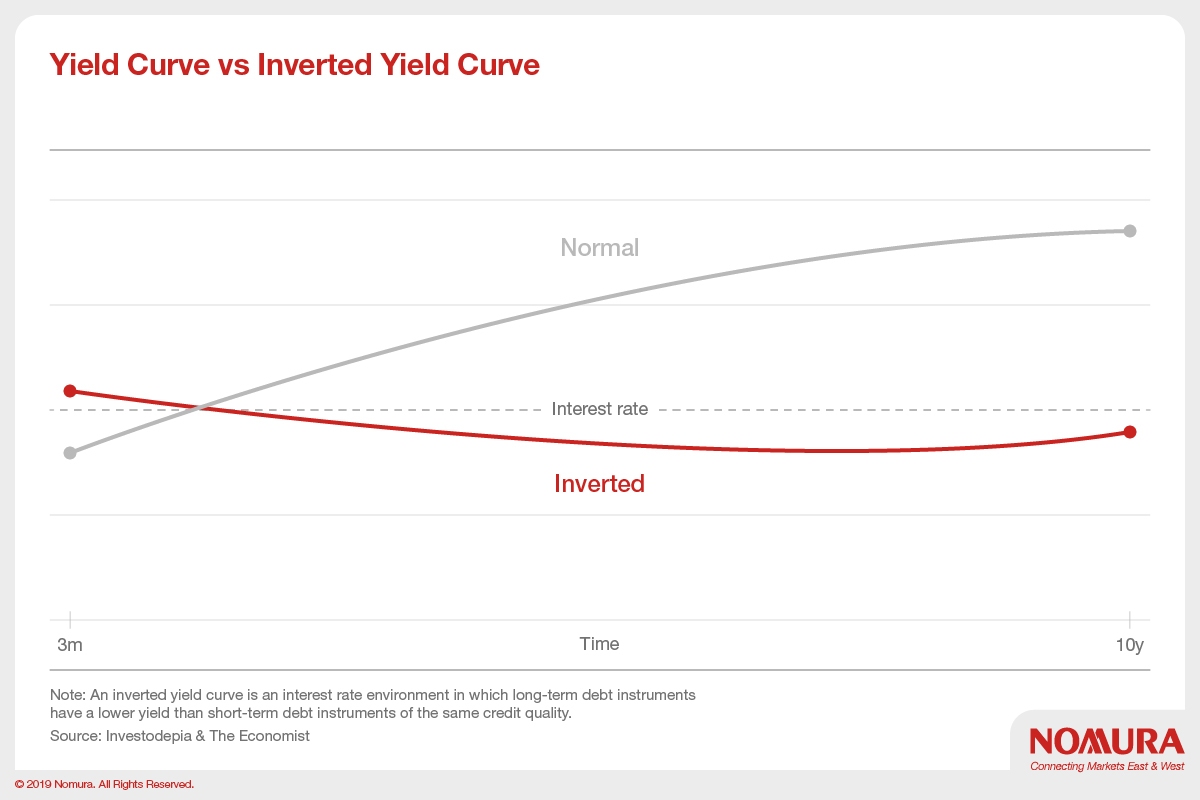

The Yield curve: The chart that predicts recessions?

In March 2019 the yield curve inverted, but why should this matter? It matters because when the yield curve inverts, recessions almost always follow.

The graph in figure 2 below shows both the normal and inverted yield curve. Although the inversion was short-lived and returned to a flatter normal curve in July.

Figure 2 - The Yield Curve, normal and inverted

However, the relationship between the yield curve and the economy is not simple or straightforward. First, the gap between the first inversion and the onset of a subsequent recession varies substantially. This gap has varied from around one-and-a-half years after the January 2006 initial inversion, to five months after the February 2000 inversion.

Second, variety of factors drive long-term interest rates and they do not all have the same implications for the economy. In recent years long term rates have been low more because in a world of reduced growth and modest inflation long-term bonds are attractive assets, not because there is compelling evidence that a recession is imminent. Despite speculation of an imminent US recession being on the horizon, Nomura’s Chief US Economist, Lewis Alexander, currently believes there is only a one-in-three chance of it happening within the next 12 months.

Now while we are predicting a 33% chance of a recession at the moment, it is important to keep in mind that there are many potential external shocks to the US economy that could rapidly increase the slowdown of the US economy and tip it into a recession.

Shocks that could tip the US into a recession

The Verdict…

The Fed has some room to act if one of the aforementioned shocks pushes the US towards a recession. Having raised rates by 175bp between late 2015 and the end of last year, the Fed is in a stronger position than central banks in many developed markets. The Fed still has some room to lower short-term interest rates to stimulate the economy.

There are, of course, fiscal policy options too, such as increasing government spending or lowering corporation or personal tax, however it is unlikely Congress and the US President would be able to act quickly enough to prevent a recession.

“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.”

It’s often said that if America sneezes, the world catches a cold. Whether or not these are the first snivels of a feverish flu or the tickle of a gentle cough is hard to say for certain. Our current view is that there are some meaningful events which need to play out before we reach for the medicine.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.