Japan in focus | 3 min read October 2025

Japan in focus | 3 min read | October 2025

Japan and Sanaenomics

Prime Minister Sanae Takaichi and her new administration launch Sanaenomics

Japan in focus | 3 min read | October 2025

Prime Minister Sanae Takaichi and her new administration launch Sanaenomics

Sanae Takaichi became Japan’s prime minister at an extraordinary session of the Diet on October 21, following the establishment of a coalition with the Japan Innovation Party (JIP). She has now started to implement her economic policies, referred to as Sanaenomics, which can be summarized in three points:

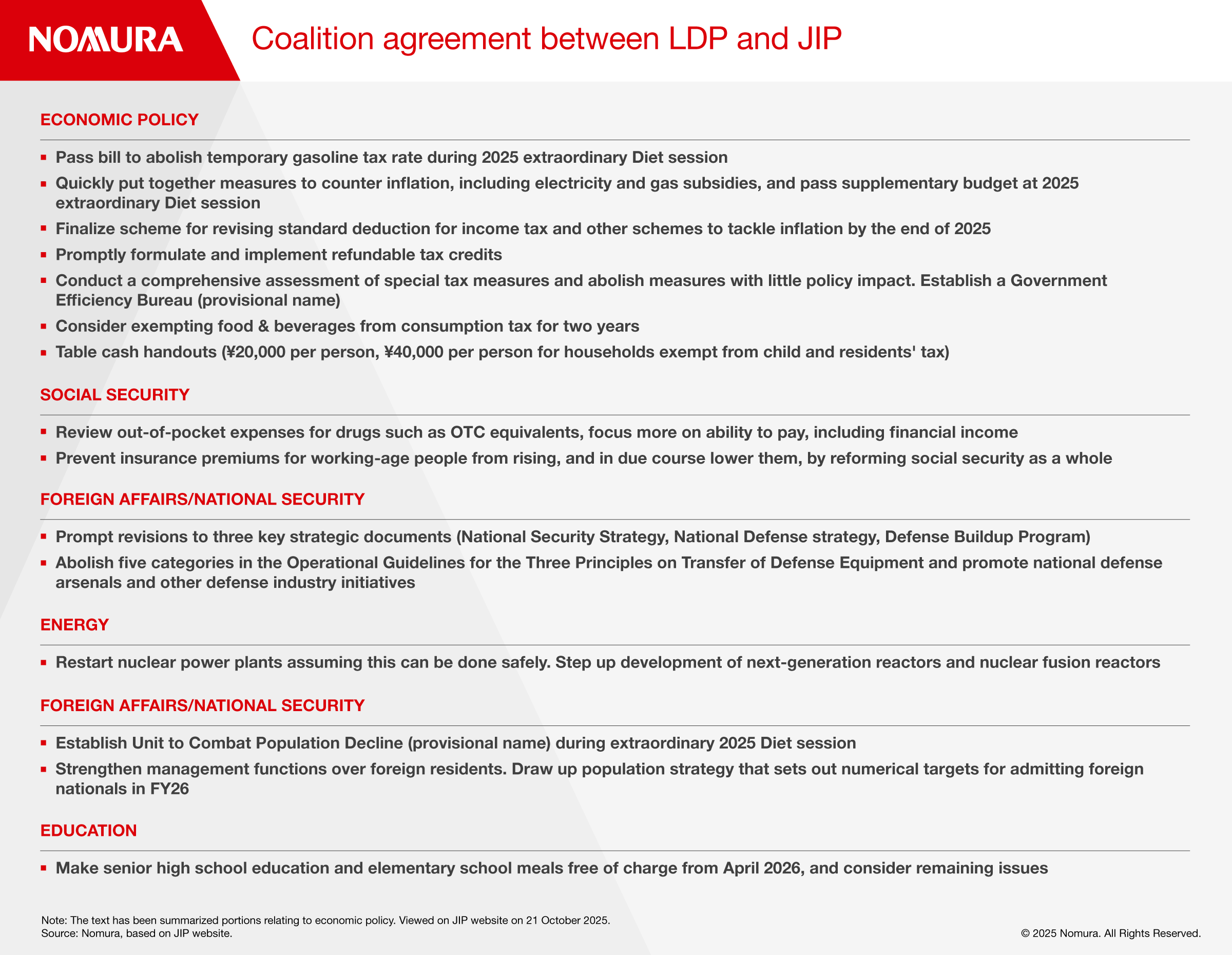

Judging by the ruling coalition agreement between Takaichi’s Liberal Democratic Party (LDP) and the JIP (see table below), it looks as though neither fiscal nor monetary policy will be as expansionary as the markets had been concerned about initially, and they will be disciplined to some extent.

However, Takaichi’s emphasis on crisis management and growth was evident from her address to the Diet following her nomination as prime minister. It included the following policies:

These measures are in line with Takaichi’s longstanding calls to strengthen national security and her LDP leadership election campaign pledge to introduce refundable tax credits.

According to the Ministry of Defense, defense-related spending in FY25 is currently set at 1.8% of nominal GDP in FY22, when the National Security Strategy was drawn up. If defense-related spending increases to 2% of GDP in the FY25 supplementary budget, this may boost GDP by around 0.2% via increased public investment and other factors.

The Japanese government has targeted reducing greenhouse gas emissions to net zero by 2050 and has planned to increase the weighting of renewables in the energy mix to achieve this. At the same time, the newly appointed Minister of the Environment Hirotaka Ishihara said at his inaugural press conference that the government needed to prevent the spread of “bad” solar power that would lead to landslides and the destruction of nature.

During the LDP leadership election, Takaichi said that she was vehemently opposed to covering Japan's beautiful countryside with imported solar panels, an indication that the current administration may take a harsh stance on renewable energy.

In contrast, she has talked about the use of perovskite solar cells, which were developed in Japan and are thin and flexible enough to be installed in a wide range of locations, so it may be that she is opposed to imported solar panels rather than the use of solar energy. In view of these comments, we think the government may come up with measures to increase the weighting of domestic procurement of solar panels and other renewable energy facilities.

It is also worth noting that her statements to date suggest that the government’s focus could shift from renewable energy to nuclear power.

We raised our share price forecasts on 7 October, after Sanae Takaichi won the LDP leadership election, and now see the TOPIX at 3,300 at the end of 2025 (3,600 in our upside scenario) and the Nikkei 225 at 49,000 (52,000). While we expect share prices to become more settled after a somewhat overblown rally, we think they are likely to remain high on the back of policy and earnings expectations.

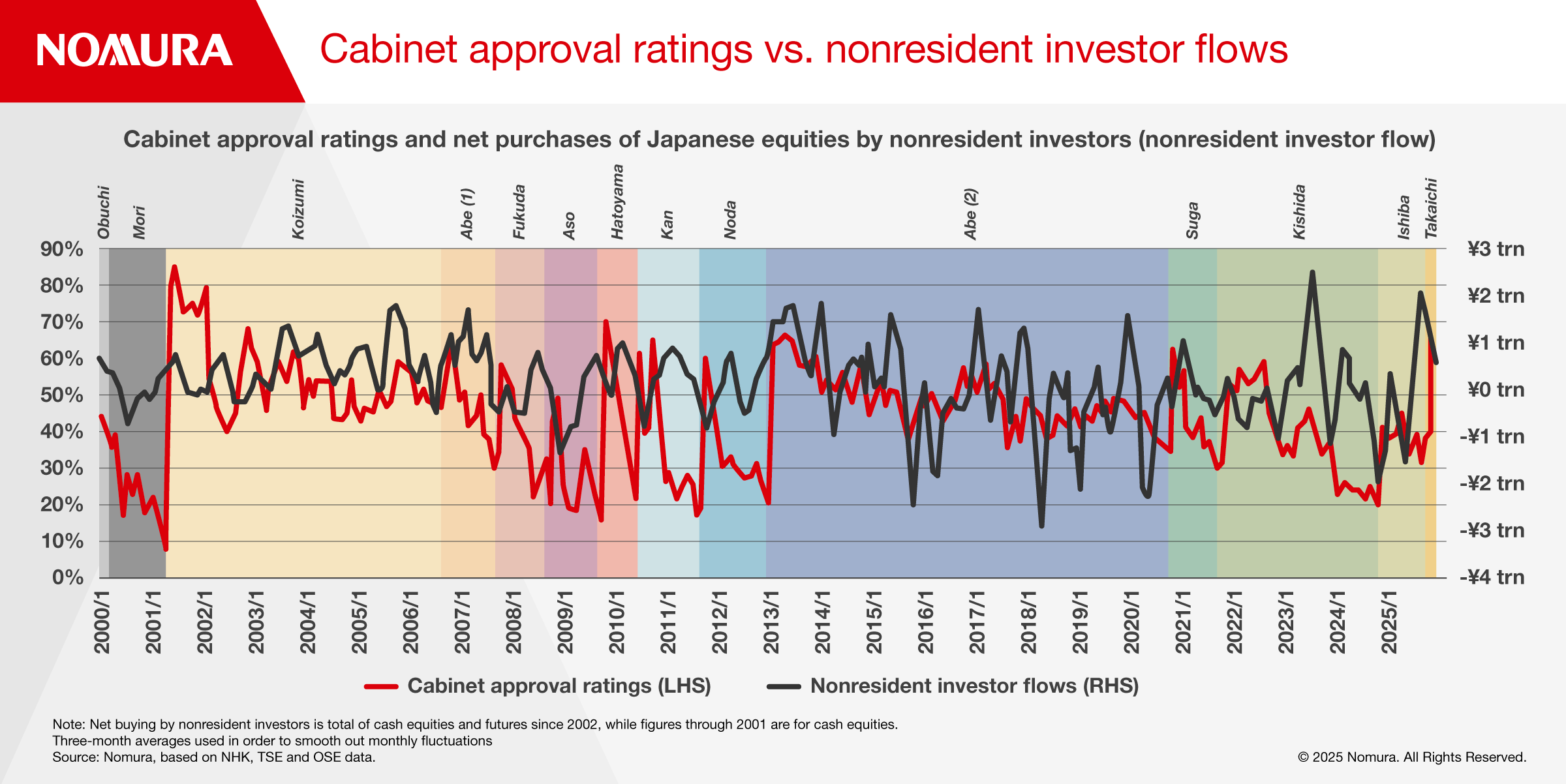

We will be watching whether the Takaichi Cabinet can keep its approval ratings high, as we see this as the key to the achievability of Sanaenomics. High Cabinet approval ratings have tended to spur net buying of Japanese equities by nonresident investors (Figure 1) though the correlation has fallen slightly in recent years. The TOPIX also tends to perform solidly when Cabinet approval ratings are high.

The appointment of Ryosei Akazawa as Minister of Economy, Trade and Industry can be read as a message that the administration plans to hold to Japan’s trade agreement with the US — which includes a commitment to purchase US aircraft and defense equipment and invest $550 billion in the US in exchange for a tariff rate of 15% on most imports. Since many nonresident investors invest in Japanese equities without hedging, they are less likely to welcome a rise in share prices caused by a weaker yen, and their attention is therefore focusing on forex policy. USD-based returns for the TOPIX in October (+2.5%) were only slightly higher than for the MSCI ACWI (+2.4%), as of October 27, and since the start of the year, they have been lower than returns for European and emerging market equities.

The LDP and the JIP between them lack majorities in both the Lower and the Upper House, so they will have to reach agreements on policies with opposition parties and/or independents. We also expect policy discussions between the LDP, the JIP, and the opposition parties about tax reforms and the initial FY26 budget ahead of the regular Diet session of January to June 2026.

While fiscal management may have brought the LDP and JIP together under Takaichi’s leadership, it remains to be seen whether this coalition will also be able to tackle longer-term issues such as making social security more efficient.

Chief Economist, Japan

Chief Equity Strategist, Japan

Senior Economist, Japan

Economist, Japan

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Japan in focus | 3 min read October 2025

Japan in focus | 3 min read July 2025

Japan in focus | 4 min read June 2025