In our recent discussions with nonresident investors, we often conclude that it is difficult to identify downside risks for the Japanese economy.

The global inflationary phase that started in 2022 provided a good opportunity for Japan to move out of deflation, with the result that the overall CPI has exceeded 2% year on year for four straight years. Also, it is becoming common practice for spring wage negotiations to settle in the 5% to 5.9% range. And although per-capita real wages have continued to fall, real macro consumption has nevertheless risen for seven straight quarters.

Provided that the Middle East conflict settles down in the near term, we think the transformation of the Japanese economy is unlikely to be impeded.

The key issue facing the Japanese economy now is raising the potential growth rate. We have identified three challenges that stand in the way of accomplishing this.

Challenge 1: The silver democracy

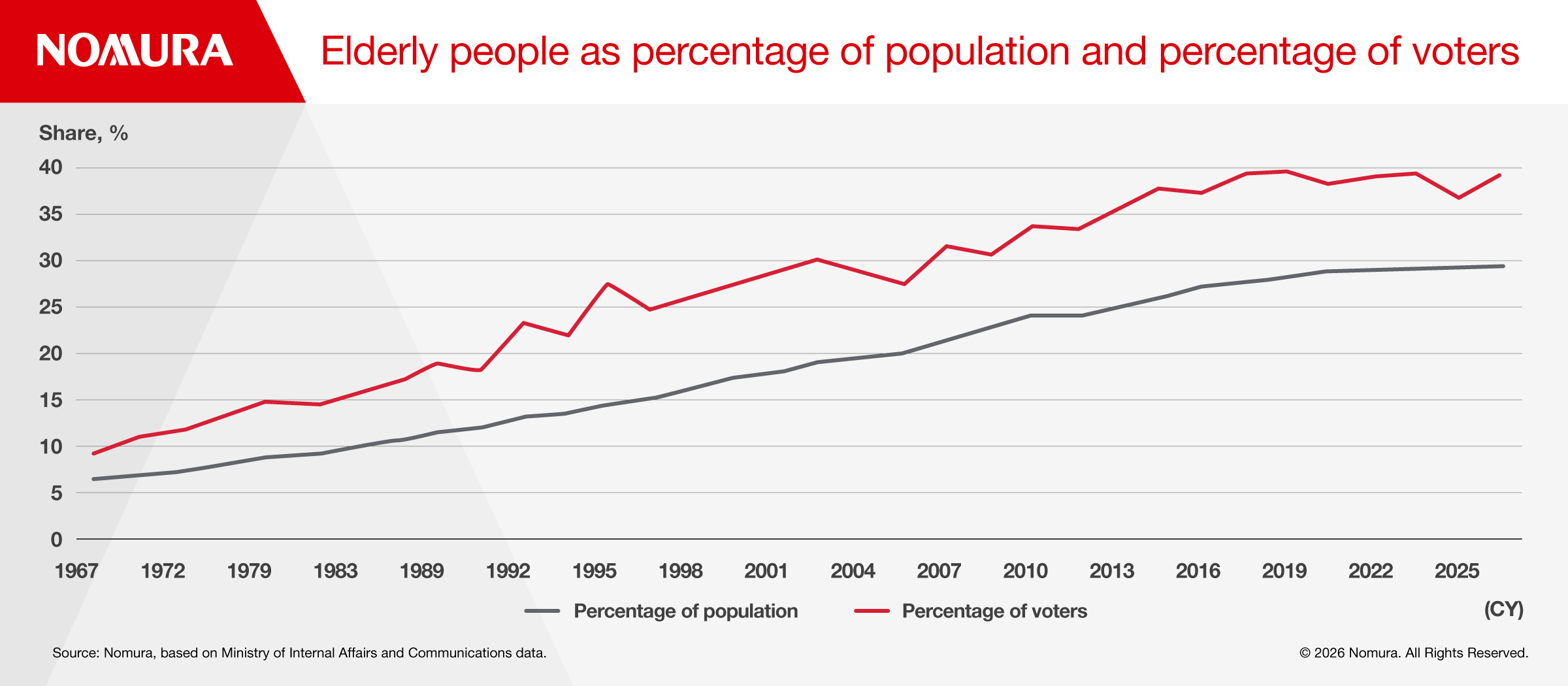

The first challenge is Japan’s silver democracy, a situation where the elderly demographic accounts for a high proportion of the voting public. This results in the adoption of policies that give preferential treatment to seniors while discouraging policies focused on future growth.

Around 30% of Japan’s population is aged 65 or older, but the group accounts for around 40% of voters in national elections (Figure 1). Japanese society is aging, and it is only natural to expect that the country’s silver democracy will be further reinforced. We have observed that investors reference the silver democracy to question the Japanese economy’s future prospects.

However, there are signs of change. The percentage of voters in their 20s and 30s started to rise gradually in the 2000s and has recently accelerated. It is unclear exactly why this cohort of voters in Japan has become more active, but it may be due to the influence of social media. In the runup to the most recent Lower House election in February 2026, there was an increase in the use of short videos to court voters. We also think social media was a factor behind the emergence of the Democratic Party for the People (DPFP) and Sanseito, as they both called for income growth for the working-age population.

Given that even a small difference in the percentage of votes won under the single-seat district system can drastically change the distribution of seats won in the Diet, we think the higher turnout of young voters is of a scale that cannot be ignored by political parties. If social media can be used to improve the voting rates of young and working-age people, then politicians are likely to step up their social media-based communications. We also expect to see an increase in the number of policies that resonate with the working-age population.

Even though social media has been a source of political instability in many countries, it could help Japan move out of its silver democracy and promote growth-oriented economic policies.

Challenge 2: Fiscal issues

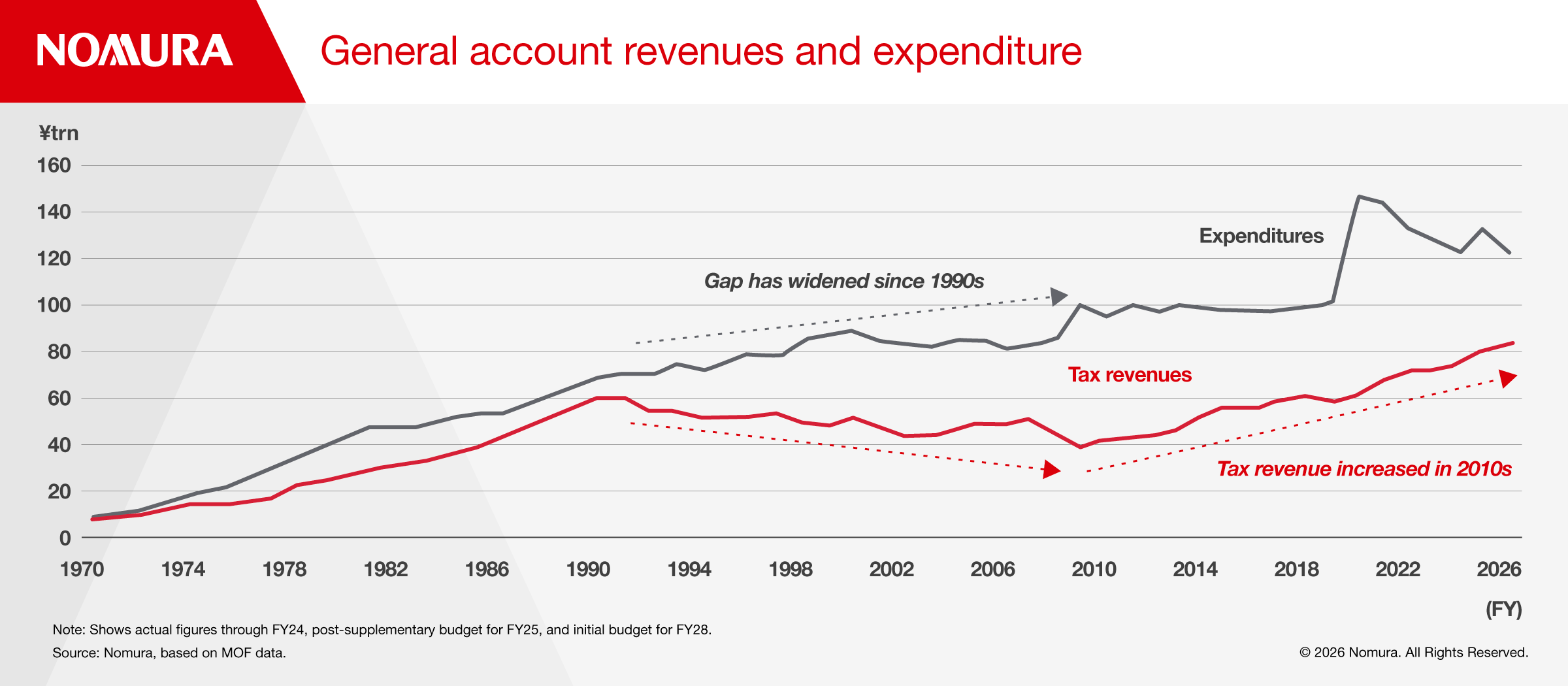

The Japanese government is facing some difficult fiscal issues, which could act as a constraint on its proactive growth initiatives. Reasons for pessimism include Japan's low birth rate and aging population, ballooning social security spending, and a government debt-to-GDP ratio exceeding 200%.

However, two changes are taking place. The first concerns recent trends in tax revenue, which is now increasing at a faster pace than government expenditure (Figure 2). Its primary balance is very close to reaching a surplus, as tax revenues have been higher than the government had estimated, especially due to growth in income tax revenue

While tax revenue from financial income has been rising in response to higher Japanese equities and dividend increases, the main driver has been growth in salaries as spring wage negotiations frequently lead to salary hikes of around 5%. This means the structure supporting the increase in tax revenue is relatively stable.

The second change concerns how the government draws up its budget, with Prime Minister Sanae Takaichi stating that the FY2027 budget drafting process would be reorganized. The first step will be to estimate the impact of growth strategies on the economic growth rate as well as the resulting increase in tax revenue and impact on fiscal policy, then the direction of the budget will be laid out in the Basic Policy. Previously, there was little relationship between growth strategies and budget formulation.

Takaichi also instructed Satsuki Katayama, the Minister of Finance, to assess the scale of possible fiscal spending while also lowering the government debt-to-GDP ratio. The longer-term economic outlook published by the government in January 2026 envisions two scenarios: long-term nominal GDP growth of around 1% year-on-year or around 3%. If the rate of economic growth were to be revised upward, we think it would be natural for the government to increase its fiscal spending.

Challenge 3: Ensuring the effectiveness of growth strategies

Whereas fiscal stimulus during recessions is a demand-side macroeconomic policy, growth strategies are a supply-side macroeconomic policy designed to impact areas such as capital inputs, labor, and technological innovation. However, even if supply capacity is increased, economic growth will not be achieved unless demand is stimulated.

The modern supply-side economics (MSSE) advocated by the Takaichi administration's economic advisors does not deny the role of government in the process of stimulating growth. Unlike neoliberalism, which is mainly based on deregulation, MSSE aims to achieve economic growth by using government functions to correct market failures. One distinct feature of MSSE is that government-led demand creation can also serve as a key policy tool.

We think the Takaichi administration’s policy of promoting investment in 61 key products and technologies in 17 strategic areas is consistent with this framework. Ahead of the drafting of its growth strategies in the summer, we expect the government to make four quantitative disclosures for each product and technology: the size of investment, the timing of investment, the knock-on effect on the economy, and the impact that it will have on stimulating related investment.

The total impact on GDP and tax revenue, as well as improvement in the debt-to-GDP ratio, will be reflected in longer-term economic estimates.

What awaits after the three challenges are overcome?

The dichotomy of demand-side and supply-side macroeconomic policies is missing an important piece: the perspective of distribution, which links supply and demand.

The government continues to support wage hikes while trying to make Japan a haven for asset management, like past administrations. But Takaichi’s government is also mulling the introduction of refundable tax credits, which we think is an efficient means of redistributing income, though it remains to be seen what kind of distribution policies Takaichi is aiming for.

To read the full report, click here.