Central Banks | 3 min read | January 2026

Japan’s Ruling Coalition Considers Eliminating Consumption Tax on Food

A consumption tax moratorium and a weak yen might encourage the BOJ to raise interest rates sooner and more often

Central Banks | 3 min read | January 2026

A consumption tax moratorium and a weak yen might encourage the BOJ to raise interest rates sooner and more often

Prime Minister Sanae Takaichi announced that she will dissolve Japan’s lower house and has called a snap election for February 8.

A key factor in gauging the economic outlook after the election is that the ruling Liberal Democratic Party (LDP) has said it is considering eliminating the 8% consumption tax rate on food for two years, as part of its coalition agreement with the Japan Innovation Party. Opposition parties have also pledged to lower or eliminate the consumption tax rate.

On the one hand, by eliminating the consumption tax on food, tax revenue would fall by about ¥5 trillion ($31.7 billion) a year. Although the Takaichi administration has been aiming for what the prime minister calls "wise spending", which combines fiscal efficiency and fiscal discipline, a move to suspend the consumption tax would run the risk of heightening fiscal concerns.

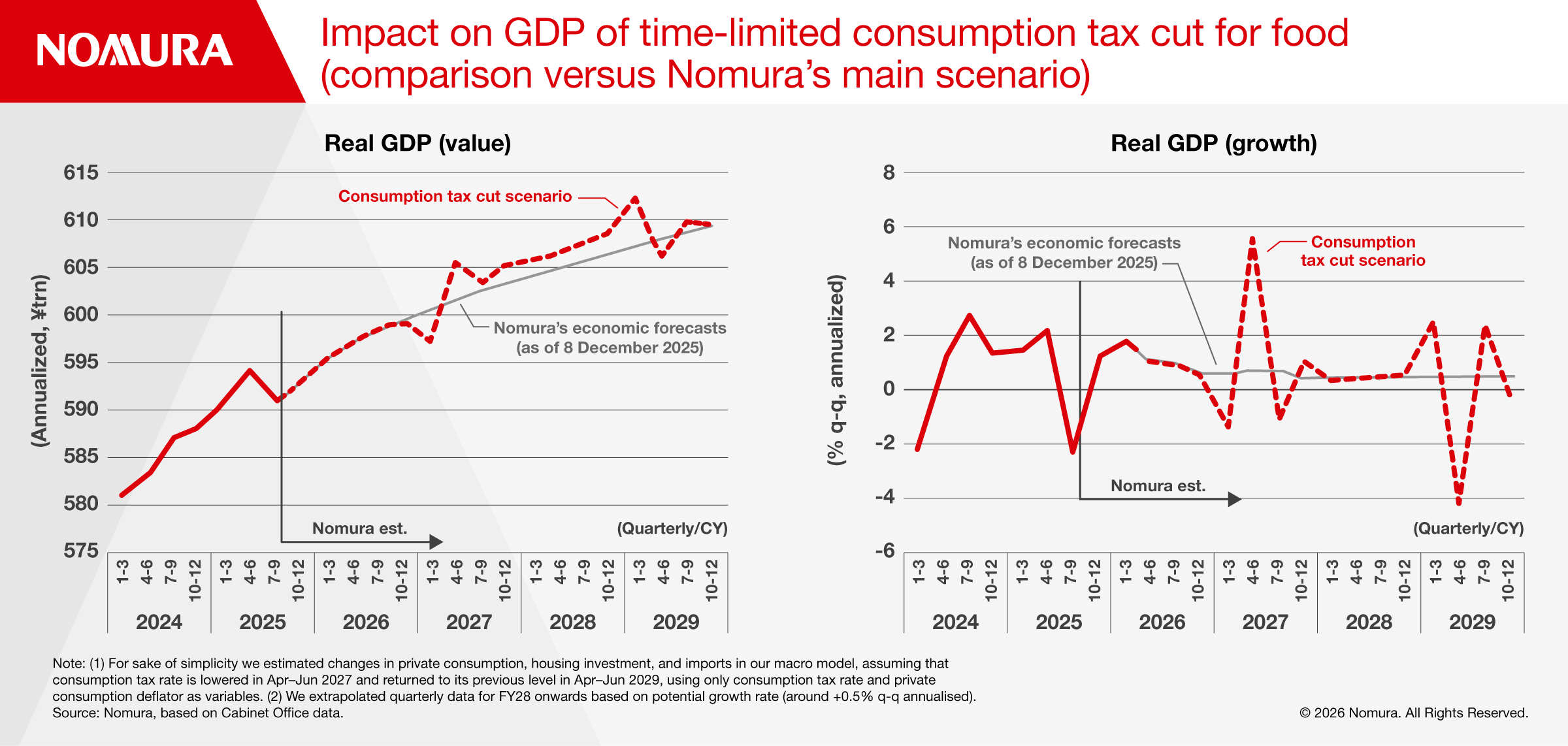

On the other hand, the policy would boost real GDP during this period. But this would not necessarily lead to an increase in potential growth (see Figure 1). Without an acceleration in potential growth, the government would have to think hard about whether tax revenues would rise enough to offset the ¥5 trillion in lost consumption tax revenue — and whether this would constitute “wise spending”.

If the consumption tax rate were to be temporarily eliminated, we think this might cause the yen to weaken regardless of US/Japan interest rate differentials.

Normally, USD/JPY acts like a kite and US–Japan interest rate differentials act like its string. BOJ monetary policy controls the string to move the kite. However, if fiscal instability were in some way to affect investor behavior, the kite might become detached from its string and move in an unpredictable way (yen depreciation).

We estimate that cutting the consumption tax rate on food to zero would lower CPI inflation by as much as 1.5%. However, a weakening yen could wipe out a considerable portion of the downward pressure on inflation.

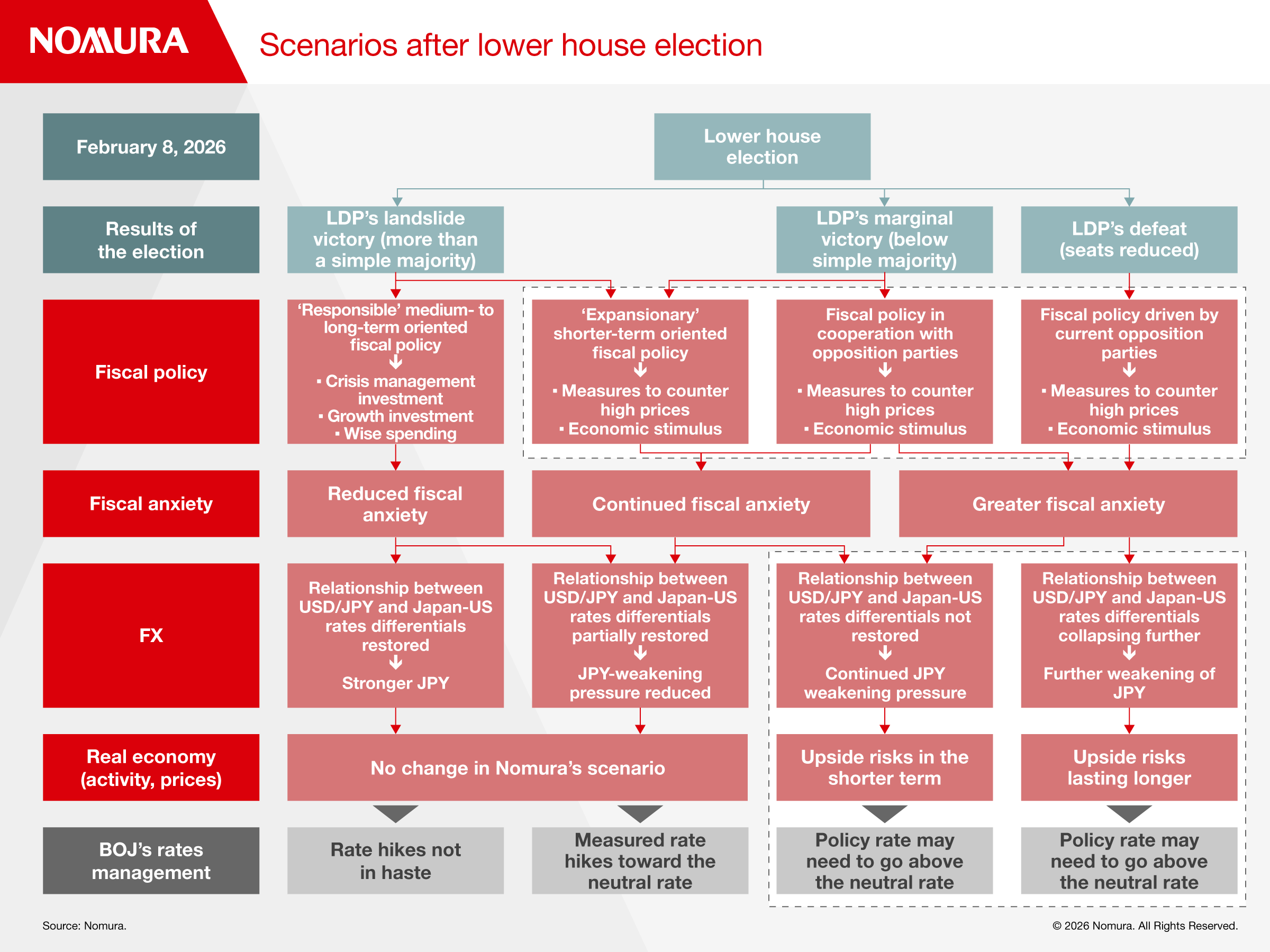

We think the main post-election scenarios will revolve around:

The current fiscal policy conduct of Takaichi’s minority government has had to take into account the stance of the LDP’s coalition partner and opposition parties — including temporary cuts to the consumption tax rate for food — as well as forex reactions. Therefore, we cannot ignore the possibility that the scenarios inside the dotted lines in Figure 2 might become reality. In these scenarios, the terminal rate (the BOJ policy rate at the end of the rate hike cycle) could exceed the neutral policy rate for the real economy, which could make monetary policy more restrictive and lead to a slowing of the economy.

Of course, with the outcome of the general election still unknown, it is not possible to favor one scenario over another.

The BOJ has said, with regard to how it conducts monetary policy, that if its outlook for economic activity and prices is realized, it will “continue to raise the policy interest rate and adjust the degree of monetary accommodation”.

This suggests that the focus of its policy rate control is on the economy and prices, and that improvements in the economy and prices are needed for a rate hike. It also suggests that the next rate hike will be aimed at adjusting monetary easing rather than tightening monetary policy and, because of this, it is highly likely that the neutral rate would be the same as the terminal rate.

However, given the risk of expansionary fiscal conduct with a short-term horizon — specifically, cuts to the consumption tax rate and a subsequent fall in the value of the yen — we should instead assume the following:

The fourth point is of particular importance.

The focus of policy rate control had been on the economy and prices, so we had forecast that there would be no rate hikes in 2026, two rate hikes in 2027, and a terminal rate of 1.25%, which is close to the bottom of the range for the neutral rate of interest.

However, considering the risk of further yen depreciation and fiscal policy conduct with a short-term focus, we now see potential for two rate hikes in 2026 if the BOJ were to change its basic monetary policy stance to one with the characteristics of points 1 to 4 above. In addition, these rate hikes would not just bring forward hikes that would have happened anyway (in which case the terminal rate would be unchanged) but would constitute additional rate hikes (in which case the terminal rate would rise).

In this scenario, we see the possibility of three or four additional rate hikes between now and the end of 2027. As a result, the terminal rate might clearly exceed the lower limit of the neutral rate of interest.

Chief Economist, Japan

Economist, Japan

Japan Economist

Japan Economist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.