Japanese equities have been negatively affected by rising crude oil prices and upward pressure on interest rates. Worsening labor shortages are also likely to trigger business portfolio restructuring.

In this environment, we think the path to success for Japanese equities will involve 100-year-old companies that are resilient to changes in the business environment, physical AI that leverages on-site data and robotics technology, and Japanese content that can attract foreign currency.

100-year-old companies

Many Japanese companies are resilient. They have survived and evolved through two world wars, oil shocks, extreme yen appreciation, and financial crises. Although these companies have sometimes been disparaged as “traditional,” their longevity offers a blueprint for success.

Since the spring of 2025, corporate Japan has faced a range of shocks, including the US tariff shock, the Anthropic shock, the Iran conflict, and sharp rises in crude oil prices. But at 100-year-old companies, earnings and share prices have been solid, except in the automotive and diversified chemicals sectors.

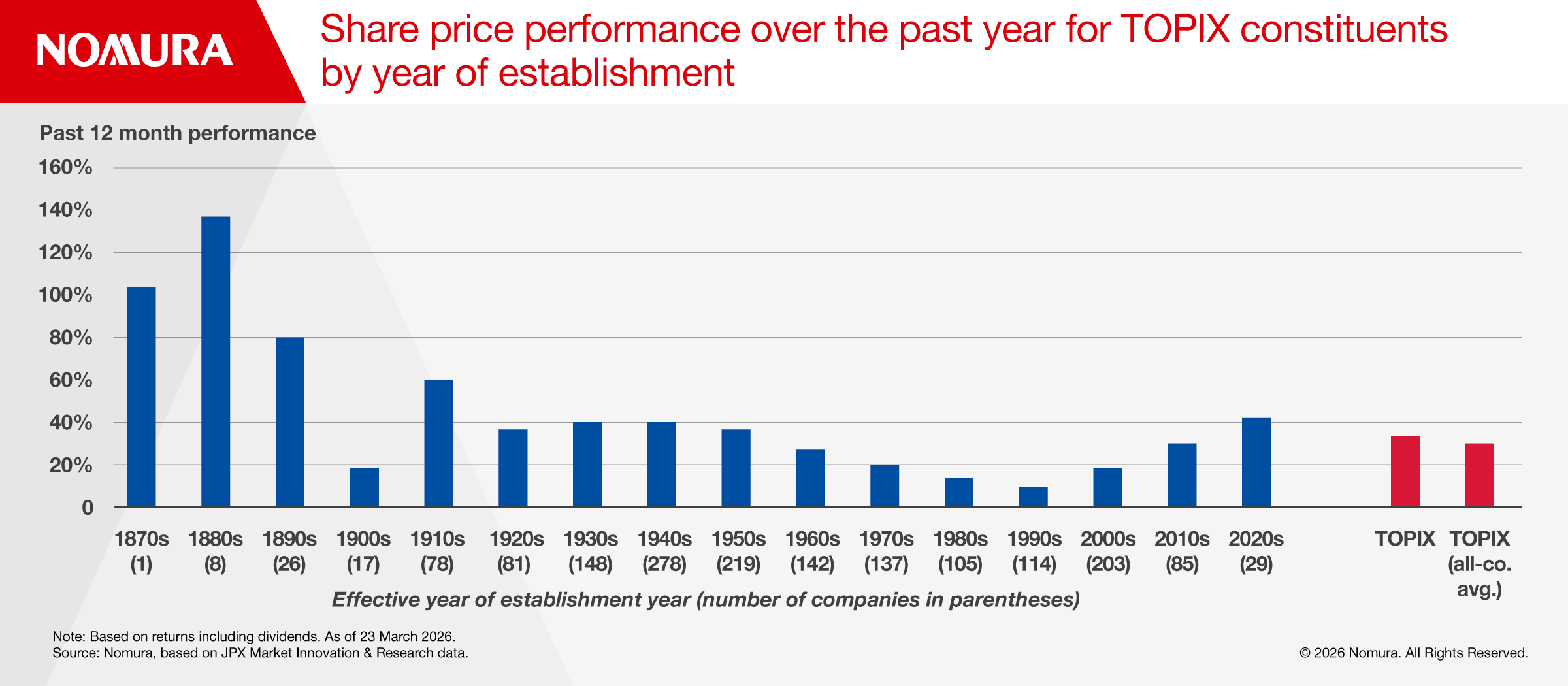

TOPIX index companies that were established prior to the Second World War have outperformed the TOPIX as a whole over the past year (Figure 1). In particular, companies established prior to the 1910s have performed solidly. While this partly reflects the large number of such companies in the construction, defense, and nonferrous metals sectors, many 100-year-old companies in the chemicals, machinery, and electrical machinery sectors have also substantially outperformed the TOPIX.

Change and evolution have been keywords for these companies. Many have gradually transformed their core operations — such as from forestry management to housing, from aircraft cooling equipment and ammunition to air conditioners, and from traditional Japanese playing cards to games and IP.

Physical AI

Physical AI is a prime example of how the use of AI technology has helped to upgrade the competitiveness of Japanese companies in the machinery domain.

We expect markets for manufacturing, logistics, and healthcare to expand from 2030, and we think Japan is likely to roll out a winning strategy by leveraging AI to incorporate the tacit knowledge contained in the factory and project site data that Japanese companies have built up over time into manufacturing equipment, automobiles, and robots.

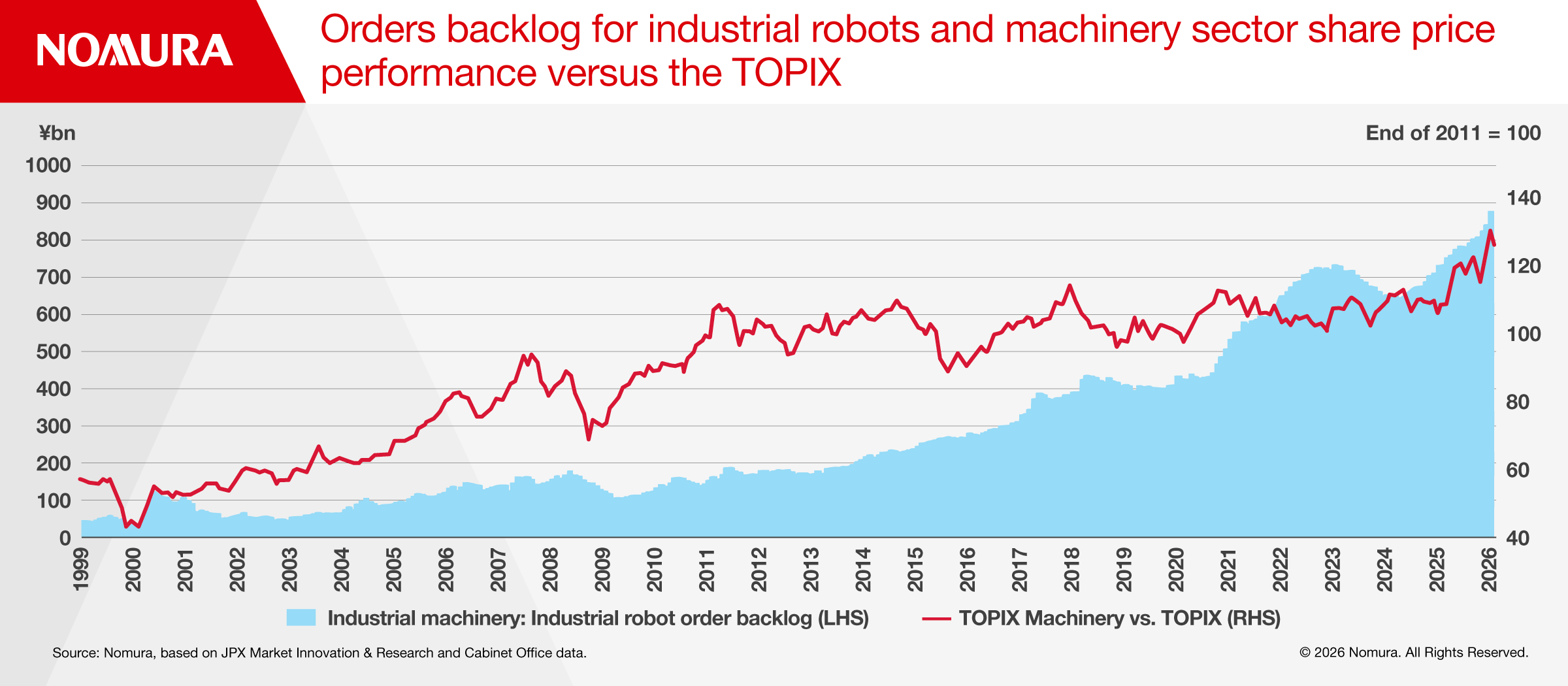

Japan’s advantages in these fields are evident in the physical AI partnerships with Japanese companies that Nvidia announced at its March 2026 GPU Technology Conference. Although China has a roughly 50% share of the global market for humanoid robots, it is often dependent on Japanese companies for parts and materials for precision manipulation and motion control products. The order backlog for industrial robots in Japan has been rising steadily and has also been correlated to the relative share price performance of the machinery sector versus the TOPIX (Figure 2).

Japan’s Ministry of Economy, Trade and Industry has stressed that a wide range of issues are being addressed by robots and automation technologies, including autonomous driving, long-term care robots, disaster response robots, self-driving agricultural and construction machinery, industrial processing robots, and food preparation robots.

The share price performance of robot-related stocks shows frequent outperformance for industrial processing robots as well as disaster response and food preparation robots, but frequent underperformance for autonomous driving. We think interest could widen if growth strategies boost expectations for growth in public–private investment.

Meanwhile, Japanese government support for the semiconductor industry, which forms part of the physical AI universe, has already reached ¥10 trillion and is likely to remain substantial in the future. Japanese SPE companies are also likely to benefit from the construction of semiconductor plants in Japan.

Content

Physical AI requires the Japanese robotics industry to combine its strengths with AI to advance its competitiveness. Similar AI synergies are also likely to emerge in the area of entertainment. The Takaichi administration's growth strategy aims to boost demand for and exports of anime and other Japanese content.

Overseas sales in the entertainment industry have quadrupled from ¥1.4 trillion in 2013 — when the Cool Japan policy got into full swing — to ¥5.8 trillion recently, while overseas sales in the creative industry have nearly doubled from ¥123.1 billion to ¥261.4 billion over the same period. The government is targeting overseas sales of content originating in Japan of ¥20 trillion by 2033 in a bid to accelerate this trend.

The Takaichi administration’s policy is to promote large-scale, long-term, strategic public–private investment and overseas expansion, including multi-year support, toward this goal. It is looking to maximize profits by offering translation and marketing support, without interfering with the content itself.

It has positioned the content industry as an overseas currency earner by transforming it from a labor-intensive industry that primarily earns domestically into a knowledge-intensive industry that earns globally, and that by 2040 will generate half of Japan’s goods and services surplus.

Since 2019, stocks related to content and services have tended to outperform in line with growth in content services exports.

While we are concerned about the potential for AI to take over the content industry, we also see plenty of scope for reassessment, as it is resilient to resource prices and supply chain risks, and it is also unlikely to be affected by tariffs.

To read our full report, click here.