The increasing convergence of different sectors within the green transition is challenging investors and founders to understand their interplay in order to back the best technologies, according to senior executives at Nomura Greentech’s Sustainable Leaders Summit in Salzburg, Austria.

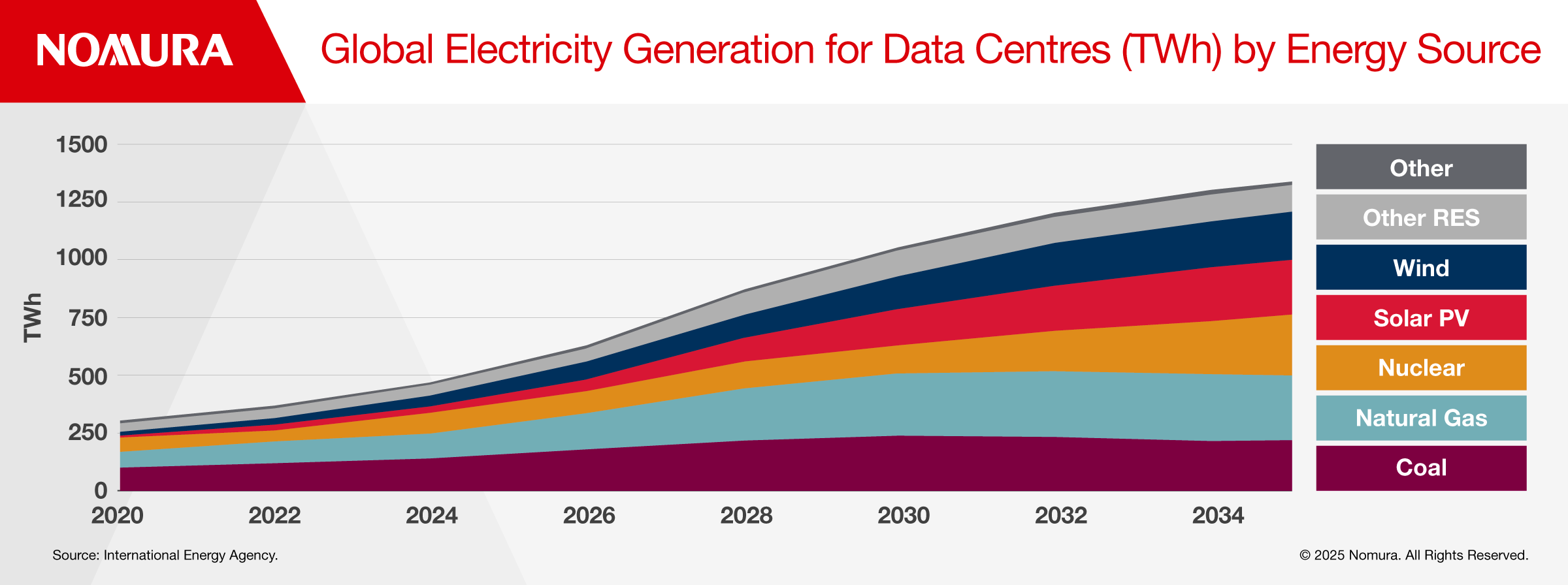

The advent of AI and machine learning is the clearest example of this convergence as the rapidly evolving technology drives massive demand for data center capacity, which in turn fuels demand for green power. The European Data Center market is set to double to $232bn by 2035, with AI driving capacity growth to 26.6GW while AI expansion in Europe is forecast to drive a 165% increase in power consumption by 2030.

As the sector transforms into a hyperscale-dominated market driven by the big US cloud providers such as Microsoft, AWS and Google, it will need to expand beyond the FLAP-D markets of Frankfurt, London, Amsterdam, Paris and Dublin for renewable energy access, underscoring how the sector is also driving geographical interconnectivity.

Executives at the summit explained how grid capacity has emerged as a critical bottleneck, with development constraints coming from the limited availability of land and power, especially in Tier I and Tier II markets. Connection delays now stretch beyond seven years in some markets such as Germany. This strain on existing electrical systems has become the primary obstacle to sector growth.

European data centers are shifting from grid dependency to a renewable energy focus, driven by surging demand and regulations like Germany’s 2027 green mandate, which will require data center operators to source 100% of electricity from renewables.

Europe leads in the clean energy transition, with renewables and nuclear set to power 85% of data centers by 2030 versus a global forecast of 60%. Data centers in the EU are now pursuing innovative solutions, including strategic grid partnerships with utilities companies, and waste heat recovery systems.

A case in point is the joint venture between Iberdrola and Echelon, a landmark transaction in Spain, which pairs Iberdrola’s expertise in land acquisition and power supply with Echelon’s responsibility for development, design and operations of data centers. Spain is evolving from a secondary market to a key Southern European hub, targeting 4-6 times capacity growth by 2030 driven by AI demand and the strategic gateway positioning of its main hubs in Madrid and Barcelona. Spain’s government is actively supporting data center growth through tax incentives, renewable energy investments, and streamlined regulations.

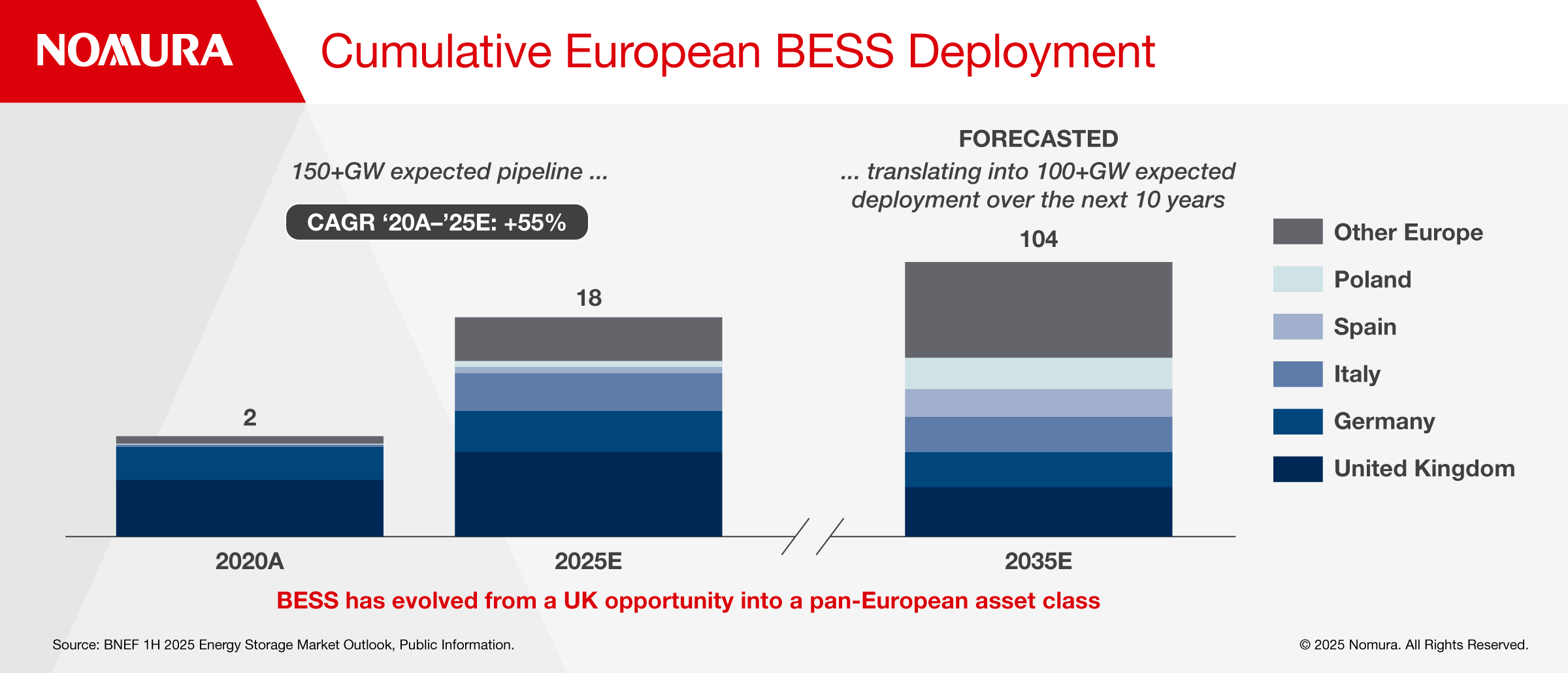

The final element in this chain is grid flexibility, using technology such as battery energy storage systems (BESS) to mitigate the volatility and intermittency challenges of using renewables in greater volumes while adding resiliency into the system.

In April this year, the Iberian Peninsula (Spain and Portugal), experienced a half-day blackout owing to a complex failure of parts of the grid. The Iberian electricity system features a high share of renewables, and a relatively slow rollout of BESS, which increases the risk of potential outages. Electricity storage systems can partially offset variability by storing excess energy during periods of abundant renewable generation and releasing it during peak demand. Additionally, transmission lines linking different electricity grids provide further flexibility by facilitating the transfer of surplus energy between them. Many countries are increasingly investing in these flexibility measures to accommodate higher shares of renewable energy.

Advancements in BESS technology such as longer duration - 4+ hours of capacity - alongside falling system costs and longer asset life are also making the technology more widely available in this ever-complex data and energy ecosystem.

Cumulative BESS capacity in Europe is projected to increase from about 18GW today to about 104GW by 2035.

LOW CARBON MOLECULES AND CIRCULARITY

It’s a similar story in the realm of low carbon molecules where innovative technologies are converting waste from one sector into usable products in unrelated industries. Take the companies involved in capturing CO2 directly at the point of emission, feeding it into a bioreactor and fermenting it with hydrogen to create emissions-free chemicals that can be reintegrated into supply chains.

THE LONG ARC OF ELECTRIFICATION – TRANSPORT & HEATING

The final major element of convergence covers the long arc of electrification, encompassing transportation and heating. As heat pumps gradually replace gas boilers and electrified homes with solar panels and battery storage become more commonplace, households and the grid will be more interlinked than ever before.

This trend will be completed by the rollout of V2G or vehicle to grid technology as electric vehicles become the dominant mode of consumer transportation and drivers connect their home vehicle charging ports to the grid whenever they have surplus power in order to lower their electricity bills. In the US, General Motors is a good example of a major auto producer that’s embracing the concept. It is introducing a suite of accessories through its GM Energy business to enable battery-electric-vehicle customers to unlock ‘vehicle-to-home bidirectional charging’, which enables the vehicle to share power with other devices or the utility grid.

The electrification market is on the cusp of massive growth with 42 million residential assets expected to be installed across Europe by 2030, adding 261 GW of capacity—equivalent to grid-scale renewables growth.

For more information on this topic, please contact Alex Wotton or Alex Stein.