Part 3 of our Nomura - University of Sheffield research on the social pillar of ESG in East Asia explores the challenges information providers face in gathering and interpreting data.

Burdensome and confusing disclosure requirements are a big issue

Global rules create contradictions for national jurisdictions

Aligning and simplifying global rules will lead to better data

This article was produced in collaboration with

ESG in East Asia: The 'S' Factor (Part 3)

ESG ratings, indices, and funds are proliferating globally, as investor concerns grow about organizations externalizing their responsibilities. However, it is this variety of outputs that makes ESG information challenging to interpret, potentially undermining the intention to express investors’ values through their portfolios.

In this our third article on ‘ESG in East Asia – The S Factor’, we look at the challenges ESG information providers face in applying the methodologies underlying ESG data accumulation and interpretation.

The Big ESG Data Challenge

Currently, ESG ratings agencies set their own data standards, methodologies, metrics, and even guide investor decision-making by assigning weightings to preferred information categories. In part they do this to assert their niche and develop brand recognition for proprietary information.

Much of the basic data in these ratings is from company produced publications for the public domain, such as sustainability reports, and audited financial statements. The outcome for investors can be confusing. Although agencies might start out with similar data, they end up producing different reflections on a company’s ESG performance. Why?

In our research among South Korean listed companies, we found a growing concern with these issues as firms develop strategies to address investor interest in ESG performance. The biggest challenges emanated from a lack of data standardization among ESG criteria by ratings agencies, as well as burdensome, confusing and contradictory disclosure requirements. This affects their willingness to comply with data requests.

Related, are differences between global and national standards, which introduces contradictions in reporting and interpretation. While keen to improve their ESG performance, we found in our interviews that East Asian companies sometimes feel compelled to conform to Western standards, despite different developmental trajectories and cultural or legal inheritances. This is particularly with respect to the social and governance pillars of the ESG framework.

An emerging methodological challenge in East Asia has consequently been divergences between companies in data disclosure approaches and practices, which feeds divergence in ESG scores, and in turn may sow doubt, and skepticism, among investors regarding the validity and value of an ESG approach.

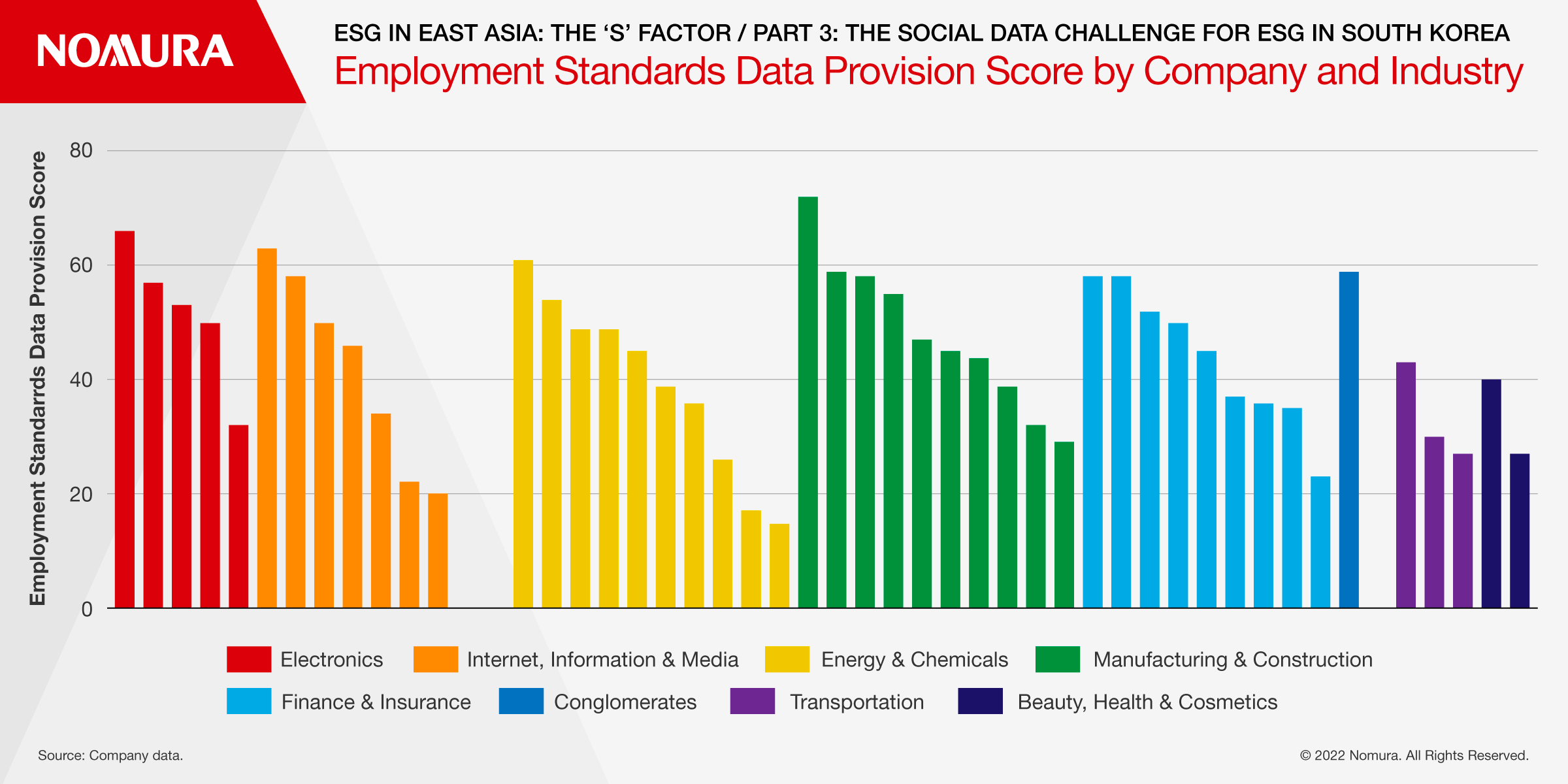

Figure 1 shows the results from our scoring of employment standards among the top 50 South Korean listed companies, divided by industrial category. While manufacturing and construction lead in their data disclosure, the graph really points to a systemic challenge, as companies in all categories diverge markedly in their public disclosures. Some companies engage enthusiastically with ESG standards, while others don’t report at all.

Figure 1 - Employment Standards Data Provision Score

If such discrepancies are spread across the whole ESG spectrum, investors need to be aware of the potential for surprises lurking in undisclosed information. Significant, we found, is the lack of disclosure caused by simple misunderstandings by companies about ESG reporting requirements that arise from unclear, overly complex, or opaque communications and reporting by ratings agencies.

One discrepancy is in companies’ interpretation of the number of employees, their gender composition across different ranks, whether they are regular or non-regular workers, and whether all employees worldwide, or just those in-country, should be disclosed in public facing ESG reporting. With a lack of standardization in public reporting of even simple numerical indicators, responsible investors need to know more about how ESG ratings agencies deal with data inconsistencies.

Clarity, Simplicity, and Transparency

There are as yet few ESG national reporting frameworks available anywhere. Nevertheless, governments and regulators are moving towards establishing reporting standards for Non-Financial Reporting, as demand grows for systematic information on corporate responsibilities.

Globally the most developed system is in the European Union, and we found an interesting contradiction within South Korean companies. On the one hand companies reported that clear, simple, and transparent reporting standards would help guide companies on what and how to report in their ESG and sustainability statements. On the other hand, companies criticised such systems for being too European – and too judgmental – of East Asian practices.

South Korean companies among many others in Asia are still new to ESG, and the demands of ratings agencies and institutional investors can feel burdensome to companies who are unaccustomed to providing comprehensive data for the public domain. Company ESG team members feel anxiety about revealing too much, and getting themselves into trouble, for example.

Nevertheless, ESG awareness is improving. Some CEOs are personally committed and are beefing up their ESG information units, while others are yet to establish a team and reluctant to engage. Without national standards and reporting requirements, however, companies currently lack sufficient incentives to comply with the ratings agencies’ requests. The result is large information gaps, and this can affect ESG performance.

In South Korea the largest companies will be required to publish ESG information from 2025 and all listed companies from 2030. It is not clear yet what the government will require, how detailed the information will need to be, and likely the majority of requirements will be environment related, to conform to 2050 carbon neutrality targets.

We emphasise, however, that employment standards underpin the whole ESG spectrum, and companies we interviewed generally concurred. In the words of one company ESG specialist, ‘I agree, because it is the employees who make decisions that impact on governance and environment’.

Conclusion

ESG reporting is proliferating globally in response to demand for greater corporate accountability. The result is a diversity of approaches, regulatory mechanisms, and methodologies being applied. ESG is still new for East Asian companies, and there is great variability in their approaches. Investors can be forgiven for feeling confused by often contradictory reports.

However, the ESG reporting challenge is multi-layered, and ensuring standardised reporting formats for numerical ESG indicators is just the top layer of a deeper set of methodologies, which we will address in our next article.

Senior Lecturer, School of East Asian Studies, University of Sheffield

Jim McCafferty

Head of Asia ex-Japan Research

Jing Wang

PhD Candidate, University of Sheffield

Yejin Shin

PhD Candidate, University of Edinburgh

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.