Economics | 0 min video August 2017

Economics | 3 min read | August 2017

Economics | 3 min read | August 2017

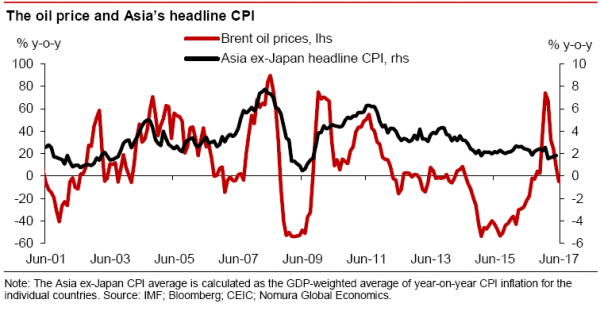

We have developed three proprietary tools to help improve our ability to forecast headline and core inflation for 10 Asian countries. One is a statistical method to estimate base effects, the second is our inflation pulses, essentially leading composite indexes of inflation comprising of upstream price indicators, and the third consists of more fundamental regression models of CPI and core inflation based on commodity prices, output gaps, effective exchange rates and country-specific factors.

Exchange rates and commodity prices can have large swings, making them inherently difficult to forecast; in short, they are the two big wild cards in forecasting Asian inflation. We therefore present a matrix of scenarios to illustrate the sensitivity of each country’s CPI inflation to movements in exchange rates and commodity prices. We identify four countries – India, Indonesia, the Philippines and Singapore – that seem most exposed to large potential future moves in the exchange rate and/or oil prices.

While useful, we are cognizant that empirical models have many limitations. Therefore, in the final analysis Nomura's country economists take the empirical analysis on board but also consider a host of other local and practical factors to arrive at their CPI inflation forecasts, which are explained in detail in the individual country pages.

Our key conclusions are:

In line with our benign CPI inflation outlook we expect most Asian central banks to keep policy interest rates at their current historically low levels for a very long time. In fact, we do not expect any Asian central bank to hike this year, or in H1 2018 for that matter; only in H2 2018 do we expect the Bank of Korea and Bangko Sentral ng Pilipinas to start hiking rates. Even in 2019, we expect only these two central banks to hike rates.

Our Asia interest rate forecasts imply a complete decoupling from the Fed, which is an extraordinary departure from past Fed hiking cycles.

Interest rate strategy: We have a constructive bias on the front end of most Asian rates curves and our Economics team’s conclusion of a benign near-term inflation picture supports our general receive bias in front-end Asia rates.

Low, or lower, inflation is one of the key reasons behind our constructive bias on front-end rates in Asia, along with stable monetary policy and, generally speaking, ample liquidity in the region’s banking systems. Indeed, it is worth noting that high real yields in Asia provide a decent cushion against the Fed and ECB policy normalization. To be clear, we do believe that the longer end of some of Asia’s low-yielding rates curves (like Thailand, Singapore, South Korea and Malaysia) are vulnerable to a rise in global yields, but even along these curves we expect the shorter end to remain relatively stable.

On the benign inflation outlook, our top recommendations are:

For further insights, see the full report here.

Head of Global Macro Research

Asia Rates Strategist

Asia Rates Strategist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Economics | 0 min video August 2017

Technology | 4 min read May 2017

Economics | 0 min podcast August 2017