Continued 'Goldilocks' economic conditions have led EM investors to view the glass as half full, but four key triggers could lead to a snapback for EM

Four potential events this year could lead to an emerging markets pricing snapback

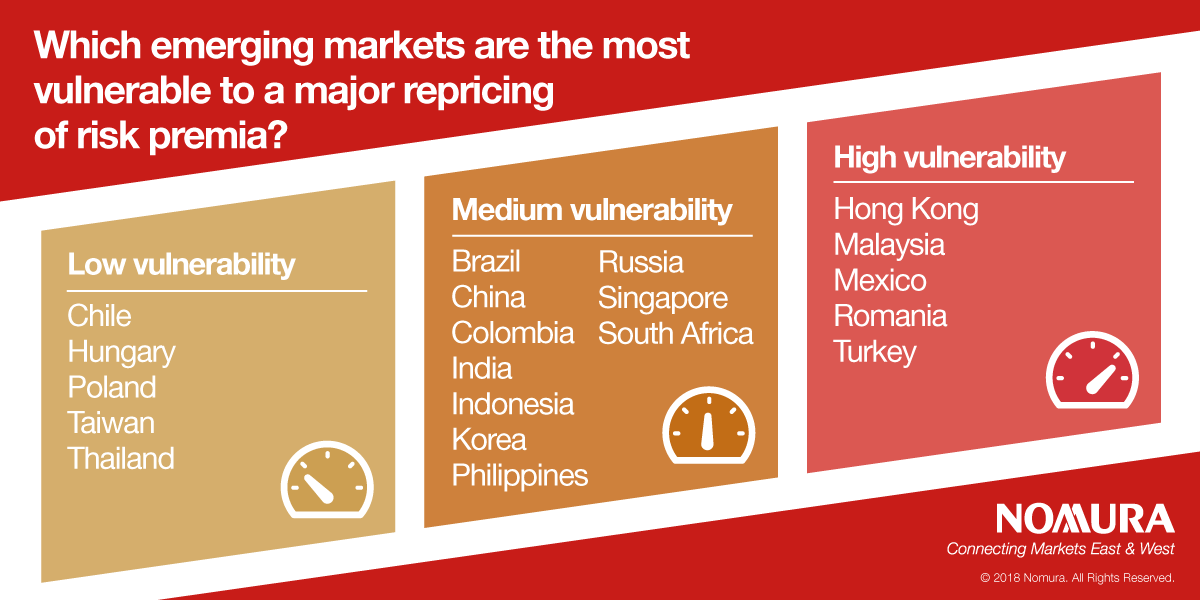

Certain emerging markets are more vulnerable than others to a major repricing of risk premia

Four triggers

1. A US bond market selloff

This year, the 10 year US Treasury bond yield has risen sharply on a firming US inflation outlook, a deteriorating US fiscal outlook and the Fed winding down quantitative easing (QE). Sharply higher US bond yields (the benchmark for the pricing of all global assets) could trigger a reappraisal of the investment risk-reward in global credit markets, sparking a major decompression of EM credit risk premia. If sharply higher US bond yields are accompanied by US dollar (USD) appreciation, the repricing of EM assets could be further amplified.

But here’s what makes it more ominous: the continued huge investor appetite for EM bonds despite worsening credit quality and declining compensation for credit risk. EM high-yield corporate bond issuance surged to a record high in 2017, and yet EM credit spreads remain compressed near multi-decade lows. The Institute of International Finance has spotted a growing disconnect between declining EM sovereign credit ratings and rising investor bond allocations to EM. Of course, there is a logical explanation for this (global QE) to which we turn next.

2. The global QE unwind

Just as QE was successful in pushing global investors into riskier, higher-yielding EM assets, the unwinding of QE will have the opposite effect, but potentially in a more non-linear fashion because of the large build-up of EM debt, complacency created by the unusually long period of very low interest rates and the speed at which market liquidity can evaporate. Currently, on a global scale, the Fed’s quantitative tightening (QT) is being more than offset by ongoing QE by the European Central Bank (ECB) and Bank of Japan (BOJ), which has stopped QE but has yet to move to QT. Assuming the ECB ceases its asset purchases in September, the BOJ continues buying Japanese government bonds at a de facto annualised rate of ~JPY45trn and the BOE continues to hold its balance sheet constant, aggregate G4 central bank QE will turn to QT in Q4 2018.

3. A China growth slowdown

In the past year, China’s economy has been a bastion of stability, and “China risk” has faded from the radar screen, however there are two reasons why we could see a slowdown in the near future.

Firstly, variables such as the decrease in shadow financing, and market speculation could have an overall impact on growth. Even though the benchmark 1 year lending rate is unchanged, banks have raised their commercial lending rates, and growth in the broadest measure of credit (aggregate financing) has slowed.

Secondly, the surge in producer price inflation last year that boosted the profits of struggling upstream State-Owned Enterprises (SOE) is fading. EM is more exposed than developed markets (DM) to a China growth slowdown, both directly through exports and indirectly through declining commodity prices.

4. Risk of a trade risk

This year, the US has taken a more aggressive stance on trade. The outcome of the Section 301 investigation, the ballooning US trade deficit with China (to a record high of USD380bn) and US midterm elections in November raises the risk of growing tit-for-tat trade friction between the US and China. After decades of trade liberalization that has driven the fragmentation of production across countries (a full one-third of the value-added in China’s exports is sourced from other countries), growing trade restrictions by the world’s two largest economies is bound to hurt exports of other countries. Here again, EM is more exposed than DM: of the world’s major economies, seven out of 10 of the most open to trade are in EM.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.