Addressing the US Affordability Crisis – Signal Versus Reality

The Trump administration has announced a range of measures aimed at addressing affordability in the run up to this year’s midterm elections including housing, healthcare and consumer finances. In our view, these initiatives are unlikely to materially alter the near-term inflation outlook

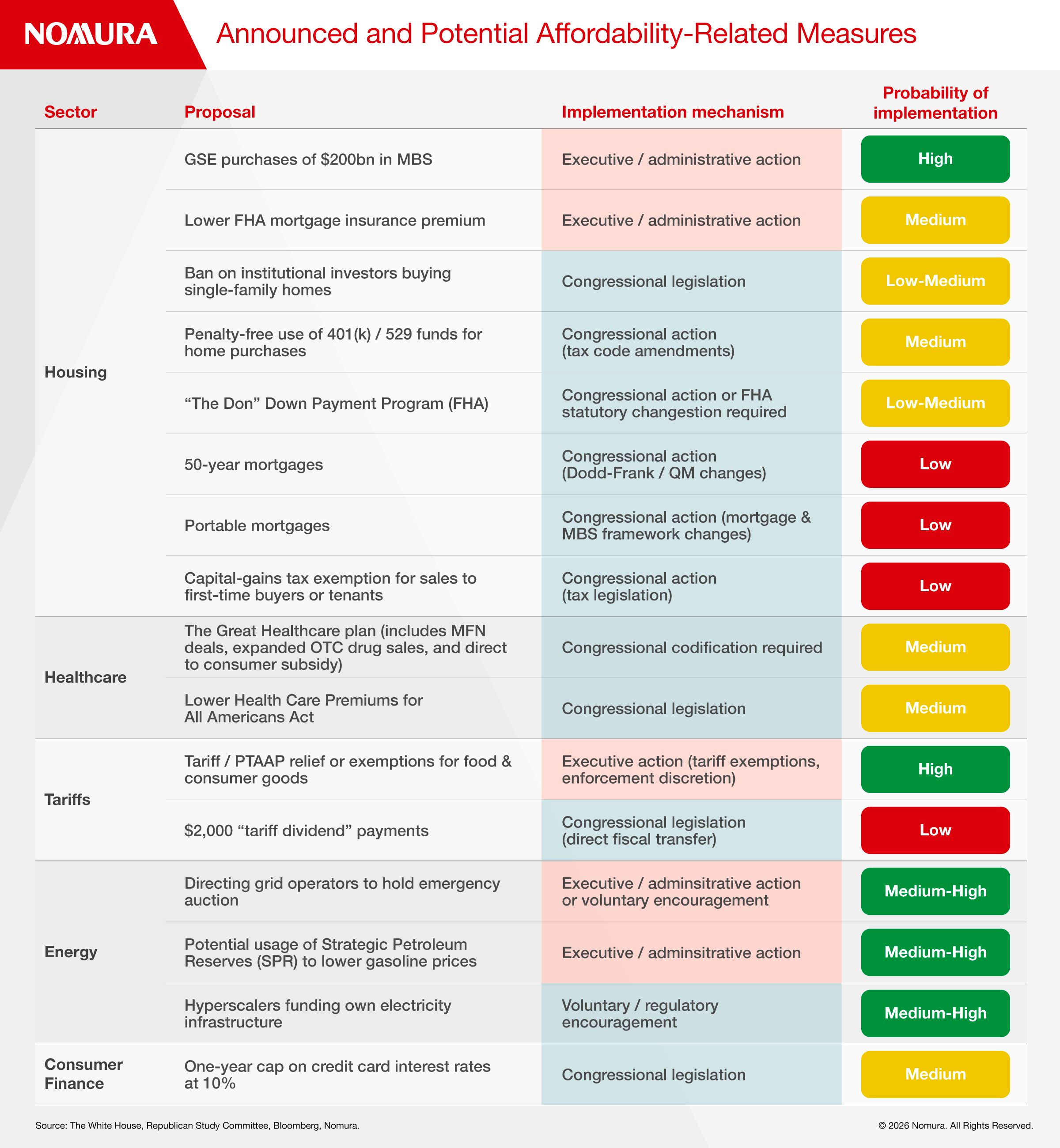

President Trump has announced affordability-focused initiatives spanning housing, trade, healthcare, energy, and consumer finance.

The majority of proposals appear to function primarily as policy signaling and could face significant legislative hurdles.

Most of the proposed policies would be unlikely to materially weigh on inflation in the near term. By contrast, some initiatives, especially in housing or $2k “tariff dividends,” could pose upside risks to inflation by boosting demand.

The Trump administration has announced a range of measures aimed at addressing affordability in the run up to this year’s midterm elections. The administration has proposed initiatives related to housing, trade, healthcare, utilities, and consumer finances.

In our view, these initiatives are unlikely to materially alter the near-term inflation outlook. This reflects three factors:

1. Legislative and implementation constraints: The majority of these proposals would likely require congressional authorization, with only a limited subset achievable via executive or administrative action. Consequently, the probability of passage for most measures appears low, and implementation timelines are long, even where political support exists.

2. Focus on affordability rather than inflation: Even if enacted, we believe most of these initiatives are aimed at addressing affordability and not inflation. On the contrary, many proposed policies carry upside inflation risks. Housing measures aim to lower mortgage rates or upfront costs, while interest rate caps on credit cards and $2k tariff dividends are aimed at boosting savings. Most of these policies may stimulate demand, particularly against the backdrop of fiscal stimulus from the One Big Beautiful Bill Act (OBBBA).

3. Disinflationary measures are back-loaded: Healthcare and energy measures are likely to be disinflationary, but only in the medium to longer run owing to regulatory complexity, and investment lags. A notable exception is tariff relief, which could help provide imminent relief for some select goods prices.

Housing

Most housing-related measures are designed to lower mortgage rates, reduce upfront financing costs, and expand homeownership opportunities. This agenda could help with affordability but not necessarily inflation. These measures do not directly address supply constraints and may boost demand, raising the risk of price or rent pressures.

GSE purchases of $200bn in MBS

This is likely to lower mortgage rates on the margin. This does not require congressional action.

Ban on institutional investors purchasing single-family homes

We estimate this would have a limited impact on the housing market, as institutional buyers account for only a small share of total transactions. Owner-occupied supply could rise, but rental supply could fall, potentially pushing rents higher in some regions. This would require congressional action.

Lowering FHA mortgage insurance premium

This would likely help reduce monthly premiums and improve consumers’ financial situation. This could be implemented via executive action.

50yr mortgages

These would lower monthly payments but materially increase lifetime interest costs. Current rules under Dodd-Frank and qualified mortgage standards effectively limit mortgage terms to 30 years, and therefore this policy would require congressional action.

Portable mortgages

Thispolicy would allow homeowners to carry their existing mortgage rate to a new property, potentially increasing turnover and supply. Implementation would be complex and potentially disruptive to the MBS market. Moreover, it likely applies only to future originations, implying no near-term impact. The policy would require congressional action.

Allowing penalty-free access to 401(k) and 529 funds for home purchases

This proposal would permit withdrawals for down payments without the current 10% early withdrawal penalty. It could support demand, but risks weakening retirement and education savings. This requires congressional changes to tax laws.

“The Don” Down Payment Program (FHA)

A proposal in the reconciliation 2.0 package, it is a zero or low down payment FHA option for creditworthy borrowers. This would expand access to credit, but could raise demand pressures without a corresponding increase in supply. This requires congressional authorization or FHA statutory changes.

Capital gains tax exemptions for home sales

Another reconciliation 2.0 proposal, eliminating capital gains taxes on sales to first-time buyers or on rental home sales to tenants could modestly increase turnover, but does not directly increase housing supply. This requires congressional action.

Consumer Finances and Fiscal Transfers

Measures targeting consumer finances are primarily aimed at reducing interest burdens or augmenting household cash flow, rather than restraining prices. These policies may support consumption and demand, posing upside inflation risks over time, particularly in a fiscally accommodative environment.

10% interest rate cap on credit cards

Trump proposed a one-year cap on credit card interest rates of 10%. This would support cashflows for some borrowers, but some banks have flagged that it could lead to reduced lending to subprime and below borrowers. This has received a mixed reaction from stakeholders, and the proposal would require congressional legislation.

$2k “tariff dividend” payments

This proposal is a cash transfer aimed at offsetting rising costs, analogous to pandemic-era stimulus or Japan-style rebates. While supportive of household balance sheets, such transfers could add to inflationary pressures and would require congressional approval.

Healthcare

Healthcare is one of the few sectors where policy could significantly affect inflation, as demonstrated by prior reforms such as The Affordable Care Act, Budget Sequester in 2013, and Medicare Access, and CHIP Reauthorization Act (MACRA). Trump’s policy proposals largely require congressional action though, and even if enacted, the disinflationary impact is likely to be back loaded.

The Great Healthcare Plan

There are various features of the plan that require congressional codification.

Most-Favored-Nation pricing / TrumpRx: Codifying the administration’s MFN deals (i.e., voluntary agreements with drugmakers to tie prescription prices in the US to the lower rates available to other nations).

Allowing and expanding the sale of more drugs over-the-counter.

Lowering insurance premiums / sending payments directly to consumers: Enacting a statutory change to send money directly to consumers rather than subsidy payments to insurance companies.

Lower Health Care Premiums for All Americans Act

This proposal would expand Individual Coverage HRAs and offers two-year, per-employee tax credits for firms with fewer than 50 employees. It has been passed in the House and requires Senate passage.

Tariff-related measures

We believe lowering tariffs would be one of the most effective ways to achieve immediate price relief. The administration took note of rising prices for certain food components and exempted them from reciprocal tariffs last year, including bananas, coffee, beef, and tomatoes.

The administration has over time expanded tariff exemptions, and the relief has skewed to consumer goods. Tariff reductions could be done via executive action.

Energy

Efforts to lower electricity prices are unlikely to generate sustained near-term disinflation, due to long construction timelines, regulatory constraints, and rising demand, particularly from data centers. Electricity price inflation has outpaced headline inflation in recent years, and structural pressures remain.

Directing grid operators to hold emergency auction

Trump and US Northeast governors, have directed the largest grid operator to hold reliability power auctions to build more power plants and prevent supply shortfalls. Such auctions would give hyperscalers the opportunity to bid for power generation. This is likely to be a directive and would be disinflationary in the longer term.

Hyperscalers funding their own electricity needs

Trump has encouraged hyperscalers to bear the cost of their energy demand. This is primarily a voluntary, negotiated approach. While utility rates are state-regulated, FERC could encourage or facilitate such arrangements.

Potential usage of Strategic Petroleum Reserves (SPR) to lower gasoline prices

The US is reportedly exploring a plan to exchange heavy Venezuelan oil for US medium sour crude to fill up the SPR. Note, nearly 70% of US

refining capacity runs most efficiently with heavier crude. Though it won’t lead to sustained disinflation, an increase in the SPR could help to prevent or offset sudden spikes in energy prices.

The bottom line

Overall, we expect the transmission of affordability policies to inflation to be modest in the near term. Many of the policies under consideration could provide a pro-cyclical stimulus, boost demand, and pose upside risk to inflation. Legislative hurdles and implementation lags would limit the passthrough to consumer prices, even for healthcare and energy initiatives.

We continue to expect the Fed to remain on hold for the remainder of Chair Powell’s term, followed by 25bp cuts in each of June and September.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.