Companies host earnings calls to report financial results to investors and shareholders, and these calls importantly provide more than just financial information. They offer prepared language by the company and carefully worded responses to analysts’ questions. There is often a hidden narrative that can be easily missed.

In this report, we show how we use Natural Language Processing (NLP) Artificial Intelligence to interpret the language of earnings calls in the context of ESG. We then use this understanding to generate an ESG score for the company and to guide stock selection.

Systematic strategies using this approach have worked very well in our seven-year out-of-sample back-tests, and have performed especially well over the past few years – a period during which systematic stock selection strategies have performed miserably.

Stock Selection Based on ESG Narratives

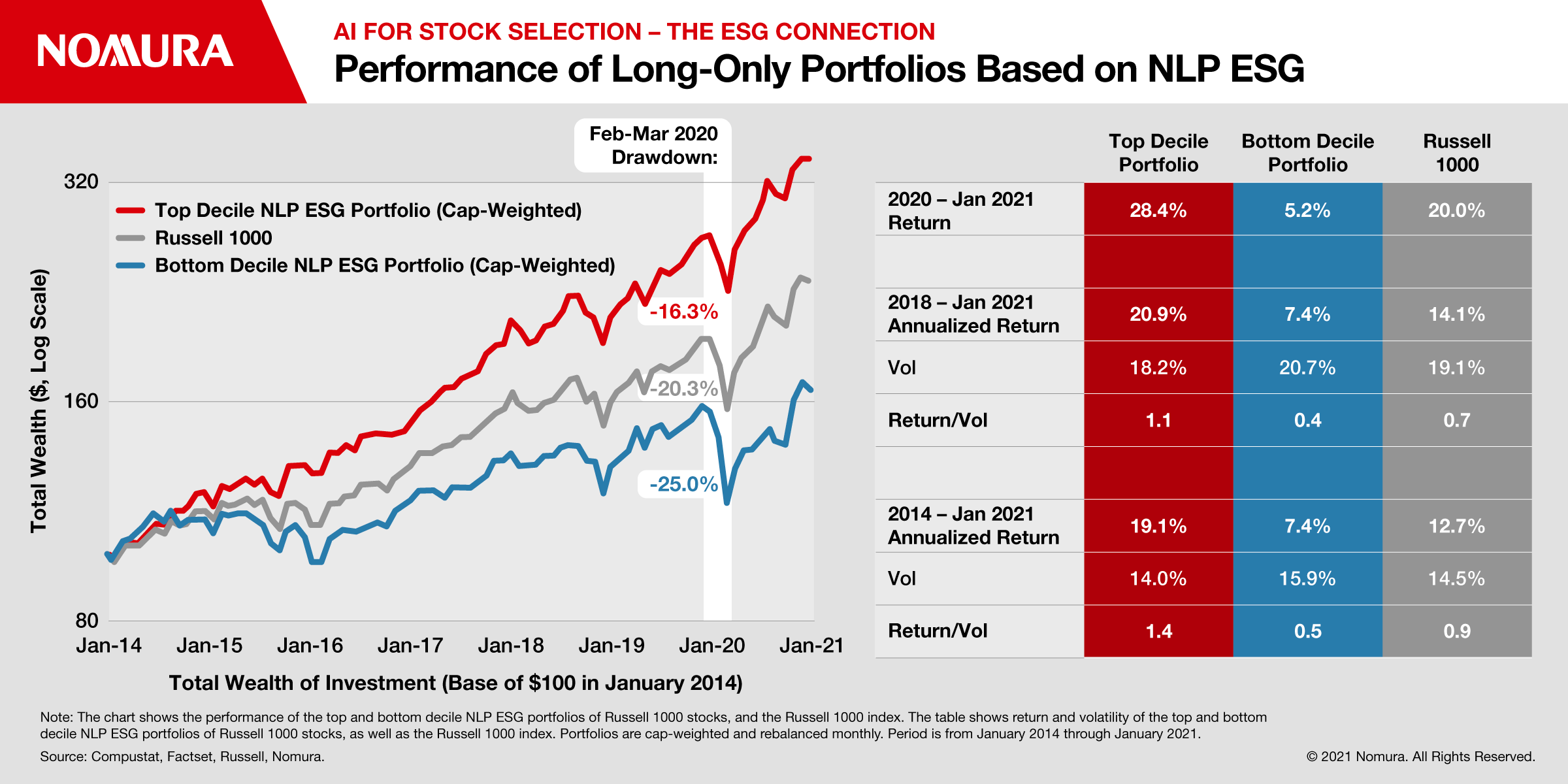

First, we’ll show what is achieved for stock selection. In Fig. 1, we show the cumulative wealth for three long-only portfolios: The top NLP ESG-ranked decile of Russell 1000 stocks, the Russell 1000 index, and the bottom NLP ESG-ranked decile of Russell 1000 stocks.

We trained our NLP algorithms on text from earnings call transcripts from 2007 through the end of 2013, so the results plotted in Fig. 1 are out of sample. It shows that the top NLP ESG-ranked Russell 1000 stocks produced superior returns and risk-adjusted returns compare to the Russell 1000 index.

The bottom-ranked ESG stocks, by contrast, generate inferior returns and risk-adjusted returns compared to the Russell 1000 index. The drawdown in the Covid-19 market collapse of February-March 2020 highlights an important feature of this ESG ranking. The drawdown of the Russell 1000 was -20.3% in the collapse, significantly better than the -25.0% drawdown for the bottom-ranked ESG stocks but worse than the -16.3% drawdown for the top-ranked ESG stocks.

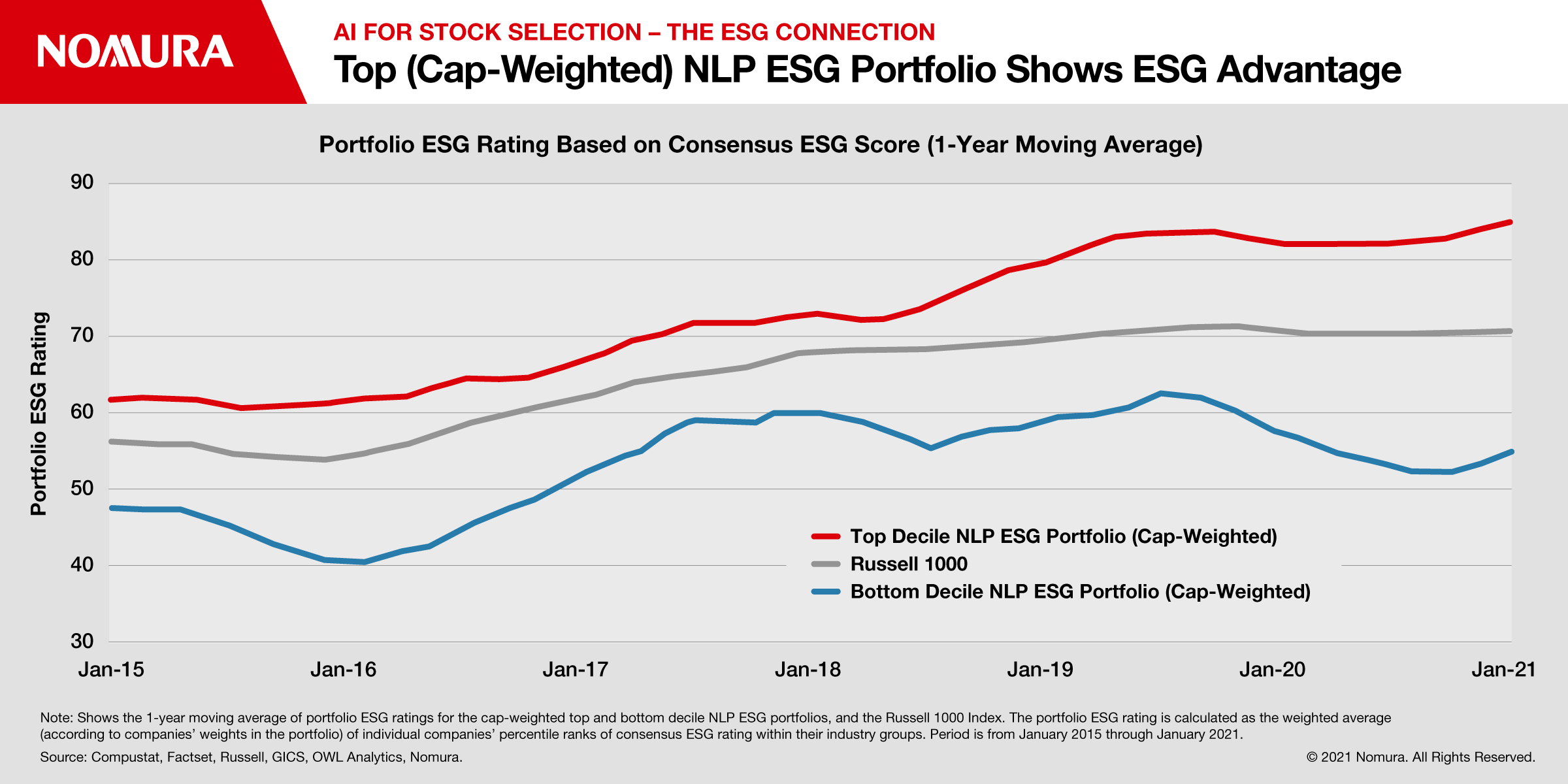

But a question remains: How do we know the top NLP ESG portfolio in Fig. 1 really has better ESG quality than the Russell 1000 benchmark and the bottom NLP ESG portfolio? In our previous report, “A Measured Approach to ESG Investing,” we described why a portfolio ESG rating should not be measured by aggregating company-level ESG ratings from any single provider. Instead, we use consensus company-level ESG ratings across a wide range of providers to calculate an aggregate portfolio ESG rating.

Fig. 2 shows the consensus-based ESG ratings for the portfolios in the long-only strategies displayed in Fig. 1. The top NLP ESG-ranked portfolio (red line) achieves a clearly higher consensus-based portfolio ESG rating than the Russell 1000 benchmark (gray line), which in turn has consistently higher consensus-based ESG rating than the bottom NLP ESG-ranked portfolio (blue line). Thus, the top decile NLP ESG-ranked portfolio achieves both superior performance (Fig. 1) and better ESG quality (Fig. 2).

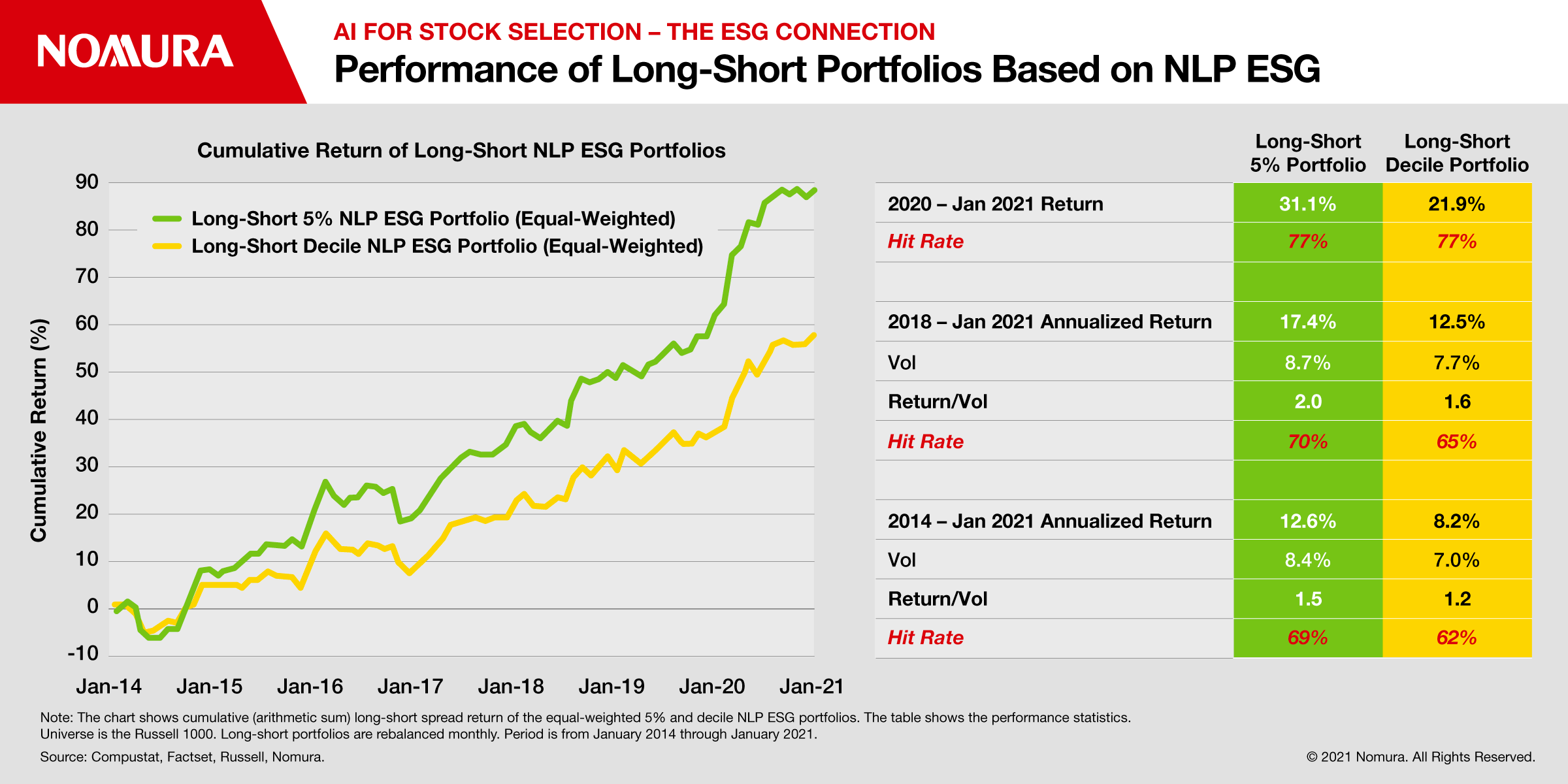

Now, given the performance contrast between the top and bottom NLP ESG-ranked stocks evident in Fig. 1, a long-short strategy makes sense (long the top NLP ESG-ranked stocks and short the bottom NLP ESG-ranked stocks).

The yellow line in Fig. 3 represents the same top and bottom NLP ESG-ranked decile of stocks used earlier, but combined into a single long-short portfolio. These portfolios are rebalanced monthly, as in Fig. 1, but they are equal-weighted rather than cap-weighted to reduce portfolio concentration.

The reduced concentration achieved by equal-weighting the portfolio enables us to build an even more ESG-focused long-short portfolio based on the top and bottom 5% NLP ESG ranked Russell 1000 stocks (i.e., top 50 stocks vs. bottom 50 stocks). This produces even better returns than the long-short NLP ESG decile portfolio.

Fig. 3 shows cumulative spread returns for both the long-short NLP ESG decile portfolio (yellow line) and 5% portfolio (green line). The performance summarized in the table is stellar, especially for the 5% long-short strategy.

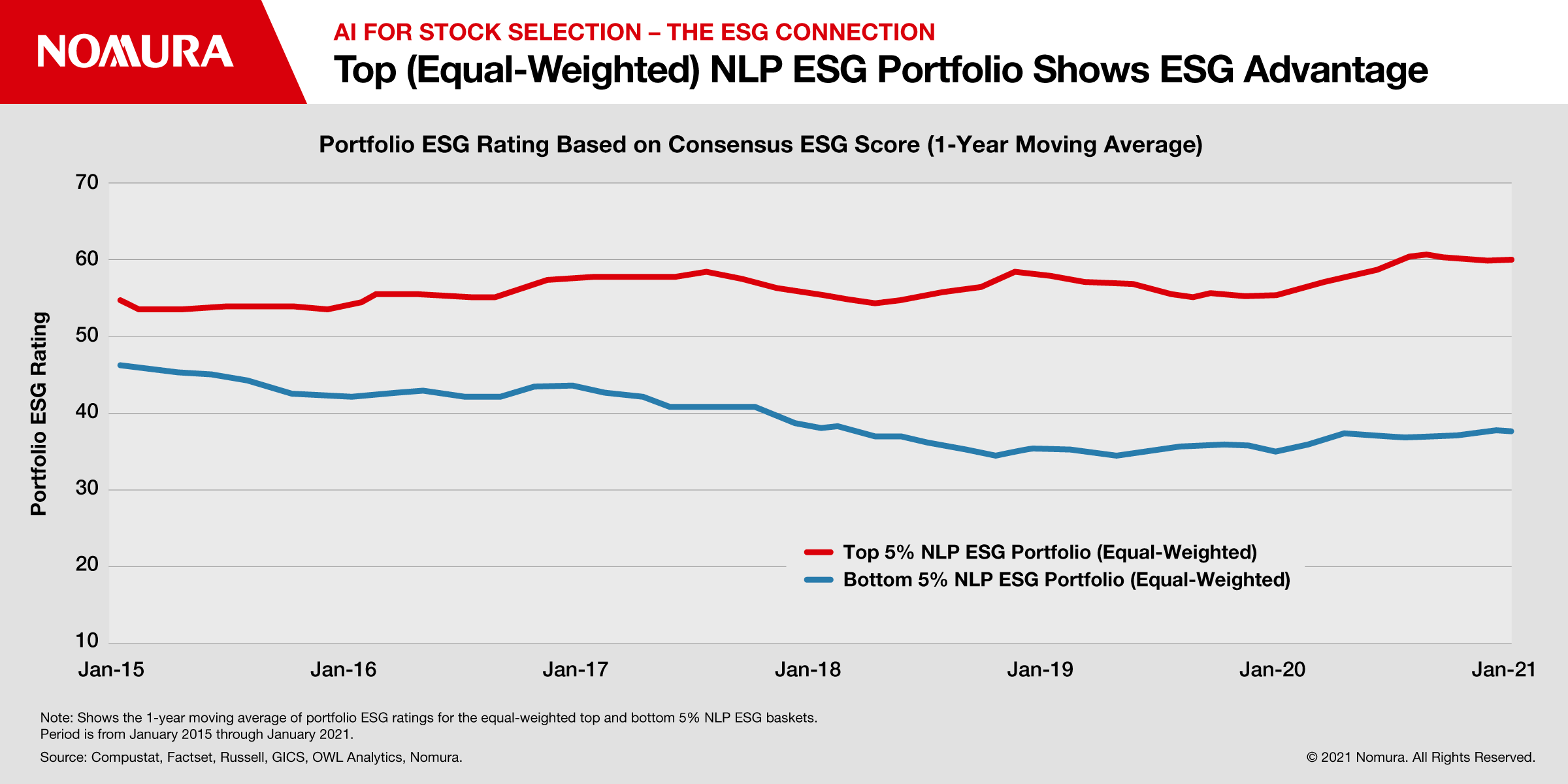

Similarly to Figs. 1 & 2, the portfolio ESG ratings of the equal-weighted top and bottom 5% NLP ESG-ranked portfolios used to generate the results in Fig. 3 are shown in Fig. 4. These ratings are also calculated using company-level consensus ESG ratings, which do not include our proprietary NLP ESG ratings that we used to construct the portfolios. The equal-weighted top 5% NLP ESG portfolio shows an ESG advantage over the equal-weighted bottom 5% NLP ESG portfolio.

What Drove the NLP ESG Strategy’s Success?

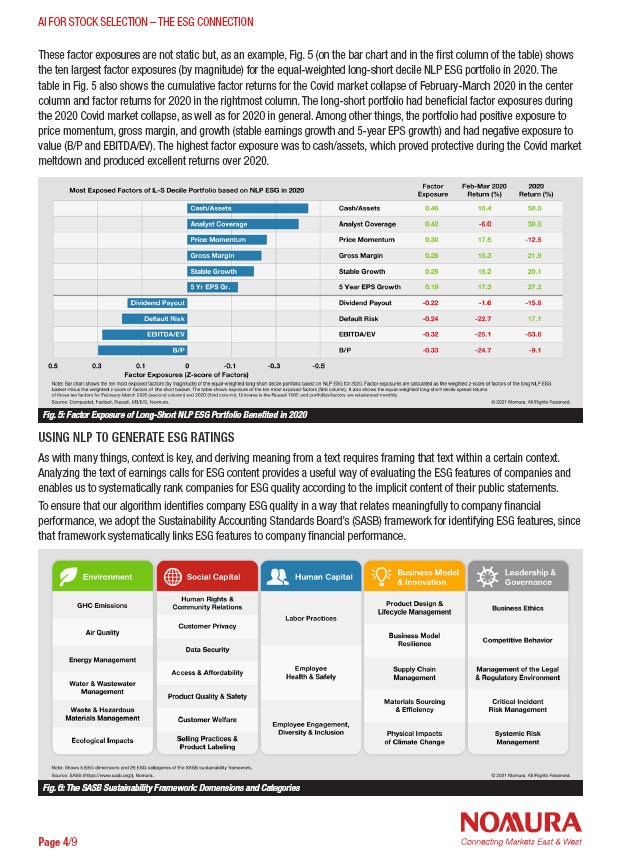

The long-short performance shown in Fig. 3 is impressive, especially given the generally terrible performance of long-short quant equity strategies in 2018-2020. We attribute some measure of this success to the fact that good ESG quality dynamically nudged the NLP ESG portfolios into beneficial factor exposures.

Read more on the success of the NLP ESG strategy by clicking the link on the right or below to download full report.