Despite US tariffs, Asia’s growth has so far been resilient – strong demand in artificial intelligence continues to power tech exports, while stock markets rally. So, has Asia evaded the tariff bullet? Is a broad-based cyclical upturn around the corner?

The region has shown resilience, though with marked sectoral divergences. Strong AI-related demand, gradual tariff implementation, frontloading and robust government infrastructure spending have supported both exports and fixed investment, despite trade policy uncertainties. However, August data revealed early signs of moderating exports to the US.

Consumption remains the weakest link across Asia, having slowed due to the fading post-pandemic demand surge and the lagged effects of higher living costs and interest rates. Nomura economists note that growth in motor vehicle sales – a key proxy for discretionary demand – is contracting in six out of 10 economies.

Growth outlook points to a broader slowdown

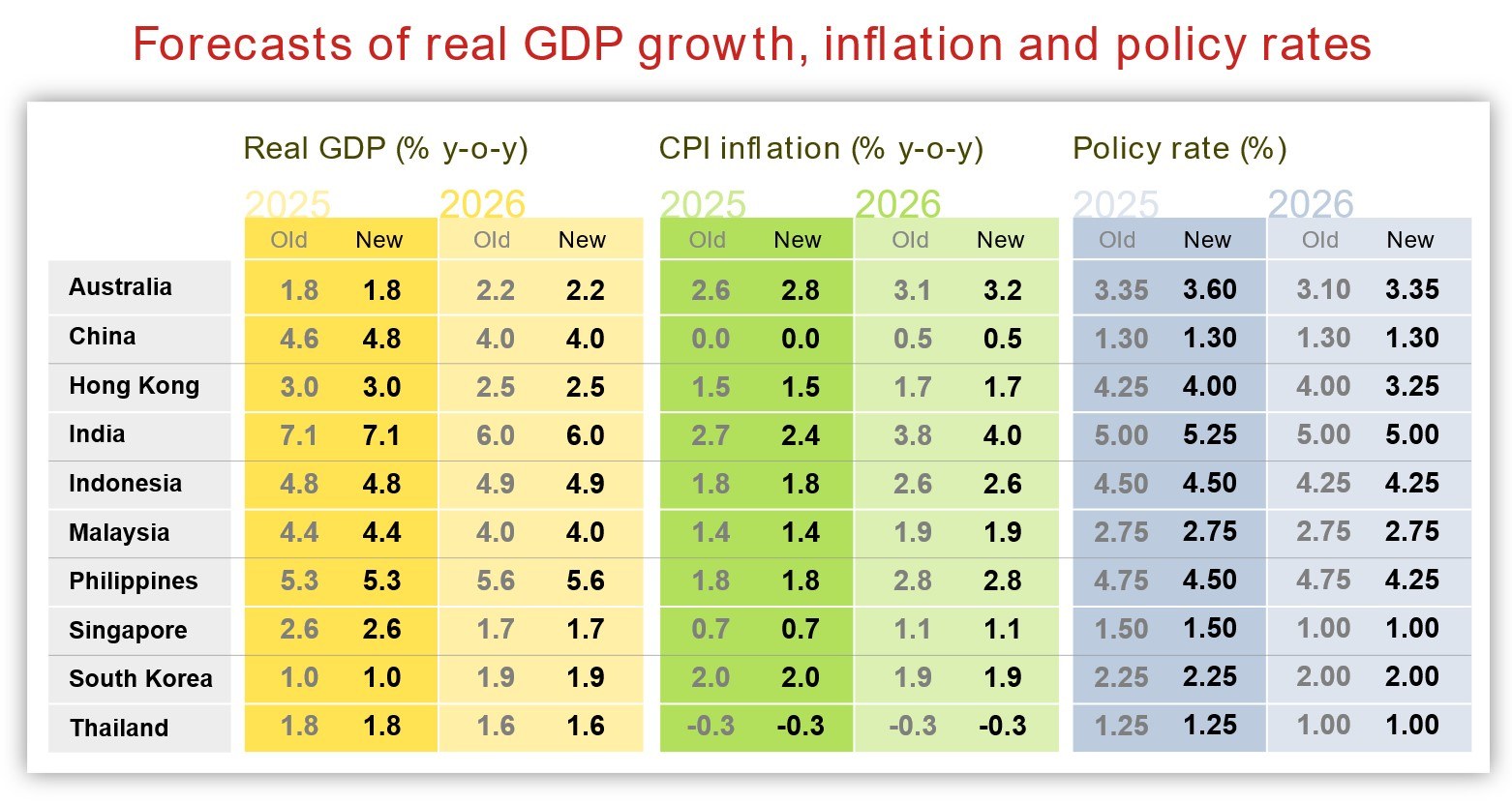

Looking ahead, we expect Asia's growth momentum to moderate more broadly, though with a shift in composition as consumption gradually improves, while investment and exports slow. Our projections show Asia ex-Japan GDP growth slowing from 4.7% y-o-y in Q2 to 3.1% by Q2 2026.

The recent resilience in exports appears unsustainable. Asian exporters have only partially absorbed US tariffs, suggesting price increases in more price-elastic categories, such as apparel and furniture, will likely dampen demand. The World Trade Organization (WTO) projects world trade volume growth to slow sharply to 0.5% y-o-y in 2026 from 2.4% in 2025.

Fixed investment across Asia also faces headwinds. Non-tech firms face margin pressures

from tariffs, while China's anti-involution campaign is weighing on EV, battery and solar investments. Government capex is also likely to slow in the Philippines (flood control project concerns), India (revenue constraints) and Thailand (election-related budget execution delays). The recent slowdown in capital goods production is an early sign of a broader slowing of fixed investment growth.

In contrast, our economists believe consumption demand may stabilize, supported by multiple factors: rising real incomes due to low inflation, targeted government fiscal measures, monetary policy transmission, and positive wealth effects in some economies. With no major layoffs despite subdued job growth, consumer spending has room to recover.

A concentrated recovery

The tech sector remains a bright spot. As per Nomura tech analysts’ estimates, US cloud service provider capex is projected to rise by 30% y-o-y in 2026, sustaining high-end chip demand. The WTO estimates AI-related trade with Asia, comprising high-value chips and advanced telecom equipment, rose by a robust 25.2% y-o-y in Q2, and contributed nearly two-thirds of global AI-related trade growth in H1 2025.

A memory supercycle also looms. Nomura’s tech analysts expect dynamic random-access memory (DRAM) prices to surge 33% y-o-y in 2026 and NAND flash memory prices to rise by 27%, on strong AI and conventional server demand, while supply is limited. Such a phenomenon should benefit Korea. Low tech inventories contrast with high non-tech stockpiles, which suggest potential for tech restocking ahead.

However, broader economic spillovers from such a concentrated recovery should be limited.

While AI-demand boosts high-end chip exports, high-end capex is less employment-intensive and relies heavily on imported equipment. We see new capex concentrating in the US. Wealth from stock market gains also tend to concentrate within a small segment, and in the case of China, household assets remain predominantly concentrated in property rather than equities.

This tech versus non-tech divergence favors economies such as Korea and Singapore as outperformers, while those less focused on tech and have benefited from US frontloading, such as India and parts of ASEAN, face increased growth risks.

Policy outlook

Most Asian central banks have slowed their pace of policy easing after reaching neutral rates, and are preserving policy space for future growth shocks. In India and ASEAN, where growth remains sluggish, additional easing appears likely. We expect a further 50bp of cumulative rate cuts in India, Philippines, Indonesia and Thailand.

However, rising housing/stock prices complicate policy choices for Northeast Asian central banks. In Korea, our base case is policy rates on hold going forward, given rising financial stability risks and better than expected growth outlook. In China, we expect policymakers to resist high profile monetary easing that could further fuel the stock market rally, but will step up its stimulus once market enthusiasm cools. Supporting domestic demand without fueling asset price inflation will be a tough balancing act for these central banks.