The joint US-Israel military operation has triggered Iran’s retaliation against energy infrastructure in the Gulf, and the Strait of Hormuz has ground to a halt as commercial shipping operators and insurers have withdrawn from the route. Very large crude carrier spot rates (from Gulf to Asia) have jumped by a whopping 1100% this year. Prices are up across the energy supply chain since mid-February, with the sharpest price increases in jet fuel (155%), followed by gasoil (62%), Liquefied Natural Gas (LNG) (58%), gasoline (37%), Brent crude oil (24%) and coal (11%); even fertilizer prices have started drifting higher. Qatar, which exclusively supplies its gas via the Strait of Hormuz, declared force majeure after its export facility was hit by Iranian drones, suspending delivery of contracts.

Asia’s exposure to the Hormuz shock

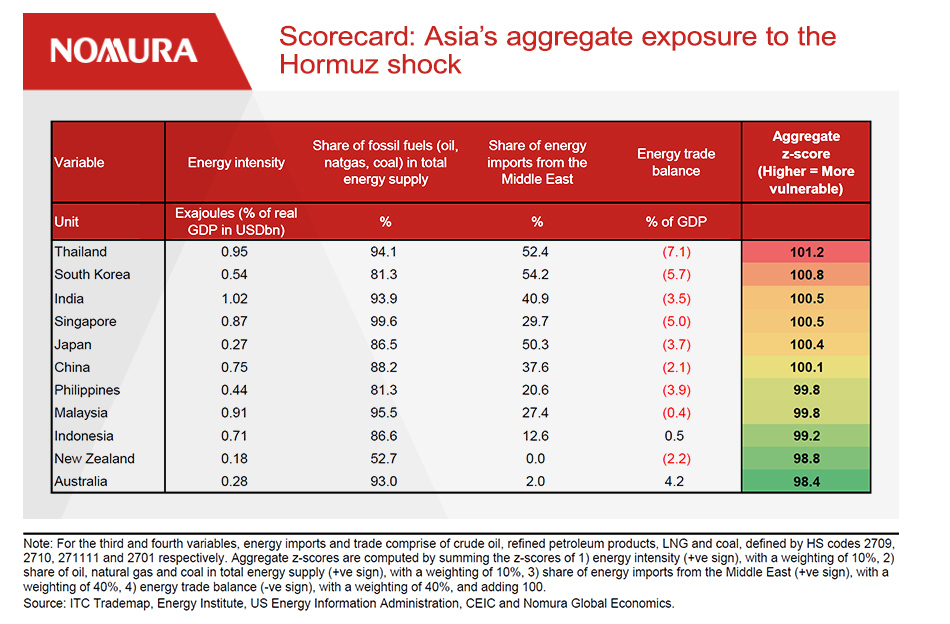

To identify Asia’s exposure to the ongoing energy shock, we analyze four parameters: energy intensity (fossil), energy mix, energy trade balance and the region’s dependence on the Strait of Hormuz.

The energy intensity and sources of energy used for consumption determine how vulnerable countries are to the Hormuz shock. Most of Asia’s energy demand is met via the supply of oil and coal. Asia is a net importer of crude oil, petroleum products, LNG and coal, making the region very sensitive to higher energy prices.

Among Asian countries, dependence on the Middle East across energy products is the highest in South Korea, Thailand, Japan and India. Japan and the Philippines source over 90% of their crude oil from the Middle East, and India sources 60% of its LNG from the region, which exposes them to concentration risk.

Using a scorecard approach (figure 1), our results show that Thailand, South Korea and India are among the most vulnerable to an energy shock, both via price and volume effects. On the other hand, Australia and Malaysia are the least vulnerable, and should benefit from positive terms of trade.

Alternative supply and buffers available to Asia

Faced with a dual price and volume shock, Asian policymakers are activating contingency plans, including drawing from government and private sector-held inventory of crude oil and petroleum product reserves, using alternate transit routes, alternative energy sources and fiscal policy as a wedge to protect consumers. We believe Asia has the inventory to tide over a few weeks, beyond which these alternatives are not enough to fully offset the supply disruption.

Countries are also looking to diversify their sources of their energy imports, as OPEC+ spare capacity (concentrated in Saudi Arabia and UAE) is trapped behind the Strait of Hormuz blockade. Global alternative supply sources include the Americas (US, Brazil, Venezuela), Central Asia, and West Africa (Nigeria, Angola). India has also received the waiver to buy Russian oil. Most of these alternative options will likely be tapped, but it will involve higher transportation costs.

Another near-term option is to switch to other energy sources. Asian countries can increase the use of coal for power generation or ramp up utilization of existing nuclear or renewable energy capacity to reduce demand for oil and gas. This means that the rise in oil and gas prices may soon trickle more broadly into other energy sources, as substitution takes place.

We expect to see fiscal policy intervention in coming weeks to protect consumers from higher energy prices. Domestic fuel pump prices are likely to stay unchanged in most Asian countries, while higher energy prices will be reflected in higher fiscal burdens, both off-budget and on-budget. We expect a mix of higher subsidies to consumers or transport operators, domestic fuel excise tax cuts and lower import tariffs on crude oil and refined products.

The Iran conflict is a stagflationary shock for Asia

Higher energy prices combined with the blockade of the Strait of Hormuz have triggered both price and volume shocks. The ultimate impact will depend heavily on the duration of the disruption.

The impact from no alternative gas supply to Qatar is already here: Indian gas firms have cut supply to their industrial customers by 10-50% with immediate effect, which in turn could hit production of downstream sectors such as power generation, fertilizer, chemicals & petrochemicals, steel, glass and ceramics. Higher fertilizer prices could raise food prices over time, disproportionately hurting lower-income consumers.

To preserve domestic supply, countries are restricting exports of petroleum products, but this can exacerbate the supply shortage at the global level and push prices even higher. The Iran conflict is also a stark reminder of the importance of building strategic petroleum reserves. Even when the crisis ebbs, demand for inventory building will likely increase.

The Strait of Hormuz is one of the world's most critical chokepoints, and in an integrated world, its blockage is beginning to trigger energy security concerns, and a cascading series of supply chain disruptions, with Asia at the epicenter of its impact.