In Asia, tech exports and production have rebounded strongly in recent months, while non-tech sectors have been tepid. This divergence has been broad-based, and is most evident in Thailand, India, Malaysia, South Korea and Indonesia, driven by both cyclical and structural forces.

Frontloading, higher chip prices and strong AI demand drive tech outperformance

In anticipation of US tariffs on chips and electronics, frontloaded demand from the US for tech categories such as computers, cell phones and telecom equipment have boosted exports, with rerouting prevalent in some ASEAN economies. China’s consumer trade-in program, which subsidizes goods including digital products, may have also lifted demand for computer and smartphone components. Rising memory chip prices are additionally giving the value of chip exports a boost.

Supported by enterprise adoption and commercialization of Generative AI, the demand for AI tech has been a key structural driver propelling the sector. However, unlike traditional infrastructure investments like roads and bridges, AI tech-driven growth is more capital intensive and has lower multiplier effects on upstream sectors, especially when high-end semiconductor manufacturing equipment is mostly imported. This leads to a concentration of profit and wage income in the hands of a few.

Soft consumption and China’s overcapacity weigh on non-tech sectors

Demand outside of the US, including from Europe and China, remains tepid. Within Asia, domestic consumption is subdued across Indonesia, Korea, Thailand and India, reflecting the lagged effects of policy tightening and the scarring effects of the pandemic. Sectoral tariffs on autos and auto parts, steel, and aluminum have led to weak export performance in autos and basic metals. Lower commodity prices are also weighing on commodity exports.

In China, overcapacity is both a cyclical and structural challenge. Even before Trump 2.0, Asian economies were suffering from a flood of imports from China. Higher US tariffs on China are driving Chinese companies to other markets, increasing competition among Asian exporters. This is weighing on industrial production and resulting in job losses in labor-intensive sectors in Thailand and Indonesia, delaying private capex in India, and adding to disinflation in the metals and chemicals sectors. All these factors are eating into non-tech sectors’ export market share globally.

ASEAN in a vulnerable position

As the economic recovery narrows, Nomura economists expect a broader downshift in Asian growth. ASEAN economies are particularly vulnerable, given the frontloading seen in Q2, high exposure to China’s overcapacity, increased US scrutiny on transshipments, and limited participation in the AI value chain. A few Asian economies can still benefit from structural tailwinds on AI and supply-chain shifts, although some cyclical spillovers are inevitable.

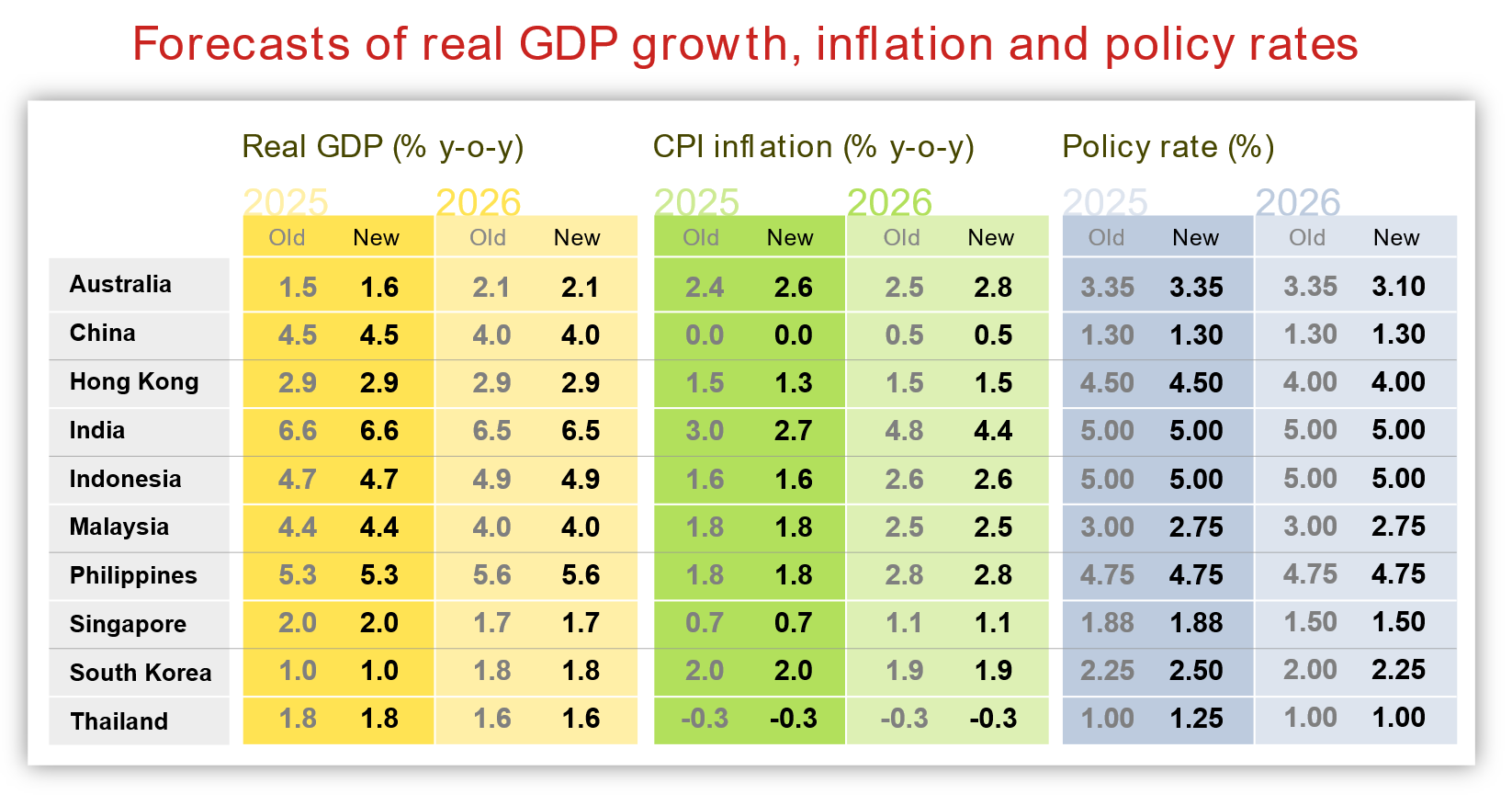

On monetary policy, Asian central banks recently surprised markets by shifting gears from accommodative to neutral, with the Bank of Thailand looking to preserve policy space, the Bank of Korea focusing on financial stability risks, and the Reserve Bank of India changing its stance to neutral. However, with a likely growth downshift and US tariffs back to Liberation Day levels, the second leg of Asia’s easing cycle could begin soon.

For our economists' complete views, read the full report.