Central Banks | 4 min read April 2026

Economics | 3 min read | April 2026

China’s Unique Advantage in the Global Energy Crunch

Chinese exporters may inadvertently stand to gain from a global shock

Economics | 3 min read | April 2026

Chinese exporters may inadvertently stand to gain from a global shock

The Iran war and the closure of the Strait of Hormuz have driven global energy prices sharply higher. Benchmark prices of LNG in East Asia and Europe have increased by 87.7% and 58.7%, with Brent crude oil also up 79.3% in March.

Many might assume China is the most vulnerable to these disruptions, as the world's largest energy consumer and net importer of crude oil and natural gas, with 38% of its oil and 23% of its LNG transiting through the Strait of Hormuz.

With the rapid growth of electrification, manufacturing has become increasingly dependent on power supplies across the world. With about 20% of global LNG and oil supply blocked by the Strait of Hormuz closure, manufacturers in import-dependent economies suffer from surging electricity prices.

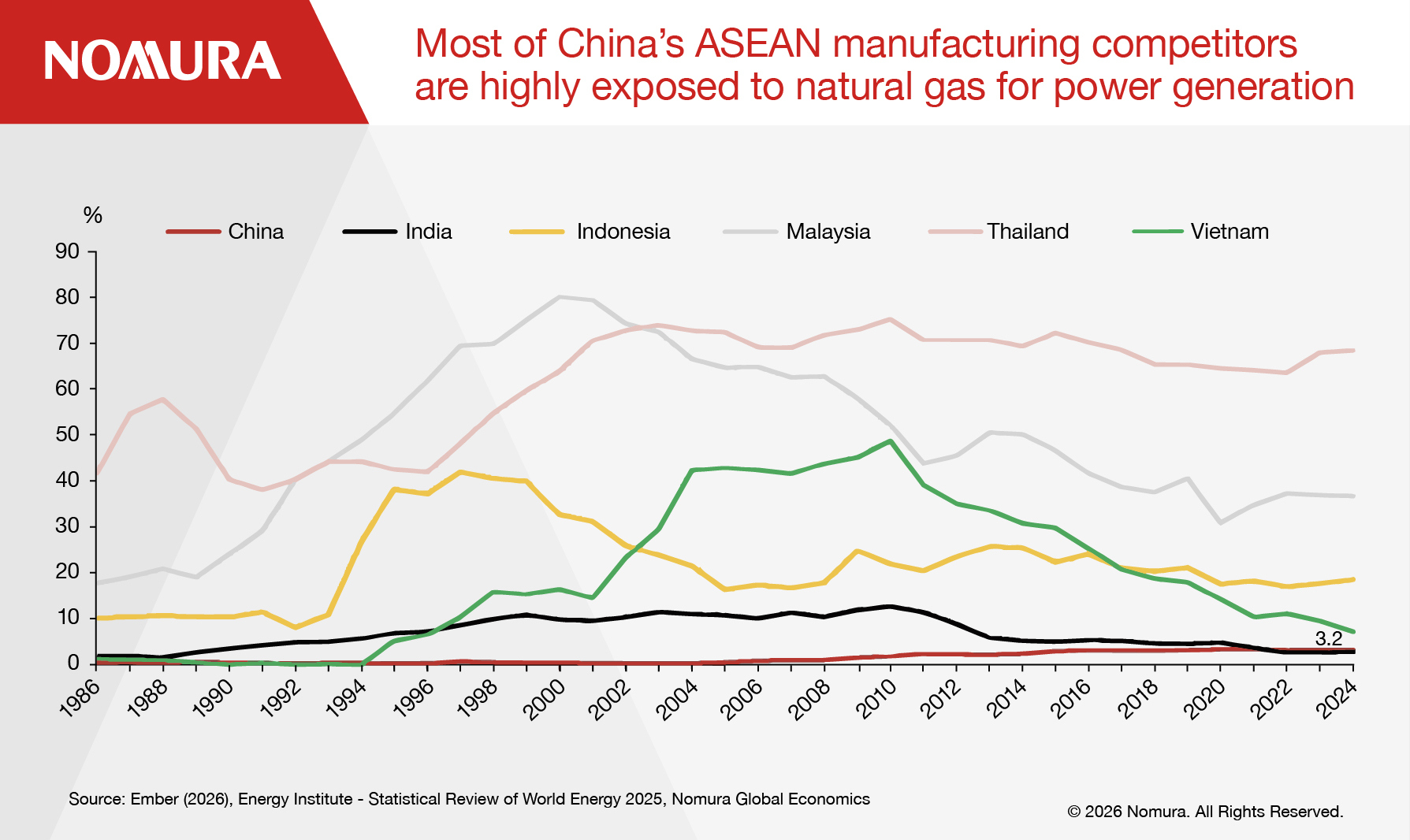

Indeed, China appears less exposed to the Strait of Hormuz closure than most other industrial economies, particularly those in Asia. China is the world's largest energy producer with low overall external energy dependency and relies heavily on domestic coal and rapidly expanding renewables – oil and natural gas represent only 18% and 8% of China's energy consumption, respectively. Energy flows via the Strait of Hormuz accounted for only 6.6% (oil) and 0.6% (gas) of China's total energy use.

China has been the world's largest exporter since 2009, accounting for 30% of world production and 25% of manufactured exports in global trade. Exports have been China's primary growth driver since 2020, surging by 45.6% through 2025 and advancing 21.8% year-over-year in the first two months of 2026.

The current energy crisis threatens this momentum. Chinese exporters may face headwinds from the global demand destruction, inflated transportation costs and severe shortages of oil-dependent raw materials. This energy shock might be the most severe challenge faced by Chinese exports in decades.

However, China’s exporters have weathered major crises over the last six years, from COVID-19 to the Russia-Ukraine war, and they may once again emerge as winners. While the current energy crisis will still have an impact, China’s export sector benefits from the country’s uniquely insulated electricity supply system. China generates electricity primarily from domestically mined coal with abundant reserves, uses minimal natural gas or oil and has rapidly expanded wind, solar and nuclear capacity. Its regulated, non-discriminatory power system ensures stable manufacturing supply.

Meanwhile, China's manufacturing rivals face crippling vulnerabilities: heavy reliance on natural gas for power generation, dependence on expensive LNG imports and exposure to volatile Gulf energy supplies. As competitors struggle with energy shortages and soaring costs, China's structural advantages may allow it to capture opportunities.

In our 2026 annual outlook, we forecasted a moderation of China's export growth to 4.0% in 2026 from 5.5% in 2025. The global energy crisis now presents upside risks, especially if disruptions persist through the second half of the year.

China's power supply advantages could drive gains, but collapsing global demand may partially offset these benefits. If the crisis extends long enough, demand destruction could ultimately overwhelm China's comparative edge, resulting in a downturn in export growth.

To read our full report, click here.

Chief China Economist

Asia Economist

China Economist

China Economist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Central Banks | 4 min read April 2026

Economics | 2 min read April 2026

Economics | 2 min read April 2026