After more than seven weeks of an energy chokehold, the US and Iran have agreed to a two-week ceasefire. Whether this truce is temporary or ultimately proves longer-lasting is still unclear, but the ripple effects are already evident. Shortages of shipping containers and byproducts and the impact on downstream industries mean a full normalization of supply chains will take at least another two months.

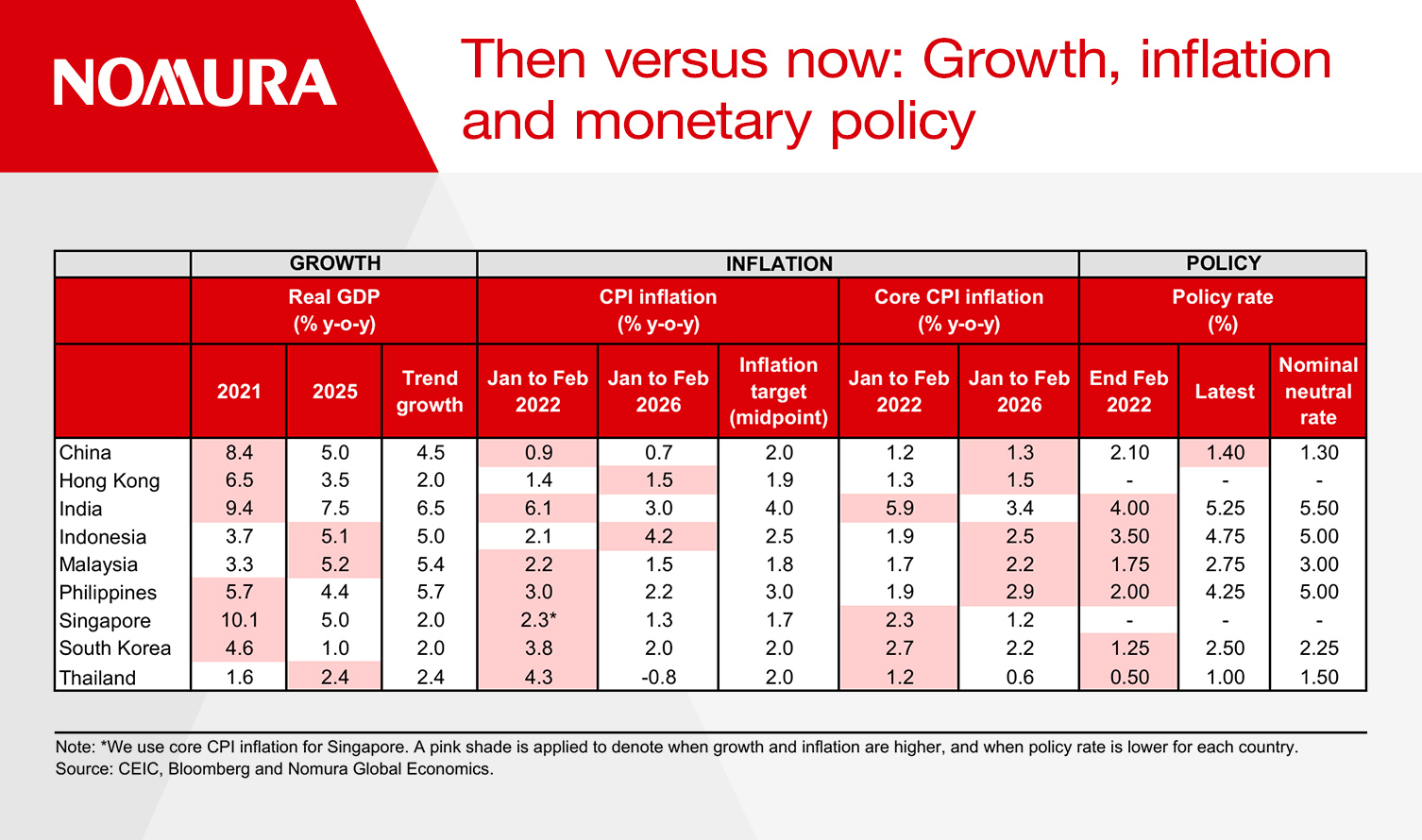

Starting point: now versus 2022

Many are comparing the ramifications of the Iran war with those of the Russia-Ukraine conflict in 2022 – there are two key differences we should note.

First, the nature of the current shock is different. Many Asian economies today are facing not only a price shock (similar to 2022), but also a volume shock similar to the COVID period. With the disruption centered around oil, which has significant spillovers across all downstream industries, this could translate into a material shock, resulting in higher inflation and lower growth.

Second, in 2022, economic conditions were considerably stronger, characterized by pent-up demand, positive output gaps, above-target inflation, elevated core inflation and below-neutral policy rates. In contrast, most Asian economies now have negative output gaps, below-target inflation, low core inflation and policy rates closer to neutral levels.

Lower buffers in emerging Asia

The economic impact of the Iran war on each country depends on whether they are protected by three important buffers: 1) fiscal buffers to protect consumers and businesses, through tax cuts or subsidies; 2) energy buffers to draw down inventories and sustain activity until supply chains normalize; and 3) FX reserve buffers

to manage balance of payments and currency pressures.

Across Asia, emerging economies have weaker buffers than their developed peers, particularly Thailand, Indonesia, the Philippines and India. These vulnerabilities reflect fiscal constraints, lower petroleum reserves and – in Indonesia's case – lower FX reserve cover. This makes them more susceptible to the stagflationary shock if the ceasefire fails and energy disruptions persist.

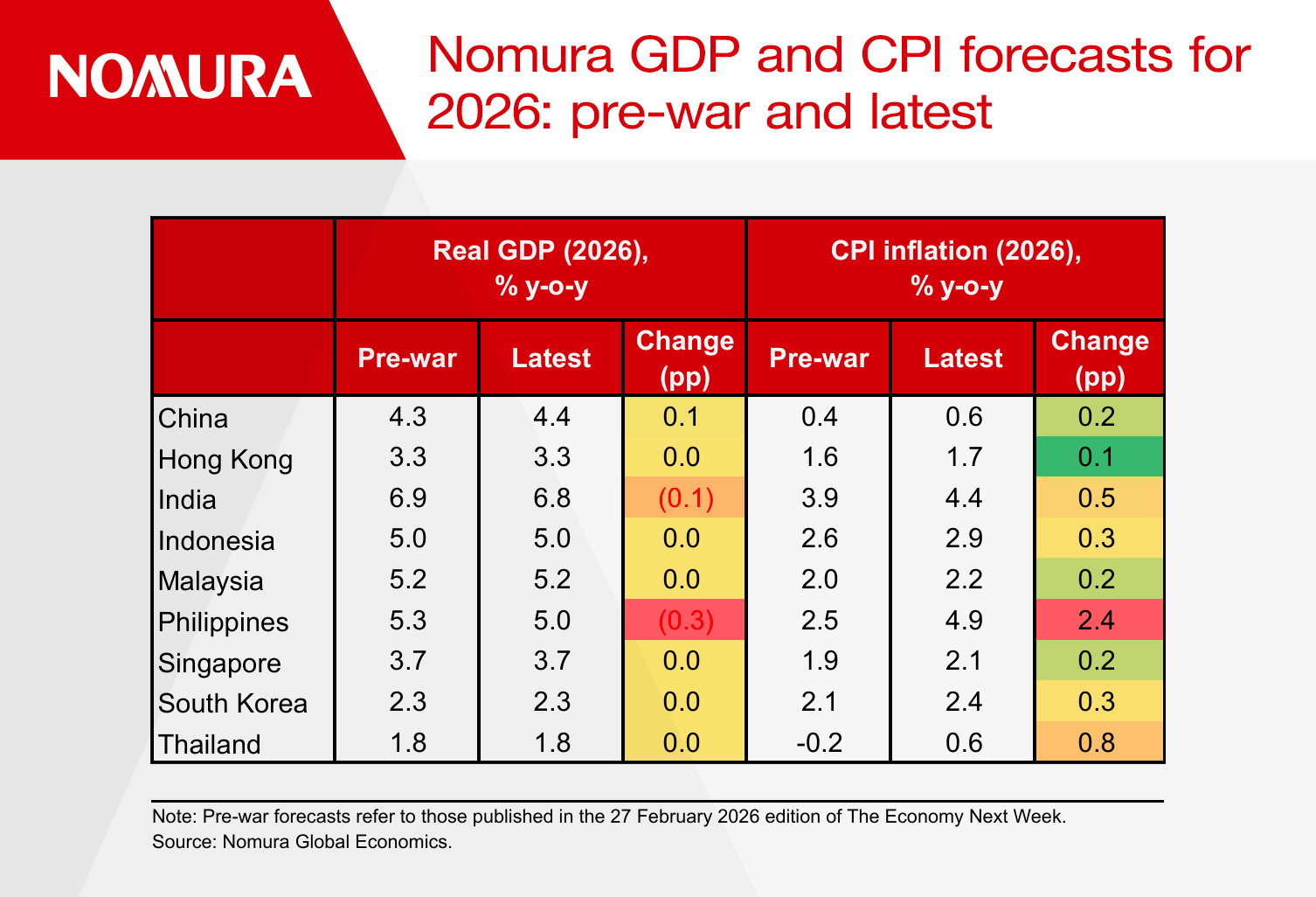

Assessing the damage to growth

The energy shock could hurt Asia’s growth through multiple channels. Direct price pressures are evident with higher costs for fuel (oil, LNG and LPG), industrial raw materials, freight and transportation. Physical supply shortages of critical inputs such as sulfur and helium have triggered rationing and forced industries to reduce output. Rising costs are squeezing corporate margins and may curtail business investment. When these costs are passed through to consumers, demand could weaken as real disposable incomes decline. Tighter financial conditions, heightened uncertainty and weakening confidence could amplify these effects. Weaker Middle Eastern demand, reduced tourism flows and lower remittance income could also dampen growth.

The growth impact is not uniform across economies. We expect emerging Asia to face greater headwinds than developed Asia. Thailand and the Philippines are particularly vulnerable to the negative terms-of-trade shock. Thailand will likely face disruptions to tourism flows, while the Philippines confronts a dual shock from lower remittance flows and reduced government spending capacity. India is grappling with supply-side rationing and an acute margin squeeze within the manufacturing sector.

In contrast, we expect strong AI-led demand and adequate buffers (fiscal and energy) in Korea and Singapore to cushion the energy shock, while Malaysia’s position as a net energy exporter provides a natural hedge. China should also be more insulated, given its self-sufficiency in coal and lower dependence on natural gas and oil to power electricity.

Assessing the inflation impact

The energy shock is generating broad-based inflationary pressures across Asia through multiple channels, affecting fuel, raw materials, food, transportation, electricity and core components. However, the direct impact is being moderated to varying degrees by fiscal subsidies to protect consumers, while the spillovers to core inflation depend on the strength of domestic demand.

So far, fiscal policy intervention is quite varied across Asia. At one extreme, the Philippines and Singapore have allowed a full pass-through of higher oil prices to consumers, and on the other extreme, India, Indonesia and Malaysia have implemented complete subsidies, keeping pump prices of widely used fuels unchanged. Most other countries fall somewhere in the middle (partial pass-through).

We expect the pass-through to core inflation to be more limited across Asia. The energy shock has hit economies when the output gap is negative and domestic demand soft, which should keep underlying inflation pressures contained, especially in Thailand, China and Indonesia. Core inflation will rise in India, due to the squeeze on manufacturing margins and select services, but we expect it to average close to the central bank forecast.

Two exceptions stand out: the Philippines and Singapore. Philippine core inflation is expected to surge, driven by energy pass-through effects on restaurants, recreation, personal care and other energy-sensitive categories. In Singapore, core inflation should also rise as the energy price increase flows through to utilities, while higher fertilizer and shipping costs raise food prices, amplified by second-round effects from the positive output gap.

Policy responses

We see the highest probability of policy tightening in Australia, New Zealand, Singapore, Malaysia and the Philippines, and the least in China and Thailand, due to persistently weak domestic demand and controlled headline inflation, respectively.

Whether the energy shock leads to more inflation or lower growth varies widely across Asia, but markets appear to have focused less on “stag” (growth) and more on “flation” (inflation) across most Asian economies. The divergence across Asia is important and presents greater opportunities for differentiation.

To read our full report, click here.