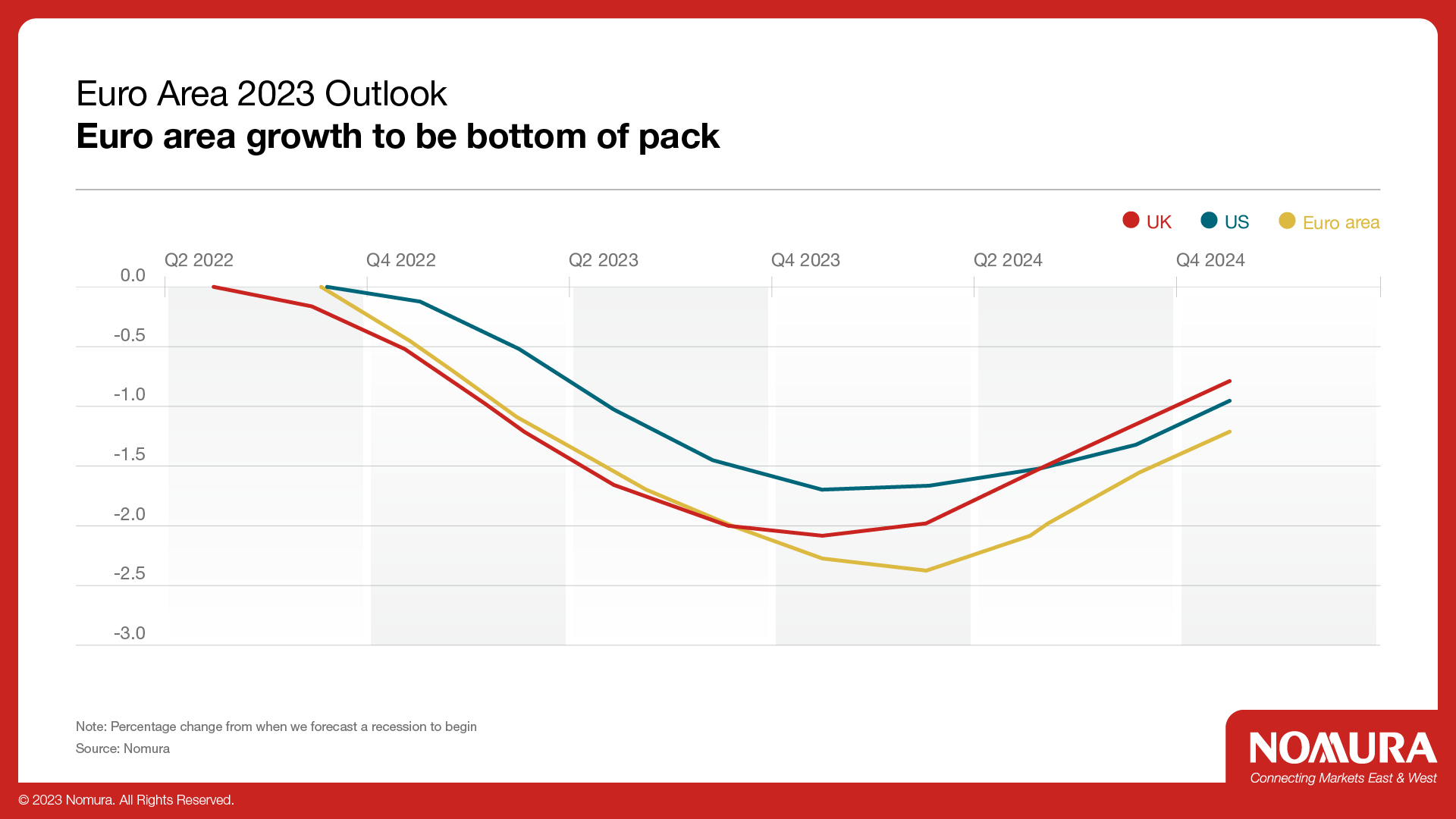

A Year of Discontent – Will it Continue?

2022 has been dominated by the Russia-Ukraine war and the impact this has had on energy prices in Europe. So far growth has been robust despite soaring energy prices. However, we expect this situation to turn around in 2023 as high energy bills begin to drain consumers’ disposable income and dent business profits, leading to a consumer-led recession.

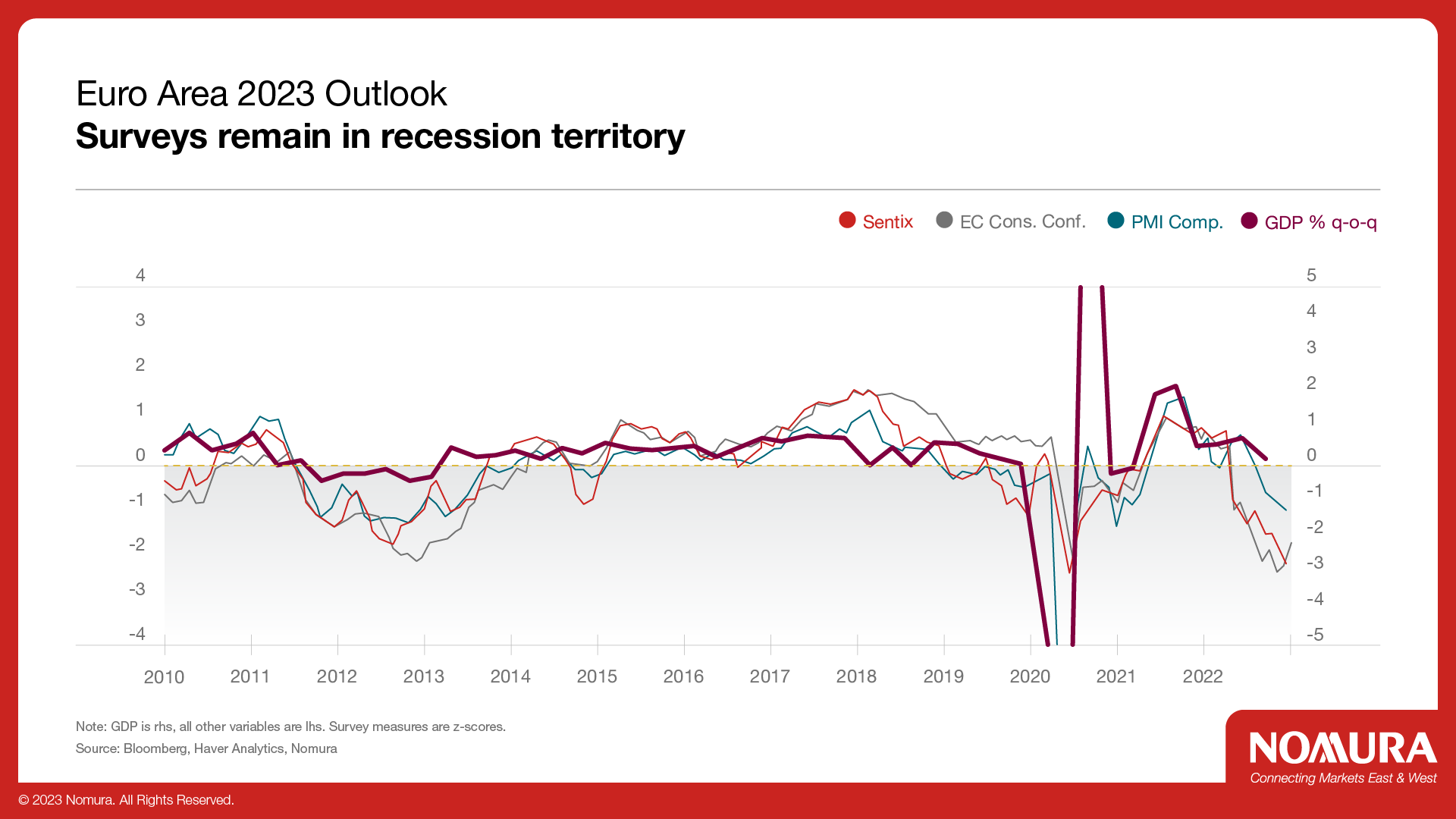

As a result of past increases in input costs and the cost of living crisis, there has been a sharp rise in the number of firms in the euro area declaring bankruptcy. Combined with the rise in business uncertainty, this might lead to firms delaying making investment decisions.

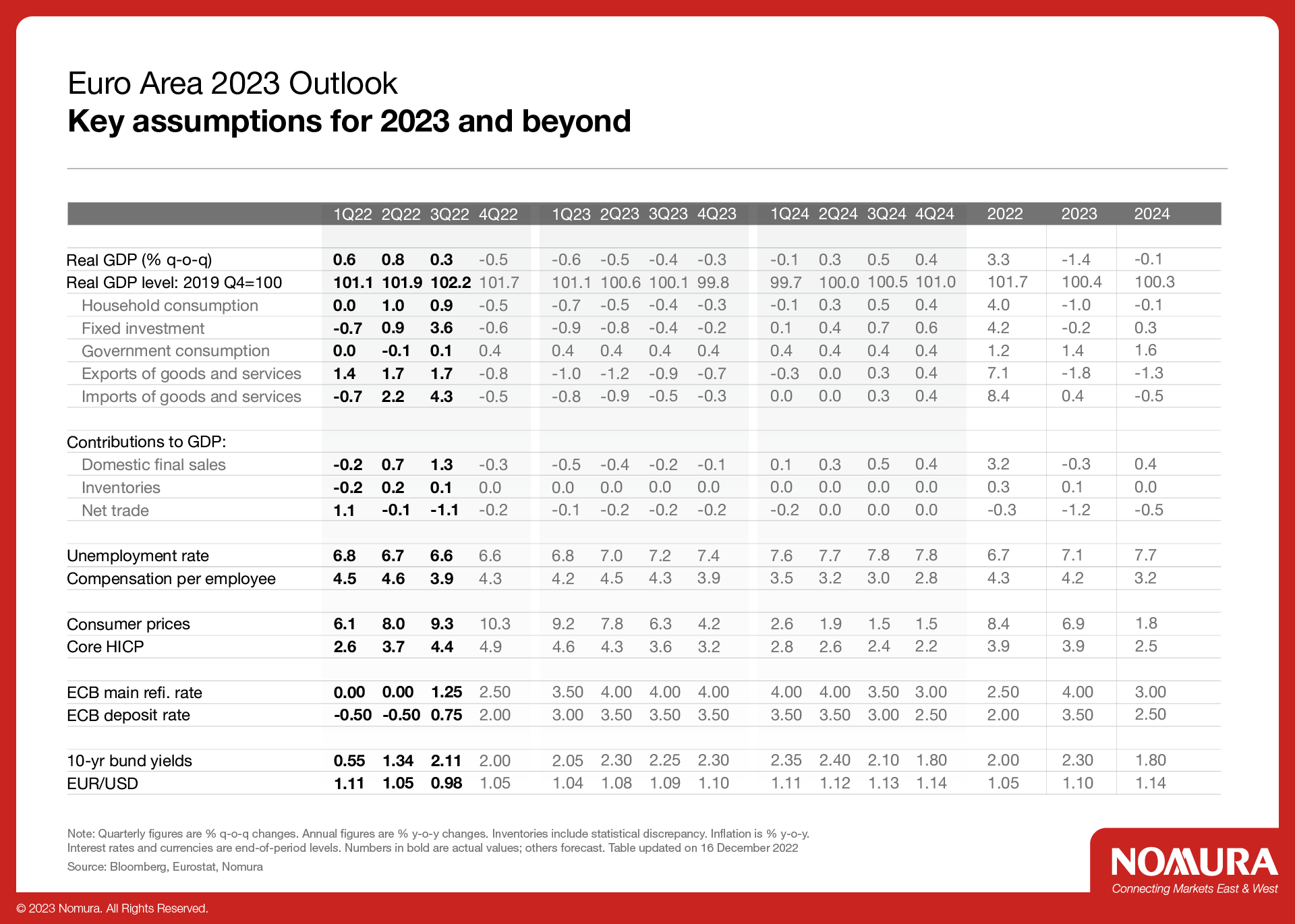

We expect weaker domestic demand and a general global downturn to hit trade hard. Our FX team thinks the euro will strengthen against the dollar to 1.10 by the end of 2023 which should add further to headwinds for exports. We are forecasting both imports and exports to continue to fall until Q2 2024. An upside risk to this scenario is the opening up of China following its zero-tolerance Covid strategy.

Ukraine-Russia War Continues Pressure on Gas Supplies

It is possible that in 2023 the war will reach a stalemate, and Europe could face a situation where gas supplies are permanently reduced.

In 2022, Europe was rescued from severe shortages by a surge in LNG imports from the US, however these flows may not be sustainable in 2023 as demand from the rest of the world increases. As China eases COVID restrictions (which itself will be a positive for the world – and European – economy) it will be in direct competition with Europe for US gas. If there are problems with gas supplies, we might expect materially weaker economic conditions in H2 2023.

However, fiscal support to deal with the energy crisis has been large, as has been the joint Next Generation EU package – both of which should help limit the scale of the recession, as could a more positive economic outcome in China. While a 2011-12-style debt crisis is not our central view, the combination of high government debt and a looming recession may yet strain the fabric of the euro system as a whole.

Inflation – The Year That Was

Euro area headline HICP inflation doubled from around 5% y-o-y in January 2022 to over 10% in October and November. In January 2023, all of the euro area’s ‘big four’ countries are planning big changes to their energy prices, which will make inflation calculations even more complicated.

There are a number of reasons inflation could fall sharply in 2023: 1) wholesale energy prices have fallen sharply, 2) surveys are suggesting that input price pressures are starting to ease, 3) financial conditions have already tightened materially, and 4) base effects.

In our view, the peak in euro area inflation is behind us and we expect it to fall over the course of 2023 and 2024 – to just below 4% y-o-y by end-2023 and around 1.5% y-o-y by end-2024. As for core inflation, we believe it will prove far more persistent (as the recent December prints have suggested), and descend much more gradually. We forecast core HICP inflation will reach around 3% y-o-y by end-2023 and just over 2% by December 2024.

The ECB has Pivoted

While we forecast inflation to fall quickly in 2023, it is likely to exhibit some stickiness and we foresee further monetary tightening. After the ECB’s rate hike of 50bp in December 2022, we see another 50bp hike in both February and March 2023, and 25bp hikes in May and June for a peak of 3.50%.

Aside from rates, the next big question for the ECB is balance sheet reduction. The ECB’s balance sheet currently stands at approximately €7trn, or almost 60% of euro area GDP. Of this, 46% corresponds to the APP, 24% corresponds to PEPP, and finally, 30% corresponds to TLTRO balances. After allowing half of the APP to wind off the balance sheet between March and June 2023, we expect full passive easing with all subsequent redemptions being allowed to roll off.

Large-scale fiscal spending will continue to be a theme in 2023. Just as the euro area looked like it had recovered from the pandemic, it was hit by secondary energy shocks and governments mobilised borrowing once again to protect household budgets.

Rather than a one-size fits all approach to debt reduction, the European Commission will use country-specific formulas to ensure debt is dealt with sustainably. This will favour countries like Italy, but could face opposition from more fiscally prudent nations like Germany. The rules will reduce the downside risks to growth that fiscal tightening would have otherwise brought, but will push sovereign debt risk out into the future.