We see a challenging first half of 2023 for Asia as recessions in the US and Europe continue to spill over into the region.

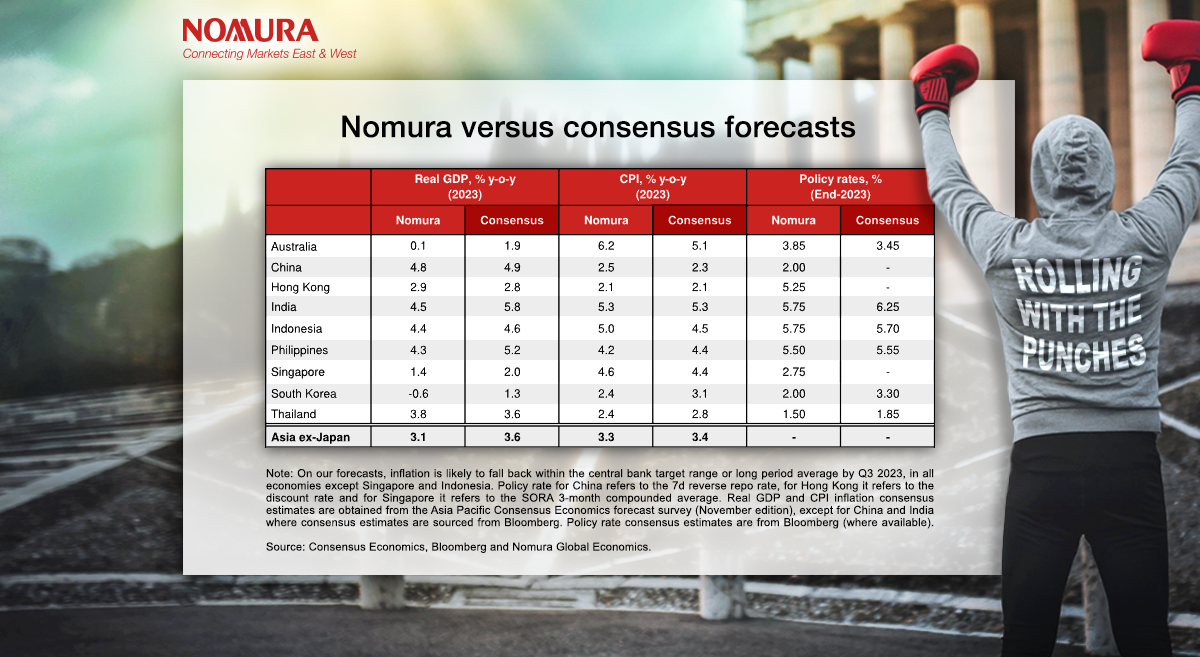

Recessions in the West will deepen Asia’s export downturn, uncertainty will lead to cuts in capital expenditure, while an inventory destocking cycle still lies ahead. All Asian economies barring Thailand look to miss consensus growth forecasts. South Korea and Australia, with housing market corrections, will likely see a growth recession – an economy that grows at such a slow pace that it results in net job losses. We expect Asia ex-Japan GDP growth (simple average) to slow to 3.1% in 2023, down from 4.0% in 2022.

The downturn in Asia’s export growth has much further to run as weakness spreads from China to the US and Europe. We forecast global semiconductor shipments to drop from -4.6% y-o-y in October to -20% y-o-y in Q2 2023 due to weak personal computer and chip equipment demand, which would lead to a double-digit decline in Asian exports.

As inventories remain elevated across semiconductor, chemicals, basic metals and electrical equipment sectors, inventory destocking will also be a significant drag on GDP growth until mid-2023. Tight financial conditions, weak demand and uncertainty will delay capex plans.

Amid weak growth, fiscal consolidation plans will likely be derailed due to weaker tax revenues and counter-cyclical fiscal spending.

But once the global dust settles, we expect Asia to attract large capital inflows, thanks to its good growth prospects and stronger fundamentals. China’s recovery, which will come from a faster reopening and Beijing’s pivot on property financing, may prop up the outlook for North Asian economies such as Hong Kong and South Korea that are more closely intertwined with China.

India, Indonesia, and the Philippines will be the medium-term champions. These three economies are likely to benefit from supply chains diversifying away from China as well as digitalization that could result in more productivity. The post-pandemic growth potential of these economies with younger populations is expected to be over 5%, the only three in the region exhibiting that potential.

Asia’s 2024 GDP growth rebound, projected at 4.3%, contrasts with our tepid U-shaped recovery forecasts for the US and Europe.

We expect the pace of inflation to continue slowing from Q2 2023, and to fall back to within the central bank target range or long-period average by Q3 2023 in all Asian economies except Singapore and Indonesia. This should give room for central banks in Asia to pause rate hikes and subsequently cut policy rates in the second half of 2023 and into 2024. The extent of policy easing will be less than in the US as policy rates in Asia are closer to neutral.

On Asian FX, we are taking a more cautious approach into the new year. The US dollar is unlikely to be as strong as its October 2022 levels within the coming year. Even so, FX volatility is still susceptible to various risks such as Fed policy, other global central banks raising rates, economic or Covid-related uncertainties in China, and balance of payments-related vulnerabilities in parts of Asia. Expect stronger Asian currencies starting in Q2 2023, which will also help to counter inflation.

For more on our macroeconomic outlook as we head into 2023, read our full report.

Ting Lu, Euben Paracuelles, Andrew Ticehurst, Jeong Woo Park, Craig Chan, Wee Choon Teo, Albert Leung, and Nathan Sribalasundaram also contributed to this report.