Volatility | 0 min video February 2019

Volatility | 1 min read | February 2019

Volatility | 1 min read | February 2019

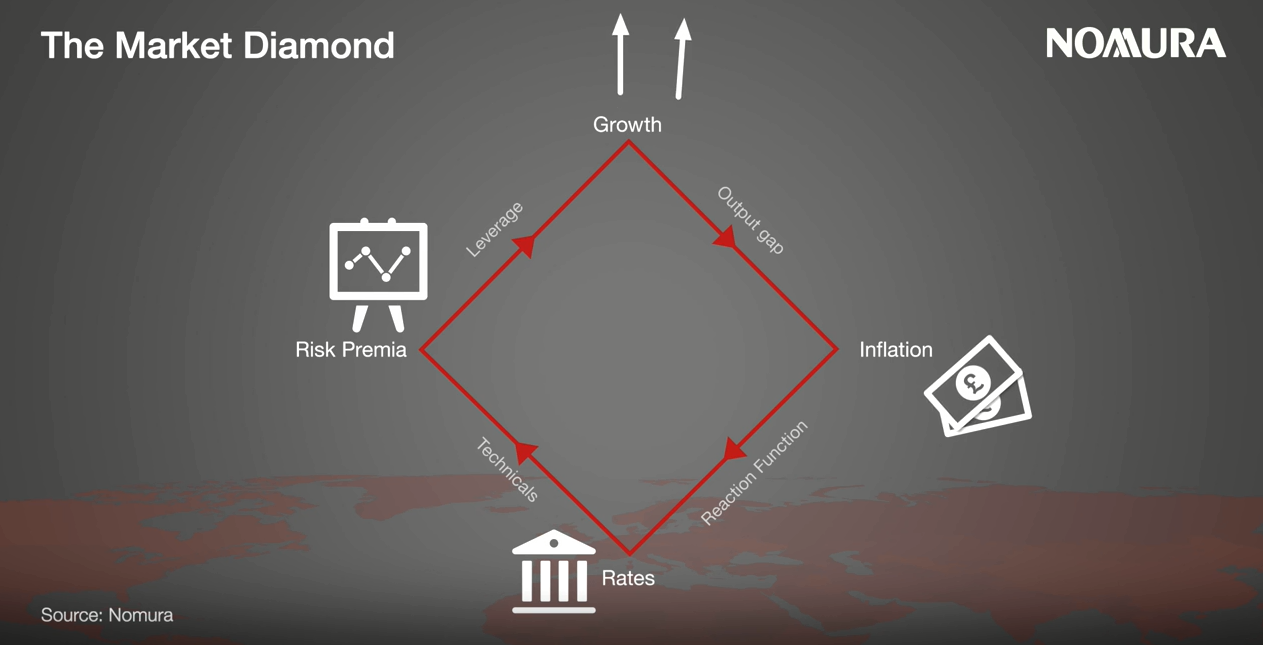

In asset allocation we use a market diamond approach to predict future economic expansion, connecting growth expectations which drive inflation, central bank policy, and market risk premia. There are feedback loops between all four of the quadrants of the diamond.

“We’ve just come out of the longest expansion in post war history, and the question for investors is timing and when it will come to an end”

When the output gap or the amount of spare capacity in the system has been used up, there is a risk that we’re going to move into a slowdown. Markets are likely going to continue to be correct, by pricing in that slowdown.

The market has recently shifted regimes, from where growth was running above trend across G4 economies and developed markets, to where growth is heading sub trend. We predict that by the second half of 2019 markets will have adjusted to the second round effects, meaning that:

The kind of problems and structural issues that are at root here are significant, and very hard to solve. We predict that issues are going to continue but the question is how deep and how hard?

For more information read Return Regime: We weren’t bearish enough

Head of International Research

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Volatility | 0 min video February 2019

Volatility | 1 min read February 2019