Hong Kong’s use of blockchain in the green bonds sector highlights how the technology can be rolled out to reduce greenwashing while attracting a greater pool of investors.

The Government of Hong Kong issued its tokenized green bond for institutional investors in February 2023 with the support of the Hong Kong Monetary Authority (HKMA). The issue amount was HKD800 million, for a one-year maturity at an interest rate of 4.05%.

The bond was issued under a Green Bond Programme introduced in 2018 with the aim to: (1) clearly demonstrate government support for sustainable development and resolve to respond to climate change; (2) set a benchmark in the green bond market; (3) serve as an example for other potential green bond issuers; and (4) promote awareness of green finance and Hong Kong's international recognition of the sector.

The tokenized green bond was issued under a framework, consistent with the Green Bond Principles of the International Capital Markets Association. Eligible project areas for use are:

- renewable energy

- energy efficiency and energy conservation

- pollution prevention and control

- waste management and resource regeneration

- water resources and wastewater management

- nature conservation and biodiversity

- clean transportation

- green buildings

- climate change adaptation

According to the Green Bond Report 2023, the actual use of the tokenized green bond was 69.5% for green buildings, 30.1% for water resources and wastewater management, 0.3% for climate change adaptation, and 0.1% for pollution prevention and control.

The seeds were planted three years ago when the HKMA and the BIS Innovation Hub launched a proof-of-concept to develop a prototype digital platform to improve transparency for retail investors accessing green bonds.

HKMA and the BIS Innovation Hub worked with six partners designing the project’s digital infrastructure including Digital Assets, a global provider of blockchain solutions; Singapore-based Shareable Assets, an asset tokenizer; and Hong Kong-based Allinfra, which develops sustainability-related software.

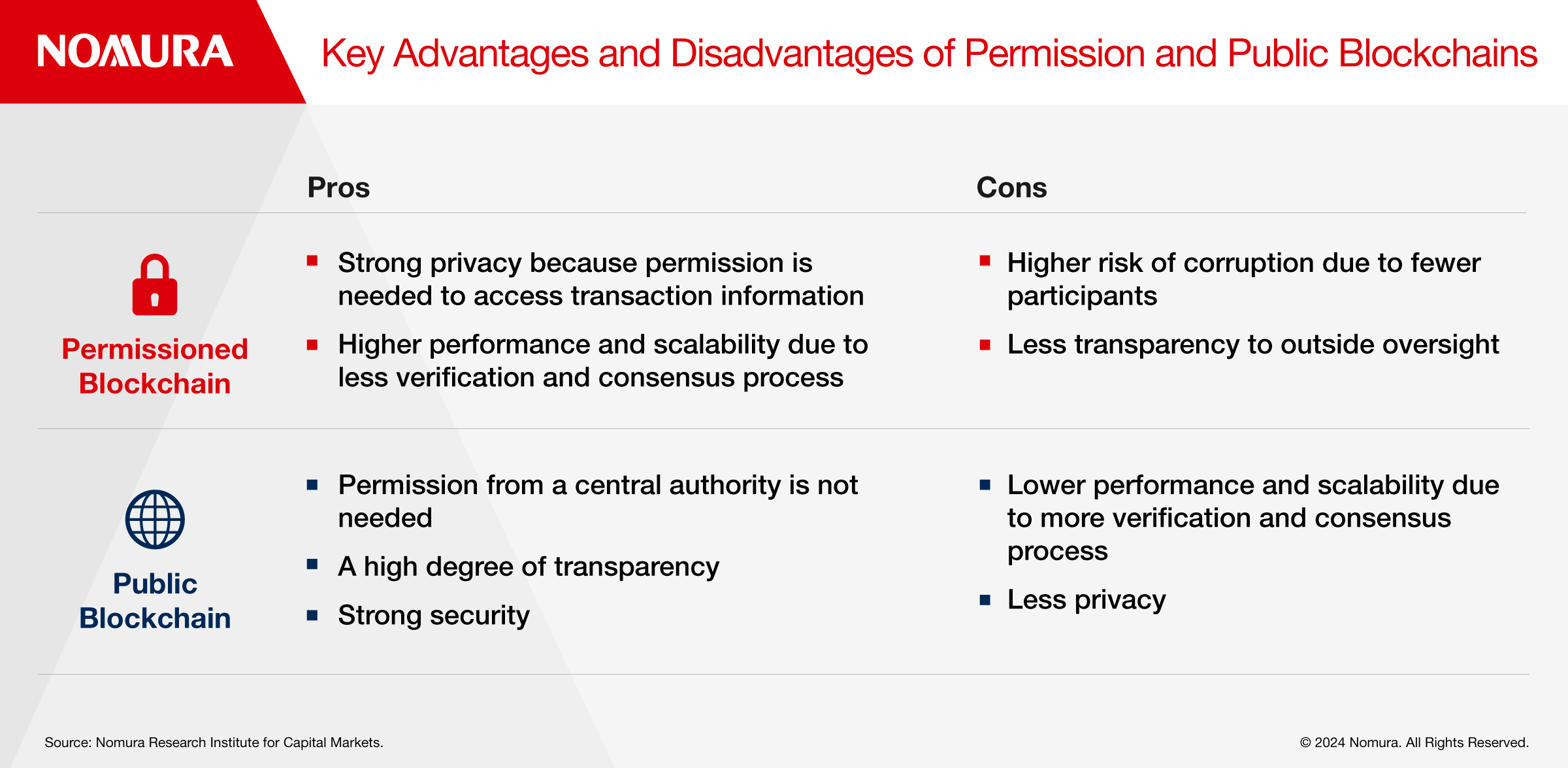

Dubbed Project Genesis, the team developed two prototypes of a digital platform: The first, developed jointly by Digital Assets and GFT Technologies, simulates a series of processes involving bond origination, offering, settlement and secondary market transactions on a permissioned blockchain platform with limited participants (Figure 1).

The second prototype simulates the same process on a public blockchain platform with no centralized administrator.

In general, bonds are traded OTC, and the privacy of transactions is important. The speed of the process is also a factor to be taken into consideration when issuing bonds.

Consequently, a permissioned blockchain is probably most suitable for tokenizing bonds and the Hong Kong government's tokenized green bond was indeed issued on a permissioned blockchain platform.

Democratizing the market

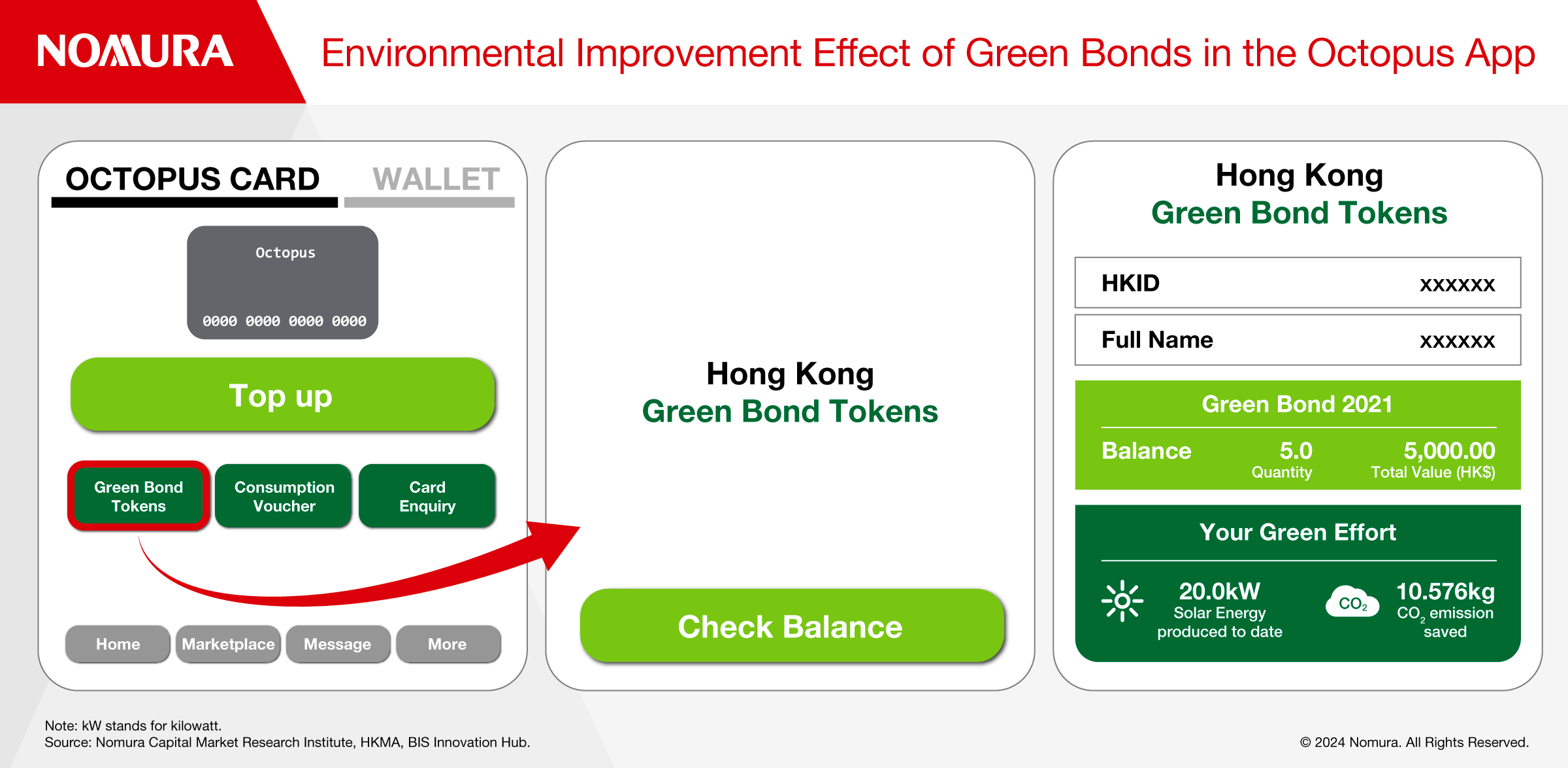

Tokenizing green bonds makes it more accessible for individual investors to invest in the asset class. For example, the Hong Kong government has issued green bonds since 2022 to encourage individual investors to participate in the green finance market but these bonds are sold through securities companies and banks, and the minimum investment is HKD10,000. In contrast, a tokenized green bond allows retail investors to buy and sell from HKD100 on a dedicated mobile app.

Second, it is easier to record the environmental improvement effect. Allinfra provided real-time tracking data on how much clean energy is being created and how much it contributes to carbon dioxide (CO2) reduction in projects funded by green bonds. To make such information more accessible, it was connected to Hong Kong’s Octopus app, the popular electronic money in Hong Kong. As a result, individual investors will be able to see the environmental impact of their green bonds in real time (Figure 2).

Use of technology for green bond-related carbon credits

Following the success of Project Genesis, the HKMA and BIS Innovation Hub addressed issues related to greenwashing and additionality of green bonds and also worked to improve the transparency, objectivity and soundness of the green bond market.

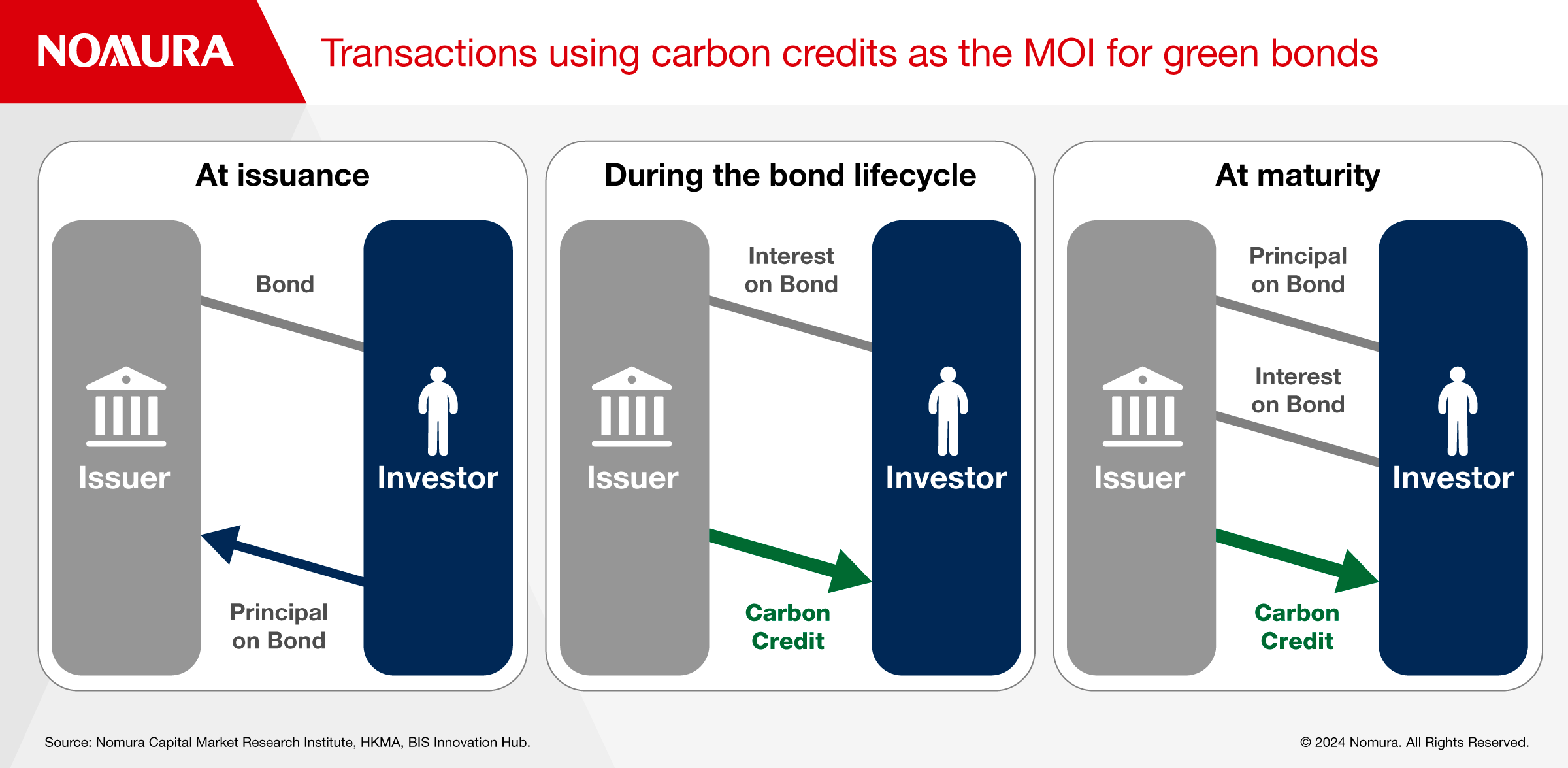

The effort, called Project Genesis 2.0, was carried out in conjunction with the UN Climate Change Global Innovation Hub. The three organizations announced in October 2022 that they had completed a feasibility study focusing on Mitigation Outcome Interests (MOIs) to quantitatively visualize the environmental improvement benefits of green bonds. An MOI is a return to investors as a result of a project for which funds are allocated, in addition to the interest rate paid to investors by green bond issuers (Figure 3).

One of the main advantages of using MOIs is the reduction of funding costs. Green bond issuers may be able to keep interest payments low by offering investors an MOI separate from interest rates. As a specific form of MOI, carbon credits were proposed.

The MOIs enable real-time tracking of the environmental impact of projects funded by green bonds while also efficiently delivering carbon credits. In addition, smart contracts can be used to automatically transfer carbon credits to investors at the time of interest payments and maturity. MOIs also prevent double counting of carbon credits which occurs when a single carbon credit is issued to multiple entities due to the absence of a common place of registration. Blockchain helps avoid double counting by clarifying exactly who owns which carbon credit.

The Hong Kong Exchanges and Clearing (HKEX) established Hong Kong’s voluntary carbon credit market in October 2022 and in future, a mechanism for green bond investors to receive carbon credits as MOIs could further expand the market.

In summary, tokenization gives investors a quantitative, real-time view of the environmental benefits of their investments, which means they can participate in green bonds without being concerned about the risks of greenwashing.

If such a mechanism is also used in green bond issuance in the private sector, it could accelerate growth of green bonds in the medium to long term.

Tokenized green bonds are also expected to generate interest from technology-savvy young people which may lead to a wider base of individual investors participating in the green bond market than ever before.

Japan has been quick to follow Hong Kong’s lead and in December, Hitachi Ltd sold Japan’s largest green digital corporate bond with a value of ¥10 billion ($70 million).