How Overseas Investors are Using Options to Play Japan Equities

Overseas investor interest in Japan’s resurgent growth story is boosting demand for equity derivatives on undervalued stocks as ongoing corporate governance reforms take the market higher.

Tomiyuki Oji

Head of Flow Equity Derivatives, Nomura, Tokyo

Nathan Watson

Multi-Strategy Sales, Nomura, Hong Kong

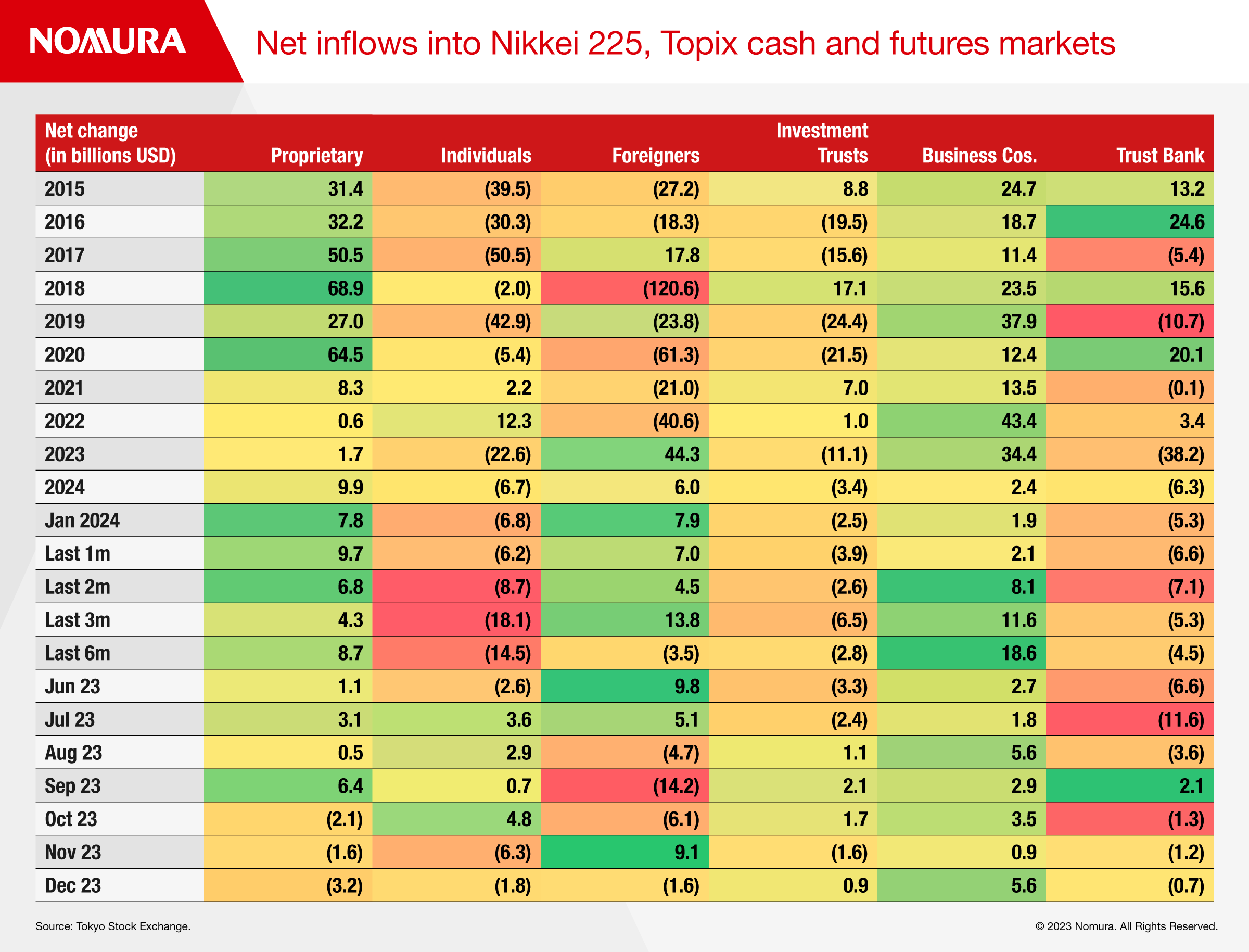

Nikkei 225, Topix buoyed by corporate governance reforms, share buybacks

Foreign investors and Corporates are biggest buyers of stocks

Client demand is for call spreads, call ratios on low p/e stocks and baskets

Overseas investor interest in Japan’s resurgent growth story is boosting demand for equity derivatives on undervalued stocks as ongoing corporate governance reforms take the market higher.

January saw foreign net inflows of $7.9bn into the Nikkei 225 and Topix futures and cash markets according to Tokyo Stock Exchange data, the second biggest month since May 2023. Last year foreign investors bought $44.3 billion of Japanese stocks, the biggest buying spree since 2013.

That momentum helped the Nikkei 225 exceed its 1989 bubble high and surpass 39,000 points on February 22.

Net inflows into Nikkei 225, Topix cash and futures markets (31 Jan 2024)

A confluence of factors including structural reforms, optimism about a break from deflation and a shift away from negative interest rates have converged over the past 12 months to burnish the appeal of Japan’s stock markets for a broad range of investors.

The current upswing reflects how investors have real conviction in the rally according to Tomiyuki Oji, Head of Flow Equity Derivatives at Nomura in Tokyo.

“The market has had a great start to the year,” he said. “Compared to two years ago, volume has picked up, local firms and offshore institutional investors are all buying Japanese equities.”

Historically, Japanese corporates have been low return on equity prompting the Tokyo Stock Exchange last year to encourage companies with price-to-book ratios (PBR) lower than 1.0 to disclose specific policies and initiatives to lift their value. A PBR below 1 is an indication that a company has not achieved profitability that exceeds its cost of capital.

While there are several ways to achieve such an outcome, a simple approach that some firms have adopted, is to boost dividends and share buybacks.

Oji says that client interest from pension funds and insurance companies has been especially high for low price-to-book companies.

“Corporates are supporting the market by buying back stock and incentivizing investors to own it,” he says. “The breath of buying has improved markedly, in part, because those companies historically are ‘cheaper’ versus the US.”

Oji adds that the widespread expectation that the Bank of Japan will soon exit its near decade-long negative interest rate policy is boosting demand for bank stocks, which stand to benefit from the change.

Japan’s banks have traded at very cheap valuations compared to their book value for many years as negative rates squeezed their net interest margins.

Cheap Valuations

Nomura's sales desk has screened for low-price-to-book companies and created custom baskets for investors to play this thematic using options structures, says Nathan Watson, Multi-Strategy Sales at Nomura in Hong Kong.

They can also trade Topix bank futures and options on exchange although larger hedge funds tend to trade index options OTC to keep their trades private.

Nomura is one of a handful of banks that offer options on Japan indexes 24/7 even in the US time zone.

Vanilla options structures such as calls, call spreads and call ratios remain the most popular especially from US hedge funds and European institutions that are keen to invest but don't want to lose more than their fixed amounts.

A call spread involves buying low strike calls while selling higher strikes. The payout is limited but the upfront premium is lower.

“What's going on in Japan now is implied volatility levels are above average and as there is an unending bid for the market to go up, call options are expensive,” says Watson.

Call ratios entail buying one low strike calls while selling two higher strikes to further cheapen the call spread.

“The call skew is very flat so what you can sell further out of the money is actually worth a lot more than it used to be,” he says.

Volatility skew is trading in the 90% region, which is extreme while Nikkei implied volatility is above 50%.

Watson adds that institutional money favours options over cash positions because they are lower maintenance.

“If I own a cash position and something happens in Japan and the index is down 5% in a day you have to do something but with a call spread the risk is minimized,” he says.

Corporate Governance Baskets

Watson notes that the drive to unwind cross-shareholdings in Japan is set to unlock deep value in leading Japanese companies this year and is fast becoming the most active thematic for clients.

“The regulatory pressure to bring book value above one, is prompting companies to sell down and unlock the worth of the cross-shareholding stakes that they own, which are often trading at a deep discount,” he says.

He adds that clients are playing the theme via bullish trades on Delta One baskets of companies that are engaging in unwinding their stakes. This is typically a basket of stocks that is given a single ticker and trades similar to an ETF but can be packaged as a total return swap. It can also be structured as options on the basket.

A different way to invest in the same idea is via a basket that goes long companies with very good corporate governance and shorts companies with poor corporate governance – pitting those who are implementing change against the laggards to maximise both sides of the theme.

Call Overwriting

Another popular strategy is covered call overwriting, which involves selling a call option on a stock or index that an investor owns. When selling out-of-the-money call options, the seller retains the potential capital growth up to a certain level, but any growth above that level is sold in exchange for an upfront payment.

In this way, demand is coming from both offshore and onshore clients to hedge their long cash portfolio which they have been building over the past 18 months and can use higher than average volatility to sell calls against their position and earn some income.

“As a franchise we see a lot of domestic hedging in Japan because pensions and life insurers in particular, are naturally long and have a hedging program while long-term offshore investors are trying to invest in Japan and need to protect their book,” says Oji.

Domestic life insurers are predominantly using vanilla options or small exotic structures such as a Nikkei put contingent on FX or similar to make the premium cheaper.

More sustainable than Abenomics

Watson says the current upswing feels very different to the Abenomics era of 2012 when the late Shinzo Abe used monetary easing, government spending and structural reforms to breathe life into corporate Japan.

“It was much more tactical; clients would come in to play Japan and there was a risk of losing much of their gains because the trend unravelled so quickly.”

Oji believes the current wave is more of an “asset allocation story” making it more robust than Abenomics as it is anchored to rising inflation and therefore growth, with corporate carrying out reforms and buying back shares, adding structural momentum to the rally.

“Trading volume in the stock exchange is bigger than 10 years ago. The market is more mature with various types of flows, and we are expecting more to come,” he says.

NISA Tailwind

The missing piece in the Japan equities story is retail participation but even that may be about to change.

Japan’s small investment tax exemption programme, known as NISA (Nippon Individual Saving Account), was overhauled in January to incentivise retail participation in stocks over saving. It now gives tax breaks to individuals on annual investments up to JPY 3.6 million per year up from JPY 1.2 million.

“This is the ultimate bull case for Japan equities – retail customers have huge savings which they're now being encouraged to start deploying into other assets and cash will no longer be king in Japan as they come out of deflation,” says Watson.

Oji says that three catalysts are required for the Nikkei 225 rally to continue: 1. consistent EPS growth in cyclical sectors; 2. A positive inflation cycle with price hikes; 3. Global asset managers rebalancing their portfolios from underweight or neutral to overweight.

“It's bubbling and after 30 years of deflation I am optimistic,” he says. “The inflation story is just starting in Japan and when you compare how prices have tripled in 30 years in the US, Japan has a lot more room to grow.”

This material is not a product of Nomura Research and is provided only to professional investors under Article 2 (31) of the FIEA. This material is for informational purposes only and is not intended to be used as an offer to sell or a solicitation to buy any of the financial instruments or strategies described herein. It is prohibited to copy any part of this document without written permission from Nomura Securities, and does not represent that any profit will be achieved. Past performance is not necessarily indicative of future results. The views expressed in this document are subject to change without notice. The products and strategies described herein may not be marketable in some states or countries or may not be suitable for all investors. Nomura Securities does not guarantee the accuracy, completeness, reliability, fitness for a particular purpose or merchantability of the information contained in this document. Nomura Securities assumes no responsibility for the use, misuse or distribution of the information contained in this document to unauthorized recipients

Nomura Securities Co., Ltd. Financial Instruments Business Operator: Director-General of the Kanto Local Finance Bureau (金商) No. 142

Affiliated Association/Japan Securities Dealers Association, Japan Investment Advisers Association, Financial Futures Trading Association, Type II Financial Instruments Business Association