Economics | 3 min read March 2018

Economics | 2 min read | March 2019

Economics | 2 min read | March 2019

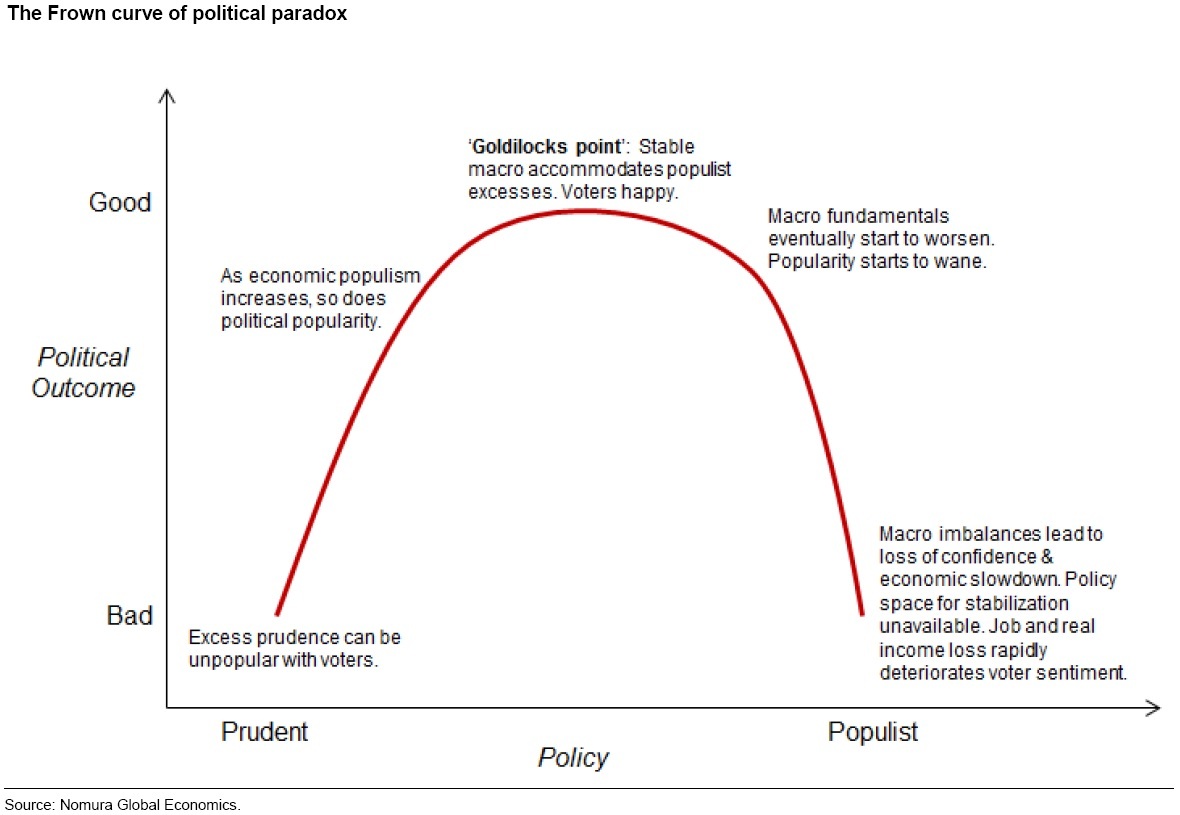

Is good economics also good politics? It could be argued that the experience of the past two decades suggests an inverted-U (a frown) relationship between the degree of populism and the electoral success. Too much populism as well as too much prudence have both resulted in an electoral defeat.

With general elections scheduled for April and signs of the tide turning against the ruling Bharatiya Jananta Party (BJP), the drumroll of populist policies has intensified over the past six months. In the short run, strong macro fundamentalists can accommodate populist excesses but, over the medium term, they risk creating imbalances, with implicit prioritization of consumption over investment. In this report, we take stock of the extent of macro policy easing that has incrementally built up in the run-up to the general elections and present our framework to assess its economic impact.

The political-economic frown cycle

The macro environment today seems similar to the one in 2004, when BJP’s “India Shining” campaign backfired. Banks had large non-performing assets during 1999-2004, as now. This also applies to low food inflation and low rural income growth. Thus, it could be argued that too much prudence does not always mean good politics. Consequently, the broader direction of macro policy has passed a turning point and is now moving away from too much prudence.

At a national level, the last two decades have suggested a U-frown relationship between the degree of populism and electoral success. Too much as well as too little of the former has resulted in an electoral defeat. The trick is finding the right balance. Policies around rural India have played a big role in deciding electoral outcome, as rural India accounts for almost 70% of the total population.

Short-term risks to look out for

The effectiveness of recent policy easing could be partially lost due to transmission lags and implementation hurdles. The impact of the Reserve Bank of India’s rate cut will be delayed and uneven. Banks that have the capacity to lend are already garnering market share from shadow banks (after last year’s crisis), which has elevated credit-deposit ratio and delayed a reduction in lending rates. Additionally, some sectors such as low-tier shadow banks are credit constrained because of the perception of higher ‘credit risk’ and therefore may not benefit as much from the rate cuts.

Medium-term risks to monitor

Even as near-term growth-inflation dynamics will likely stay benign, medium-term macro dynamics are changing at the margin. The ongoing rural distress implies that, irrespective of the political party in power, the political-economic cycle will dictate that rural reflationary policies remain the key priority.

Rural reflationary policies matter for inflation dynamics. These policies may face near-term implementation challenges, but as they are successfully executed over time, they will likely lift rural demand and food inflation.

To know more about accommodative macro policies in India, read here.

Chief Economist, India and Asia ex-Japan

India Economist

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.

Economics | 3 min read March 2018

Central Banks | 1 min video December 2018

Economics | 3 min read September 2017