Following the US and Israel joint military operation targeting Iranian military infrastructure, leadership sites and nuclear-linked facilities, Iran launched missiles and drones at Israel and US bases in multiple Gulf states, causing an oil price shock impacting oil importing nations.

Here we discuss the economic impact, policy response, winners and losers, as well as the equities and FX implications for Asia.

Oil prices have been drifting higher since mid-January, building in a higher geopolitical risk premium and supply disruption. Oil fundamentals appear weak over the medium term, but temporary supply-side shocks can trigger even higher oil prices, depending on the duration of the conflict. A curtailment of Iran’s oil exports, damage to Gulf energy infrastructure and vessel traffic shortage or prolonged disruption in the Strait of Hormuz can lead to a significant energy shock for Asia.

Economic impact

Higher import bill is the most potent channel

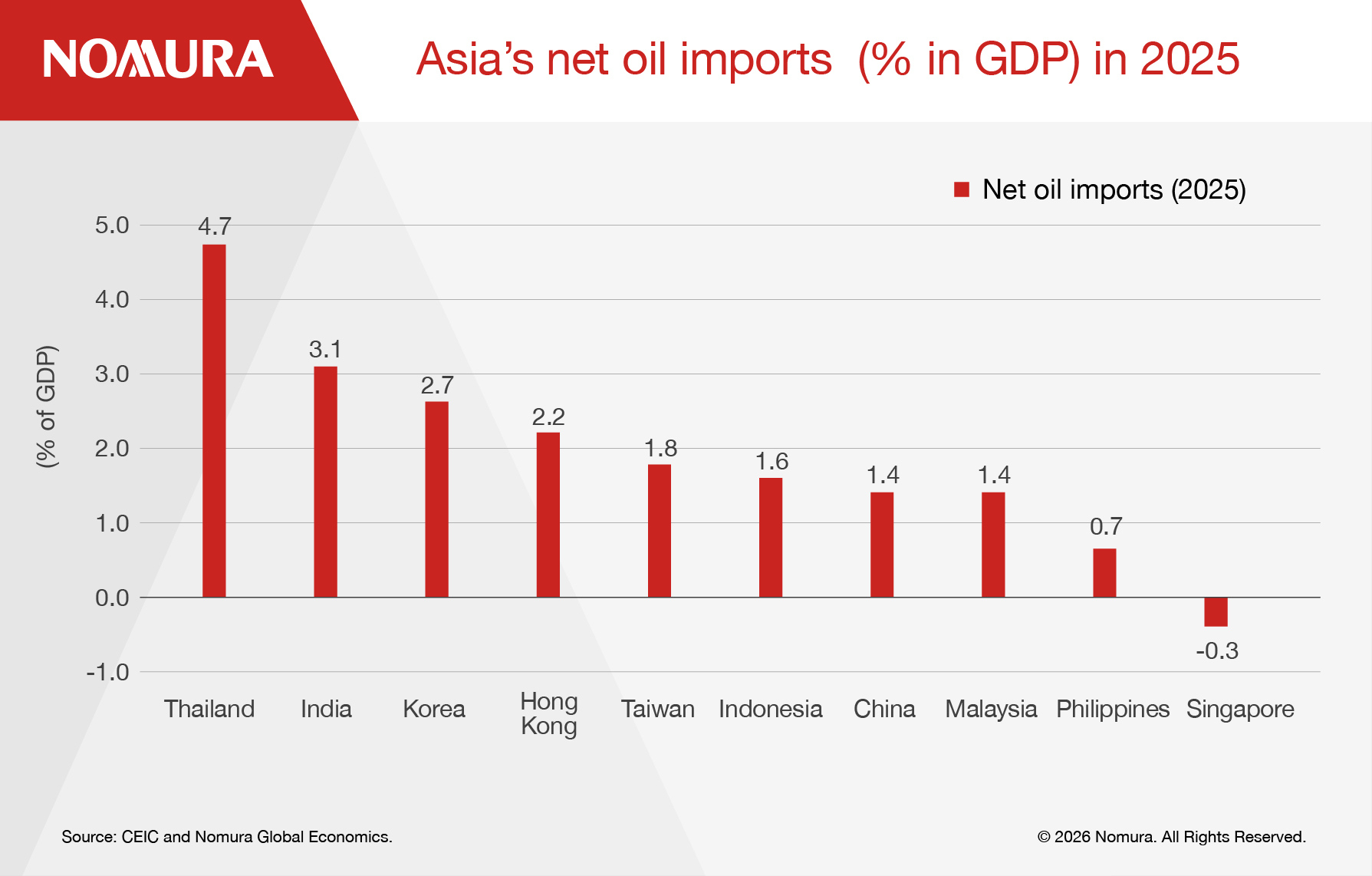

Higher oil prices will significantly impact Asia's import bill and current account balances due to the region's heavy dependence on oil imports. On average, every 10% rise in the price of oil worsens Asia's current account (CA) balance by ~0.3% of GDP. The top three most vulnerable economies include Thailand (net oil imports are the highest at 4.7% of GDP, and every 10% oil price change worsens its CA by 0.5pp), India (3.1%; 0.4pp) and South Korea (2.7%; 0.3pp). The Philippines also runs a current account deficit, which is likely to be back on a widening path. Two other factors can amplify the impact of oil prices on Asia: first, a weaker currency due to risk aversion can further increase the oil import bill; and second, many governments provide subsidies to shield consumers from price increases, so higher global oil prices do not always lead to a proportional demand reduction.

Inflation pass-through should be limited

The impact of higher oil prices on Asian inflation is not straightforward. While energy accounts for 3-14% of the CPI basket, and every 10% oil price change, on average, adds 0.2pp to headline CPI inflation, the actual pass-through differs significantly across economies, due to government intervention. EM Asia economies that are most sensitive to the inflationary impact of higher oil prices (India and Thailand) also use price controls and subsidies that limit immediate inflation, with costs absorbed by fiscal authorities or state oil companies. Moreover, the current low inflation starting point provides a cushion. We estimate higher inflation pass-through for countries like the Philippines (0.5pp for every 10% oil price rise) and Korea (0.3pp), which have market-determined fuel prices. We would expect inflationary risks to become a larger threat, if the rise in oil price sustains and spills more broadly into food and other commodities, due to an increase in transportation/freight costs and higher fertilizer prices.

Fiscal burden will rise

Higher oil prices create both direct and indirect fiscal pressures across Asia, as governments typically use fiscal policy as a wedge – through subsidies, tax cuts or excise duty reductions – to shield consumers from energy price increases. Within Asia, India, Indonesia and Thailand could face an incremental fiscal burden, due to higher oil prices. In India, the marketing margins of oil marketing companies would come under pressure, and they may require government support, if higher oil prices sustain. In Indonesia, a 10% oil price rise could worsen the fiscal balance by 0.2pp via higher subsidy spending, and raise the risk that the 3% ceiling could be breached.

Country winners and losers within Asia

In Asia, Thailand, India, Korea and the Philippines are the most vulnerable to higher oil prices, due to their high import dependence, while we see Malaysia as a relative beneficiary.

In Thailand, current account and inflation pressures should rise, but we are less worried about inflation, amid ongoing deflation and the below-potential growth outlook. In India, we expect a higher import bill and risk-aversion driven portfolio outflows to increase balance-of-payment funding pressure in the near term. In Korea, we believe higher oil prices and resident portfolio outflows are likely to partly offset the gains from the AI boom, sustaining KRW depreciation pressures. We also see a risk of a much wider current account deficit in the Philippines, due to its high oil import dependence, and some inflation risk from an immediate pass through to consumers, due to the absence of subsidies.

In contrast, Malaysia could emerge as winner due to its status as a net energy exporter. While Malaysia is a small net crude oil importer, it is a small net exporter of LNG, so we believe the impact of rising crude oil prices on the CA balance has also turned positive.

Monetary policy in wait-and-see mode

On monetary policy, central banks are likely in wait-and-see mode for now, given elevated uncertainty on the duration of any oil price shock, and offsetting effects on growth (lower) and inflation (higher). The ongoing Iran conflict solidifies the case for many central banks to hold rates steady for now. We do not see higher oil prices as a trigger for rate hikes, unless the oil price increase sustains and there are signs that this is broadening into other commodity/food prices and seeping into higher core inflation.

Asia equity strategy

Historically, beyond initial short-term reaction, markets have tended to look through geopolitical tensions. In the most recent episode, during the ‘twelve-day war’ between Iran and Israel in June 2025, US stocks were largely unscathed even when oil prices spiked by ~USD10bbl when Israel attacked Iran’s nuclear facilities.

Any sustained rise in oil prices due to supply disruption will be clearly negative for Asian equities, which are mostly net-energy importer countries. Most vulnerable equities in the region are likely to be India, Indonesia and the Philippines – all twin deficit countries.

However, if the conflict ends relatively quickly, alongside the fall of the Iranian regime, which also results in structurally lower oil prices over time (due to improved perceptions of Middle-East “stability”), it is quite conceivable that this would prove to be positive for equities.