We expect US tariff policy to continue its current de-escalatory trajectory, despite the possibility of episodic flare-ups

We expect US trade/tariff policy to continue its current de-escalatory trajectory, despite the possibility of episodic flare-ups

Wider exemptions, lower tariff rates, and greater focus on affordability suggest limited further escalation in US tariff policy despite uncertainty from the latest Supreme Court ruling

Our new expectation for the terminal effective tariff rate suggests tariff-induced price pressures will start to diminish in the coming quarters, while higher commodity prices might exert an offsetting force

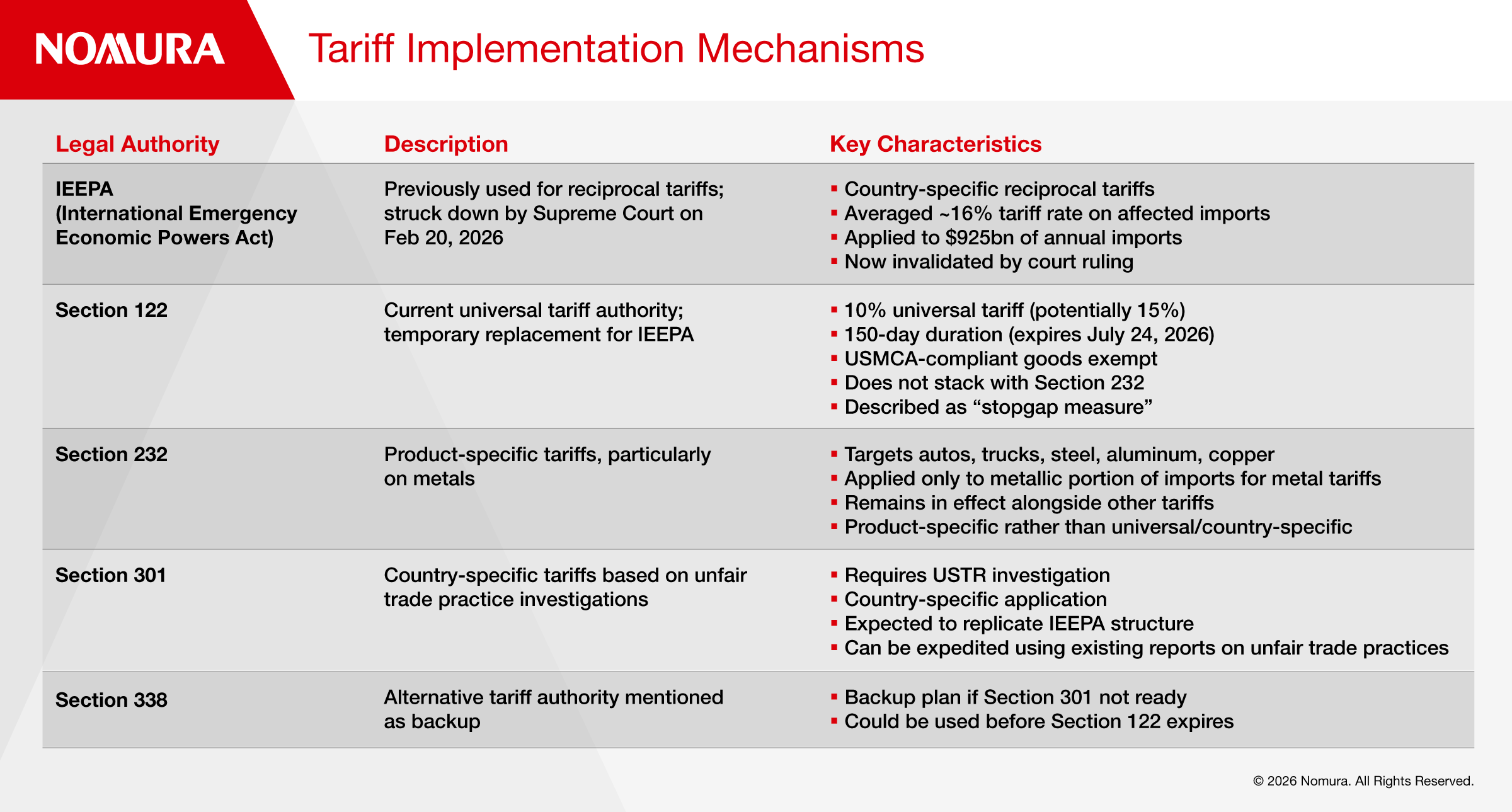

We expect US trade/tariff policy to continue its current de-escalatory trajectory, despite the possibility of episodic flare-ups. The Trump administration has signaled an intent to preserve continuity in the trade framework following the Supreme Court ruling striking down IEEPA (International Emergency Economic Powers Act) tariffs and imposed only a 10% tariff under Section 122, potentially rising to 15%, in lieu of reciprocal tariffs. Section 122 tariffs, which give legal authority to impose universal tariffs on imports for a period of 150 days, is a temporary measure and we expect a substantial replication of struck-down IEEPA tariffs via Section 301 tariffs, which give legal authority to set country-specific tariffs after investigation of trade practices. The administration has already announced Section 301 investigations last week against many trading partners which are linked to “structural excess capacity and production in manufacturing sectors” and “forced labor.” These new trade investigations will likely be completed prior to the expiration of Section 122 tariffs on 24 July to allow tariffs to remain in place uninterrupted.

More importantly, however, the administration has also concurrently broadened product-level exemptions as the list of exemptions for Section 122 tariffs was expanded compared to IEEPA tariffs. This expansion of exemptions is likely to provide bigger relief than changes in tariff rates in the medium term. Considering recent tariff developments including a number of trade agreements with US trading partners, we lower our expectation for the long-term average effective tariff rate and now expect it to settle within a range of 8-9% from 14% previously.

US Tariff Implementation Measures

Bilateral Deals and Product Exemptions Drive Tariff Reductions

US tariff policy has de-escalated on net over the past six months. During that time, the White House has announced a number of bilateral trade deals, many accompanied by a commitment to reduce or eliminate tariffs on products listed under the Potential Tariff Adjustments for Aligned Partners, (“PTAAP”). The US also agreed to significantly reduce country-specific reciprocal tariff rates on China and India.

Currently, the tariff rate levied under Section 122 stands at 10%; however, President Trump’s and Secretary Bessent’s remarks have raised the risk that it will rise to 15%. A rise to 15% could put existing trade deals in jeopardy, as the UK and Australia negotiated a 10% ceiling, while agreements with the EU, Japan, South Korea, and Switzerland cap the combined MFN (Most Favored Nation) and additional tariffs at 15%.

In addition, the administration announced new relief measures (e.g., reimbursement of tariffs for imported parts used for domestically assembled trucks, broad tariff-exemptions for imported semiconductors for domestic use, etc.) against the backdrop of new Section 232 product-specific tariffs.

Response to Legal Challenges in Tariff Enforcement

On 20 February 2026, the Supreme Court struck down IEEPA tariffs. In response, the White House announced 10% universal tariffs under Section 122, effective on 24 February, with President Trump threatening to raise this rate to 15%. USMCA (United States, Mexico, Canada Agreement) compliant goods remain exempt, and Section 122 tariffs do not stack up on top of existing Section 232 tariffs.

Tariff Exemptions Take Precedence over Lower Headline Rate

The administration significantly broadened tariff exemptions under Section 122 universal tariffs. Relative to earlier lists, the Section 122 exemption list is larger by roughly $350bn in annual imports (2025 basis). In our estimates, this expansion reduces the aggregate effective tariff rate by about 1.0pp.

We believe lower tariff rates under Section 122 will only provide temporary tariff relief, ending when the US replicates the IEEPA tariff structure via Section 301 tariffs. We calculate that $925bn of imports (roughly one-fourth of total US imports in 2025) are currently subject to Section 122 tariffs. These goods previously faced about 16% of tariffs on average under IEEPA.

Country Specific Tariffs via Section 301 Outlook

USTR Ambassador Greer initiated Section 301 investigations into 16 major trading partners, with which consultations will take place until 5 May. This Section 301 investigations are linked to "structural excess capacity and production in manufacturing sectors,” and the federal register notice mentioned structural excess capacity “can be evidenced by the existence of large or persistent trade surpluses in certain sectors.” This suggests that tariff actions are very likely to happen regardless of the investigations and resulting consultations.

Separately, USTR initiated additional Section 301 investigations of 60 foreign countries, focusing on forced labor issues. A draft of the federal register notice refers to some research conducted by the International Labor Organization (ILO), as well as US Department of Labor (DOL), on forced labor in other countries. This suggests that their investigation process could be expedited by leveraging findings from DOL and ILO.

These new trade investigations will likely be completed prior to the expiration of Section 122 tariffs on 24 July to allow tariffs to remain in place uninterrupted. Although Greer said that existing trade deals with foreign countries are independent of new Section 301 investigations, they will be considered, suggesting that the new tariff rates will likely be similar to IEEPA tariffs.

We expect the US to largely replicate IEEPA tariffs through Section 301 country-specific tariffs.

Administration’s Focus on Affordability

A majority of new additions to the tariff exemption list are civilian aircraft and their related products, but the definition includes some consumer products, which should help mitigate consumer price inflation. The White House separately added several food products to the tariff exemption list, indicating that policymakers are sensitive to tariff-induced price pressures on grocery prices. As discussed in a previous note, we believe that the Trump administration will continue to focus on affordability issues, which should prevent tariff policy from escalating

Escalation Risk Remains

Tariff uncertainty remains elevated, and the risk of renewed escalation cannot be dismissed. Following the Supreme Court ruling, the EU Parliament discussed incorporating a suspension clause in a prospective EU–US trade arrangement. Separately, President Trump also threatened to curtail trade with Spain amid tensions related to the Iran conflict and threatened to impose 100% on Canadian imports in the event of a Canada–China trade agreement, underscoring the scope for renewed volatility.

For more information about this topic please contact reach out to Ruchir Sharma.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.