Despite price hikes, wage hikes, and rate hikes becoming more deeply rooted in 2025, Japan has yet to see the mutual reinforcement of price hikes and wage hikes, according to Kyohei Morita, Nomura’s Chief Japan Economist, speaking at the Nomura Investment Forum in Tokyo in December.

“To achieve sustained 2% inflation, price and wage hikes must become a single economic phenomenon, but in Japan they still occur separately,” he said. “Next year’s top task is to integrate price and wage hikes.”

Expectations for more durable wage hikes and rising productivity

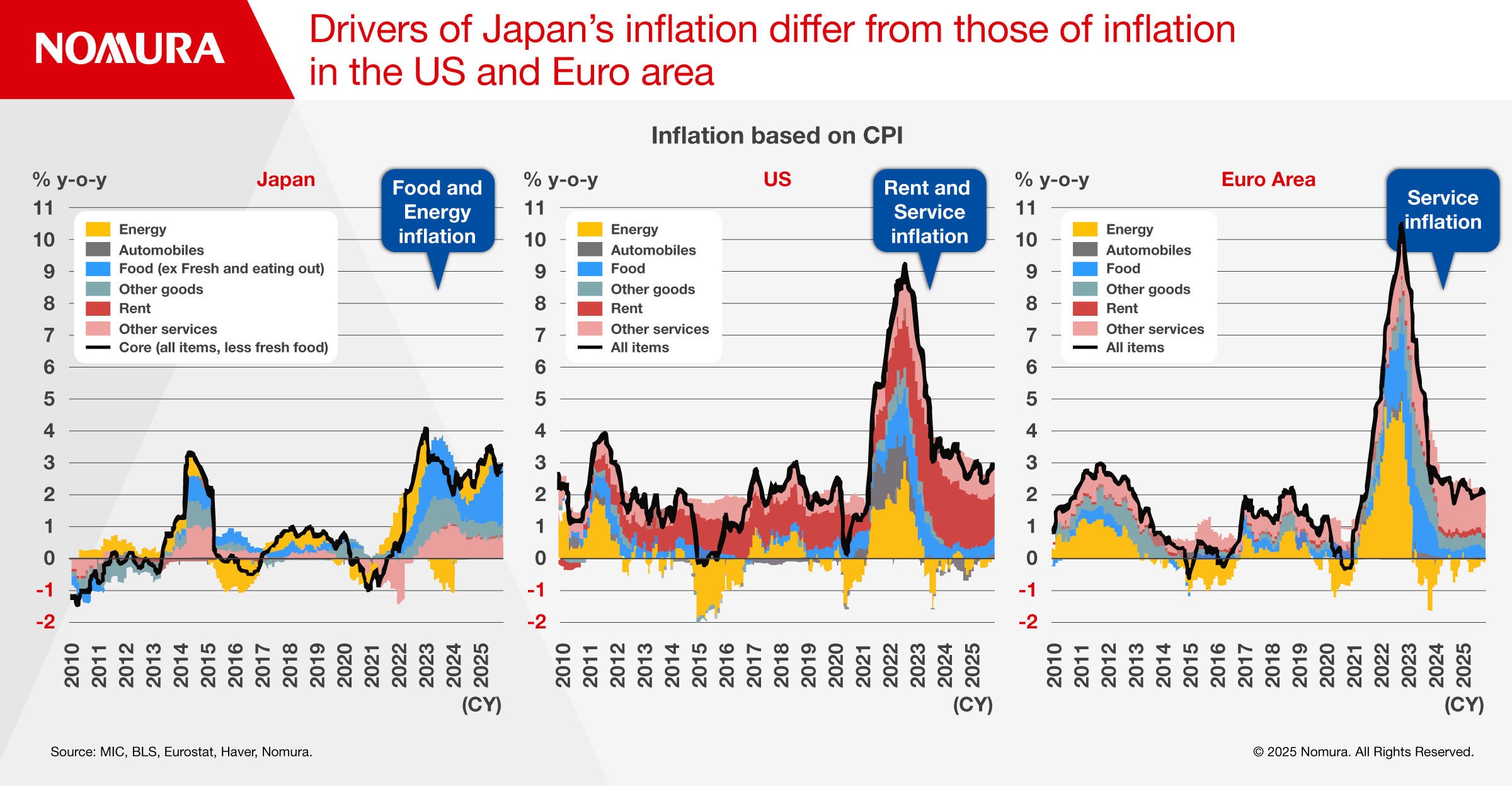

Morita noted that inflation in Japan is different from other advanced economies. It has been driven by import-dependent food and energy, while inflation in the US and the Euro area has been driven by domestic items such as rent and services.

But Japan is moving in the right direction. One example he gave was that investments in software are increasing, which suggests that companies are lowering their reliance on labor.

“I’ve watched Japan’s economy for about 30 years, and I’ve never felt more confident that productivity could truly rise,” he said.

Another key change Morita has observed is the way wage hikes are decided. Survey responses show that more firms cite peer companies’ wage hikes as a reason for their own hikes — something that historically has not been the case in Japan because of its enterprise unions. He said a market price for labor is emerging and that if companies pay below it, people quit, and companies find it more difficult to hire. With a tight labor market and greater mobility, wage market pricing can take hold, and that supports the durability of wage hikes.

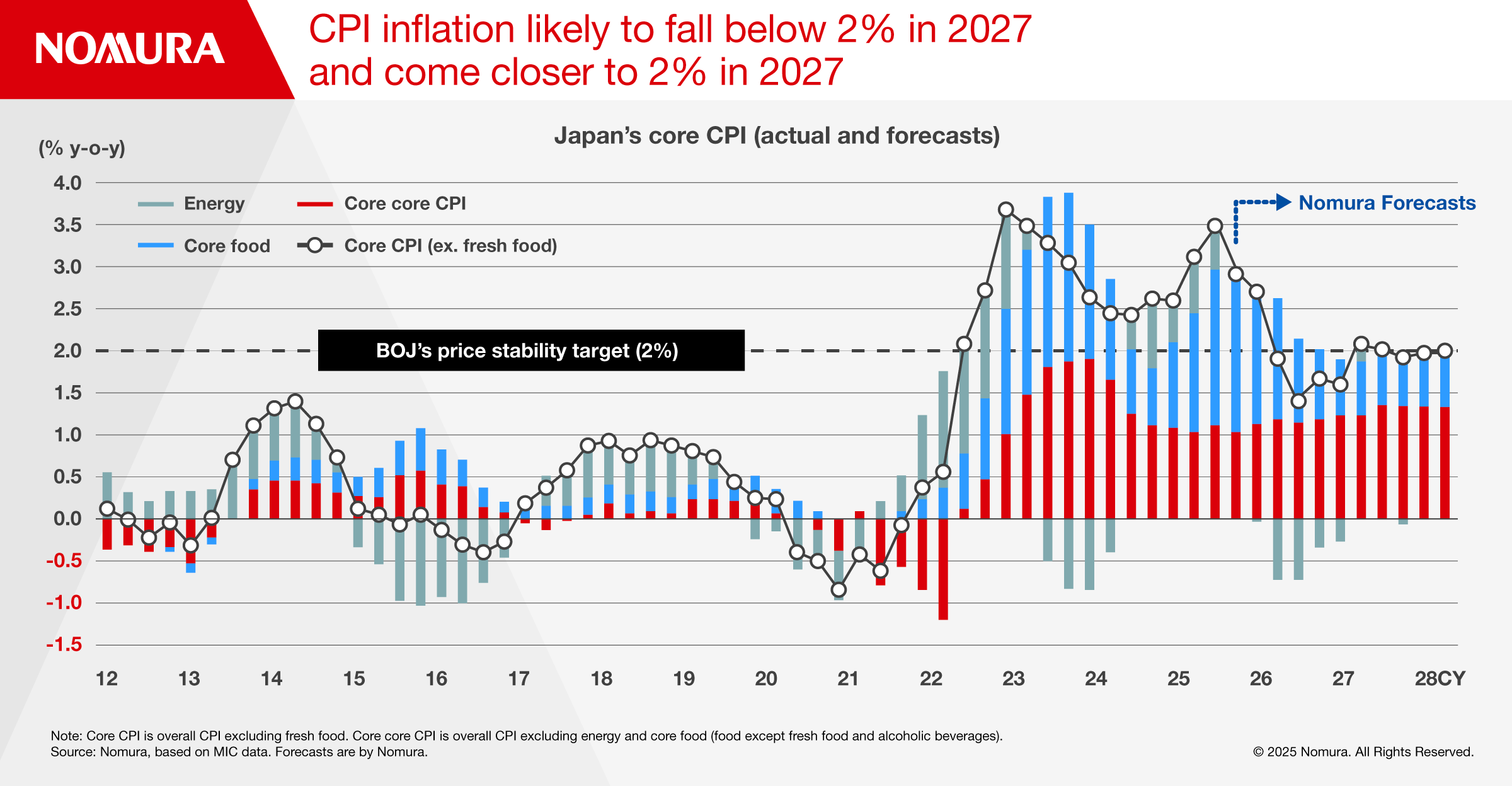

Morita believes inflation will dip below 2% in 2026 and core CPI (excluding fresh food) will likely be below 2% throughout the year, due to factors such as a normalization in food prices, stable global oil prices, and the expectation of a softer USD/JPY.

Watch Morita summarize the key points of his talk in a brief interview at the Nomura Investment Forum.

Tolerance for a weak yen may not last

Despite strengthening early in 2025, the yen started weakening in July and has remained weak. This has been driven by heightened expectations of a reflationary fiscal policy and increasing yen depreciation pressure under Prime Minister Sanae Takaichi’s new administration, explained Yujiro Goto, Head of FX Strategy for Japan. So, the key question for 2026 is how the administration’s tolerance for yen weakness will shift.

Traditionally, USD/JPY followed rate differentials closely, but since April, the link between them has loosened as global volatility fell and carry trades revived, he noted. In Japan, expectations of easier fiscal policy raised concerns about JGB supply and demand, dampening foreign inflows, even as yields rose, and higher yields did not translate into yen strength.

“Will a reflationary policy persist?” Goto asked. “A critical constraint is public sentiment, with concerns about inflation being very high in the polls ... Although wage hikes are progressing, inflation has outpaced them, hurting real wages and fueling discontent. This means that further yen weakness, along with import inflation, could become politically problematic in 2026.”

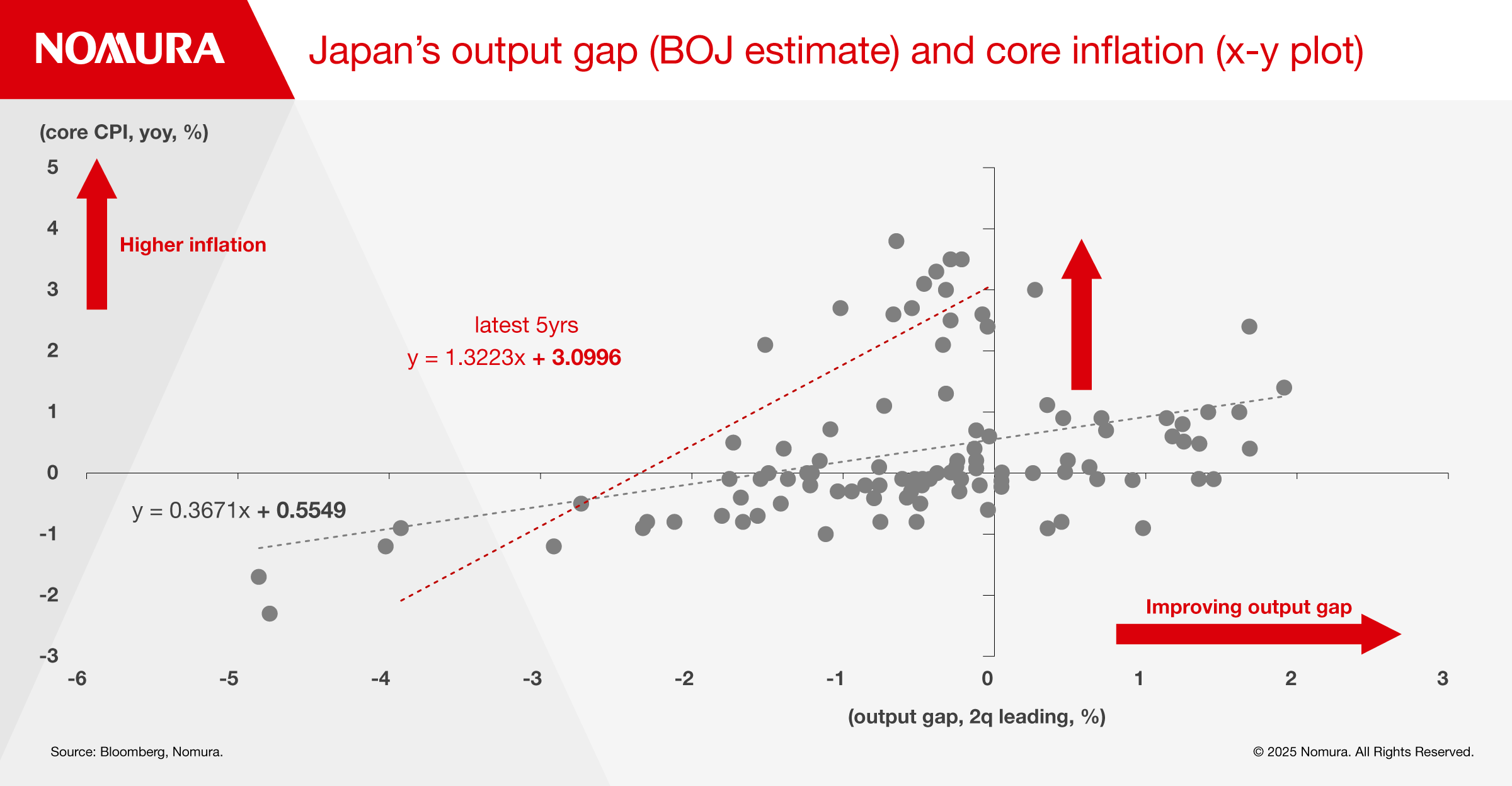

Japan may be more prone to inflation now, he acknowledged. Over the past five years, the slope in the relationship between the output gap and inflation has steepened. The exchange rate pass-through from FX to CPI has also risen, notably in services, which reflects inbound tourism. And prices are sticky on the downside. Companies raise prices when the yen weakens but do not lower them much when it strengthens, signaling changed pricing behavior.

Goto expects there to be lingering yen weakness through June then relatively quick appreciation in the second half of 2026 — potentially to between 145 and 140. Crosses such as EUR/JPY could remain high into March (around 180) and then fall, with acceleration coming later in the year.

“Given the direction of inflation, and the government’s response to it, we believe the bias toward a stronger yen may become clearer in the second half of next year,” said Goto. “And that’s something to watch closely.”

Winning conditions for equities in 2026

The industrial policy of the Takaichi administration — selectively supporting sectors where Japan can lead — presents a few “winning conditions” for equities, said Tomochika Kitaoka, Chief Equity Strategist.

The first one he noted was the environment of positive nominal growth and rising nominal rates, in which equities generally benefit. Both Takaichi and Minister of Finance Satsuki Katayama view nominal GDP growth exceeding nominal long-term interest rates as being crucial for the economy as this supports companies’ margins and profits.

Another winning condition Kitaoka discussed is the expectation of a 14% rise in the TOPIX EPS in FY2026 and of 9.8% in FY2027. This outlook reflects price hikes under a dovish fiscal stance, FX rate expectations, resilient US growth, and share buybacks.

“Double-digit earnings growth and a shrinking share count lead to favorable equity supply–demand dynamics, and I expect this situation to continue,” he said.

In terms of indexes, Kitaoka places more of an emphasis on the TOPIX because it has a broader earnings-based rationale, while the Nikkei 225 is heavily influenced by a concentration in stocks related to AI and semiconductors and is therefore more volatile.

Not all companies find themselves in favorable circumstances. B2B companies are mainly the ones that are succeeding in raising profits. Citing labor shortages, they are choosing to exit relatively low-margin, unprofitable businesses to concentrate on those with higher margins. Even if volumes do not increase, they can raise prices to increase profit margins. In Kitaoka’s view, this is the winning condition for B2B companies today.

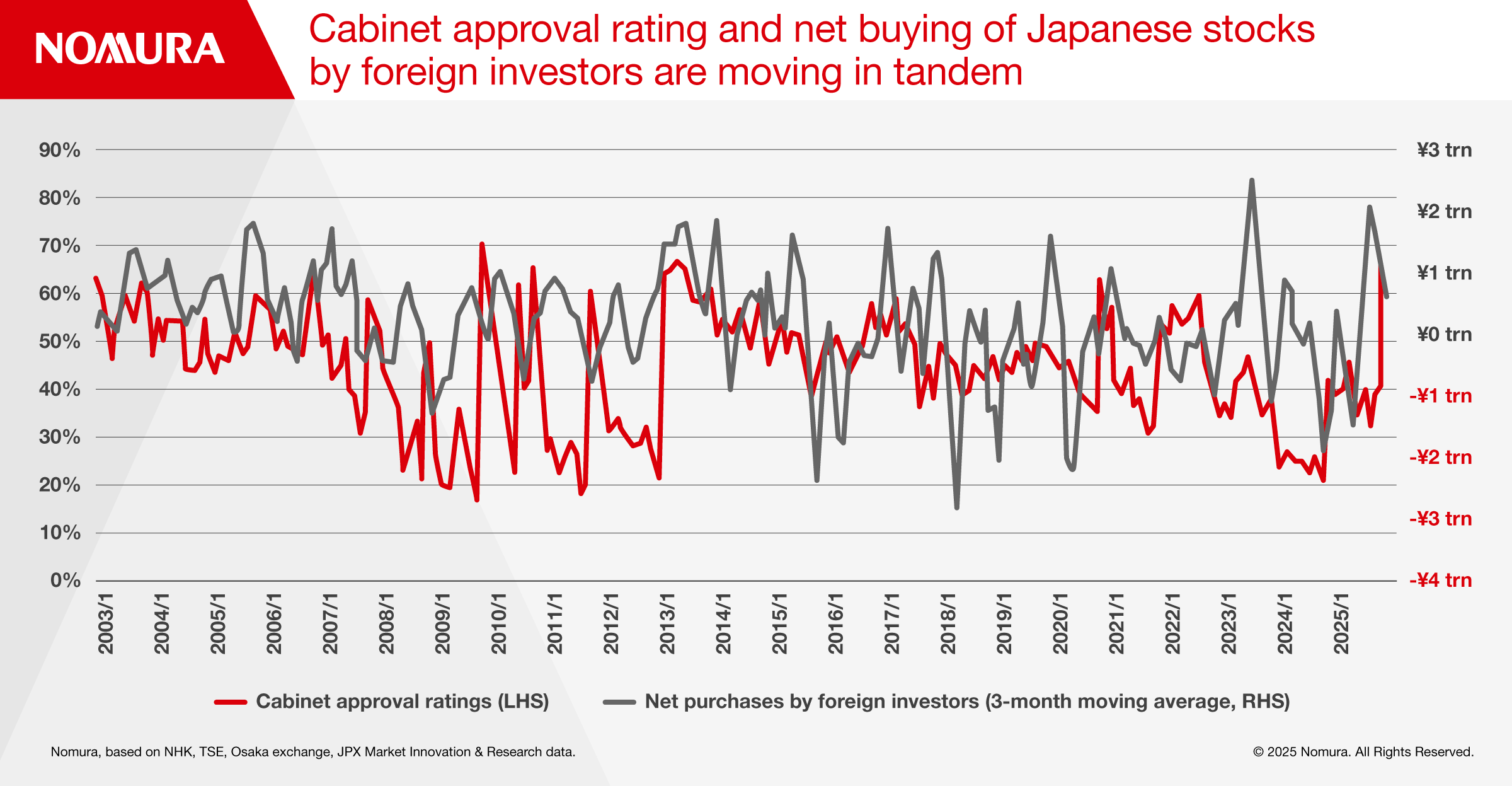

Kitaoka observes that overseas investors are more likely to invest in Japanese equities when the Cabinet has a high approval rating. They respond favorably to an environment where policymakers aim for high nominal growth while keeping rates contained and channeling capital to strategic sectors. Priority policy themes of this administration include defense and nuclear power, as well as new energy, such as fusion energy and perovskite solar cells.

“Looking beyond next year, in defense and nuclear energy, we think there is room for further expansion as budgets and policy frameworks broaden,” Kitaoka said. “We see opportunities.”