This article was produced in collaboration with

Introduction

Although gender is the core diversity issue facing East Asian organizations, it does not end there. Hence, we continue with diversity and inclusion as a positive ESG attribute and focus here on the employment of people with disabilities – the world’s largest minority group. We do so from the dual and complementary perspective that not only does diversity and inclusion promote human well-being for all employees through an enhanced sense of belonging, it improves business performance and sustainability. It is therefore a key concern for ESG investors.

In article 5 in our series on the ‘S’ factor in ESG in East Asia we looked at gender diversity in employment at South Korean listed companies. Although we found great variation among companies and sectors, there were some common areas of concern around the recruitment of women into core positions and their promotion into leadership ranks, as well as the complicated issue of data disclosure and its meaning.

Beyond this there lies the question of other minority or marginalized groups. We saw in article 4 that East Asia is entering a long-term period of labour scarcity. With the ageing and reduction in the male labour force, companies can ill afford to maintain restrictive hiring practices that amount to statistical discrimination.

Achieving numerical diversity is just the start. Unless companies can include employees from minority and marginalised communities into core and leadership roles, they will find it hard to reap the business performance and financial successes that the diversity dividend can unleash.

Disabled Employment In East Asia

There are few job tasks within a modern developed economy that cannot be done by people with disabilities. Yet, employment rates of disabled people worldwide are much lower than those of able bodied, even within countries and in occupations experiencing severe labour shortages. Barriers to employment may lie outside the workplace, such as in transportation, family circumstances and living conditions, as well as in individuals’ perceptions of themselves. However, barriers also lie within organizations, including prejudices regarding disabled people’s capabilities for contributing to organizational performance.

There is already ample evidence demonstrating that the inclusion of disabled workers not only does not harm a business, it can enhance it. In the United States, for example, ‘Disability Inclusion Champions were, on average, two times more likely to outperform their peers in terms of total shareholder returns,’ and ‘companies that have improved their DEI score over time were four times more likely to … outperform their peers.’

Both South Korea and Japan are shifting from a medical and welfare model of disability towards a social and rights-based understanding. This partly explains why each has a low ratio of registered disabled of under 10% compared to other OECD countries, whose ratios cluster around 15-25%. Significantly for East Asia, disability is increasing with population ageing, and the need among older adults to continue working is increasing with lower numbers of children available for care in later life.

South Korea and Japan implement a quota, levy, and subsidy system for disabled employment, using the revenues collected from the levy to offer subsidies for companies exceeding their quota. Currently the South Korean quota requires the employment of 3.6% disabled employees in public sector organizations and 3.1% for larger private sector companies. Korean companies’ uptake of disabled employees has been increasing over the long term, with 34.6% of disabled adults now in employment. However, there remain criticisms that companies are more willing to pay the levy and keep disabled employment low, rather than make the changes necessary in reducing barriers and increasing employment to match or exceed the quota.

There is still a pervasive belief globally that disabled people are a dependent group and a cost, rather than an asset, that employers are unwilling to shoulder, and that the state, non-profit organisations, or families and communities should mainly be responsible for their support.

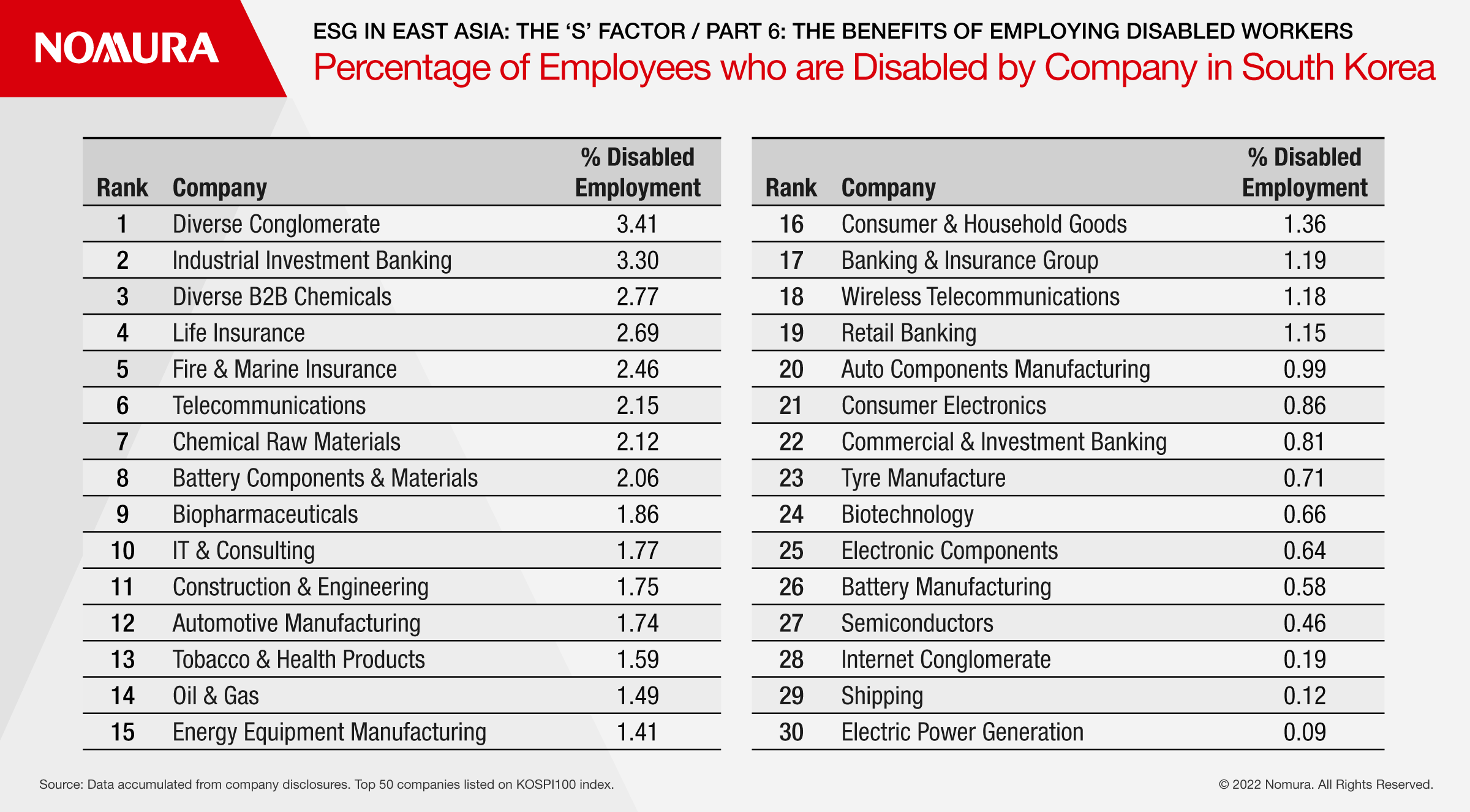

In our research among listed companies in South Korea we found a few companies already making great strides in disabled employment. By our calculations, two out of fifty top companies comfortably exceeded the government set quota, with another handful of companies approaching their quota. However, there remain a larger number who, thus far, demonstrate that they perhaps do not acknowledge the problem because they do not disclose data, or who undershoot their quota significantly.

Sectorally, there is a greater mixture among top companies in disabled employment than for gender diversity, and we argue that the latter is because of entrenched traditional attitudes regarding the types of work that women should or can do. Among the top disability employers, three were three financial services firms, mirroring performance in gender diversity. However, there were also three chemicals companies, one each in telecommunications, biotechnology, and IT, and a large diverse Korean conglomerate topped our list with an employment ratio of 3.41%.

Conclusion

High quality employment standards are the foundation-stone for high performance across the whole ESG spectrum. Key to achieving this is an active and vigorous diversity and inclusion policy.

There is an enormous consumer market out there eager to discover which companies support their needs, desires, beliefs, and dreams. Half of the world’s population is women. Over 1 billion people or 15% of the world’s population is in some way disabled. To repeat, they are the world’s largest minority group. More than a fifth of the world’s population is East Asian. Every country in the region is either already affluent, or soon will be, and with that comes more discretionary spending.

A more vigorous diversity and inclusion policy would enhance South Korean business and, consequently, financial performance in a number of ways. It expands the available pool of high-quality employees just as all East Asian countries are entering a period of prolonged labour shortage. Those employees provide valuable and alternative leadership perspectives which reduce risk. They add innovation and creativity to products, services, and processes. Outputs can be tailored to meet the demands of new customers and expand a company’s market share, and they allow companies to expand their range of products and services to develop new markets.

The 21st century is an age where authenticity and responsibility in business and commerce count. East Asian companies are yet to properly understand, and therefore reap, the diversity dividend. Not only do companies need to achieve greater numerical employment balance, but they need to include employees from minority and marginalised groups into core and leadership positions. It is the right thing to do; and it will enhance business and financial performance.