In 2025, we stated our view that the Japanese economy is transitioning to what we dubbed a “normal economy” as price hikes, wage hikes, and rate hikes — the “three hikes” — become entrenched.

Now that a year has passed, we believe the Japanese economy has been changing largely in line with our expectations. Three developments illustrate the positive changes taking place:

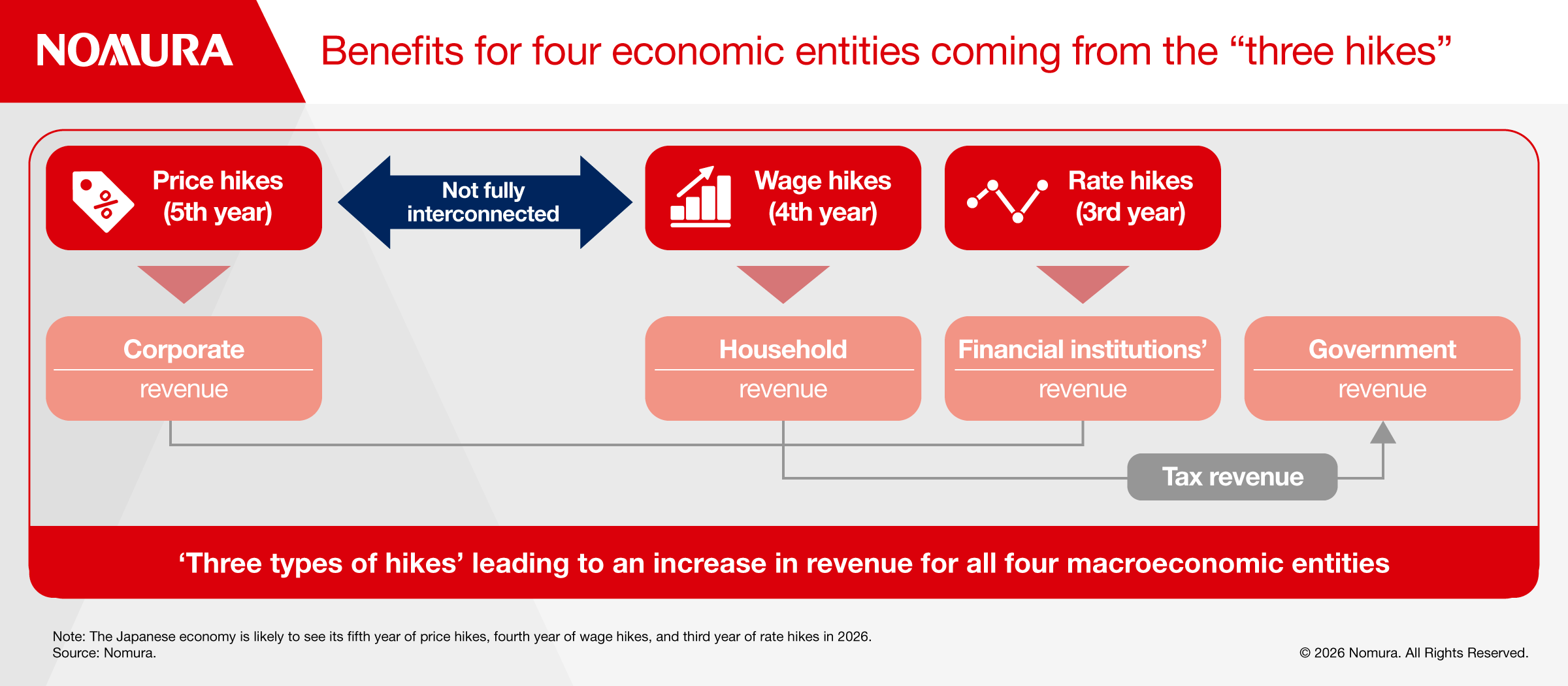

- benefits from the three hikes for four macroeconomic entities

- reduced reliance on humans, such as through software investment, which leads to an increase in labor productivity

- increased synchrony and sustainability of wage hikes

Benefits to four economic entities

In 2026, the Japanese economy is likely to see its fifth year of price hikes, fourth year of wage hikes, and third year of rate hikes (Figure 1).

Price hikes stimulate companies’ top lines through sales. Wage hikes equate to top-line growth for households. And rate hikes, if they become entrenched, lead to top-line growth at banks and other financial institutions that are lenders. During phases when these three hikes occur, tax revenue is also expected to increase, boosting the government’s top line.

With these three hikes occurring in Japan, we expect to see these benefits for all four macroeconomic entities — companies, households, financial institutions, and the government — as the Japanese economy moves closer to a fully functioning, normal economy in 2026.

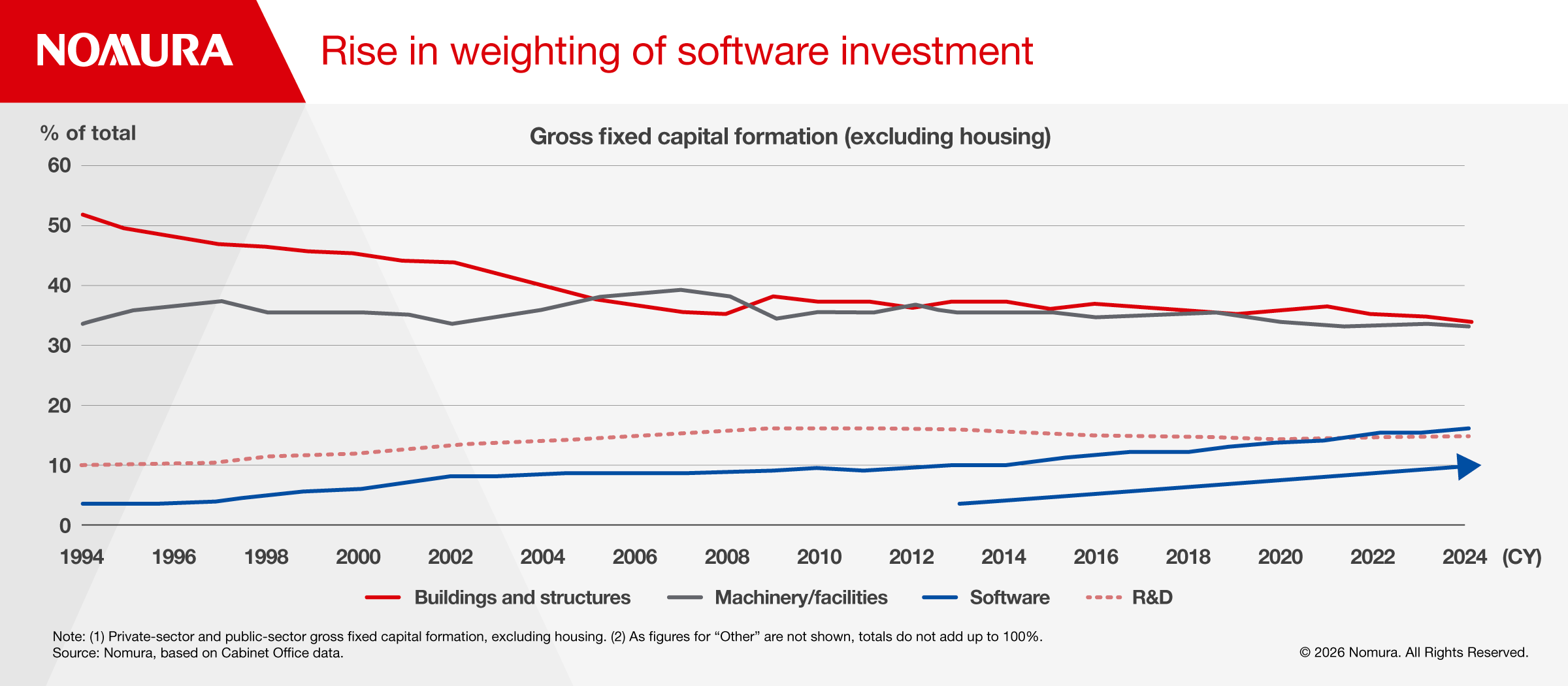

Software investment reduces reliance on humans

Changes in capital expenditure also point to changes in the Japanese economy. An example of this is the increase in software investment.

Software accounted for 16% of private-sector and public-sector gross fixed capital formation (excluding housing) in 2024, surpassing R&D (Figure 2). Also, according to METI and BOJ data, there has been a clear upward trend in the sale of custom software since 2021.

Japan’s population aged 15 and older — Japan’s available labor force — has been declining since 2021, which means it is no longer possible to resolve Japan's labor shortage by hiring more workers. One way companies can adjust to this reality is to reduce their reliance on humans and increase their investment in software. Capex is then likely to become less of an amplifier of peaks and troughs in the economy and more of a stabilizing force, while also translating into an improvement in labor productivity.

Increasing synchrony and sustainability of wage hikes

In Japan, labor unions have historically been organized by company rather than by industry, so wage hikes have tended to be based on company-specific decisions. Labor market fluidity has also been low. This means a company’s wage raising activity has not typically been influenced by that of other companies.

However, in 2026, wages are expected to be raised for a fourth straight year. Over the past four years, the percentage of companies citing wage developments at sector peers as a reason for their own wage hikes has been edging upwards.

In the context of severe labor shortages, if a company were to become reluctant to raise wages at a time when its peers continued to raise wages, we think it would see workers leave or threaten to leave. As a result, a growing number of Japanese companies are becoming more aware of a market rate for wages, and they are considering wages at sector peers when setting their own wages. This has brought about synchrony in wage hikes.

Wage hikes could also become more sustainable if the improvement in labor productivity, backed by a reduced reliance on humans, were to be added to the mix.

If this stage is reached, we think the three hikes would become stickier and the benefits of simultaneous top-line growth for the four economic entities would finally become entrenched.

Responsible fiscal policy

In the past year, the start of the Takaichi administration has significantly changed the environment for the Japanese economy. Sanae Takaichi, who became LDP president and Japan’s prime minister in October 2025, can serve a maximum of 11 years, until October 2036. This would be much longer than the 2,822 days that former Prime Minister Shinzo Abe served during his second premiership.

Even if Takaichi is able to remain in power, the economic environment surrounding fiscal policy management will be very different from what Abe had to contend with: Abe battled deflation, Takaichi will be fighting inflation.

From bonus to onus

The impact of inflation on fiscal policy tends to change over time. Inflation stimulates nominal GDP growth at an early stage, resulting in a bonus for government finances in the form of an increase in tax revenues. Meanwhile, as government debt is largely on fixed interest rates, the effective interest rate — which reflects the government's interest payments — does not tend to rise much at first. As a result, growth tends to be greater than the effective interest rate in the initial stages of inflation.

However, as time passes and existing Japanese government bonds are refinanced, the government interest payment burden (i.e. the effective interest rate) begins to rise in line with the market interest rates under inflationary conditions. If the increase in tax revenue is a bonus that inflation yields for fiscal policy, the increase in interest payments is the onus left by inflation.

When inflation starts to become a burden on government finances

The longer the maturity of government debt, the later the onset of the burdens of inflation. As of the end of 2024, the average maturity of bonds issued was 14 years in the UK, 9.5 years in Japan, 7.4 years in Germany, and 5.9 years in the US.

At 9.5 years, the average maturity of JGBs is fairly long, but this is still shorter than the potential tenure of Sanae Takaichi’s administration, which means it could be faced with the burdens of inflation. Considering this, we think there would be considerable value if the government were to implement responsible fiscal management from an early stage in order to curb the market’s concerns about fiscal sustainability.

The litmus test for responsible fiscal policy

We are not advocating fiscal austerity. We think proactive fiscal management will contribute to further entrenching the three hikes, as long as the aim is to sustain a situation where growth is greater than the effective interest rate. This can happen by taking advantage of the bonus provided by inflation in the early stage and boosting the economy's growth potential. We think a litmus test of responsible fiscal policy management is whether it contributes to growth being greater than the effective interest rate.

Despite several external threats — including a sharp rise in Dubai crude oil prices and Chinese government restrictions on exports of rare earths to Japan — we think the Japanese economy will continue to change from within, based on the three hikes, in 2026.

To read the full report, click here.