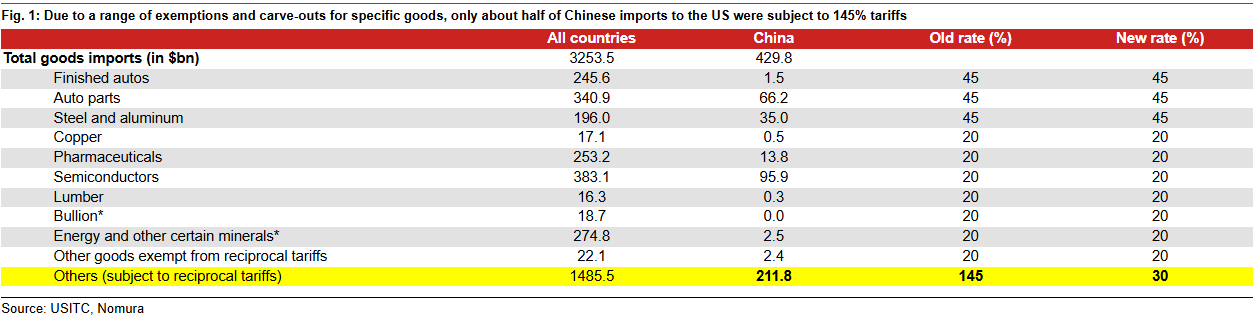

Many China goods unaffected by tariff reduction

The Trump administration announced that the US and China had agreed to reduce reciprocal tariffs by 115 percentage points for 90 days, a larger reduction than we expected. Due to a range of exemptions and carve-outs for specific goods (including consumer electronics, auto parts, and semiconductors), only about half of Chinese imports to the US were subject to 145% tariffs, leaving the rest unaffected by this deal (Fig. 1). With imports from China equal to just over 13% of total US imports, this implies that today’s deal is a dramatic cut in tariffs for roughly 6.5% of US imports.

Prospects for tariff deals

The outlook for US-China trade has improved with this 90-day freeze, but progress on trade negotiations for countries other than China has been slow and implied that 10% may be a hard tariff floor.

President Trump expressed confidence that the US and China would reach a deal during this 90-day period. In addition, he stated that although tariffs on China would rise if the two countries don’t reach a deal, the joint reciprocal and fentanyl tariff rate on China would not rise all the way back to 145%.

In contrast to the better-than-expected temporary agreement China, trade deals between the US and other countries have proceeded slowly. Thus far, there has only been a single deal, with the UK, a country with which the US already runs a trade surplus and which was never subject to reciprocal tariffs in excess of 10%.

The US-UK trade deal did not lower the US’s tariffs on the UK below 10%, a tariff level that may be a harder floor than we previously expected. Moreover, key US trading partners like Japan and South Korea have taken a relatively hard line with the US, so far refusing to agree to deals that don’t lower auto tariffs.

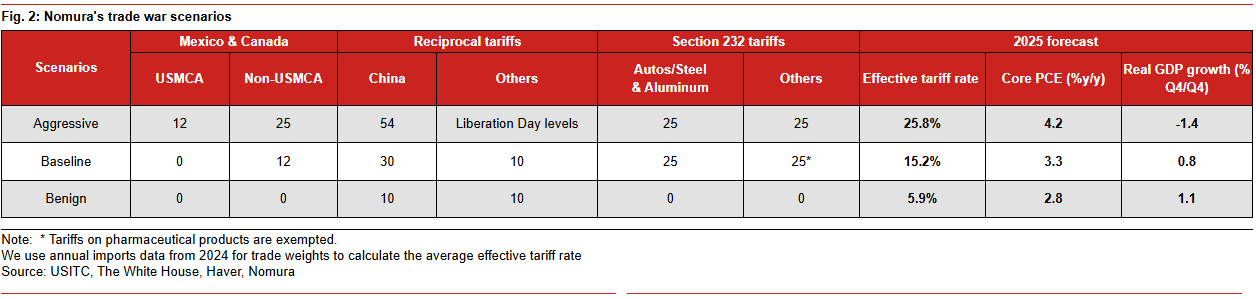

Updated trade & macro scenarios

Fig. 2 shows our current aggressive, baseline, and benign scenarios.

Our base case is for reciprocal and fentanyl tariffs against China to remain at the current 30%. Under this scenario, we expect the US to continue to implement sector-specific tariffs. Semiconductors, copper, timber, and lumber all appear likely to see additional tariffs. The exception is pharmaceutical goods, as President Trump signed an executive order on a most-favored-nation policy aimed to lower drug prices. In contrast, we assume country-specific tariff rates will remain unchanged at 10%, avoiding the increases scheduled for 8 July.

Our more benign tariff scenario assumes several trade partners successfully negotiate their reciprocal tariff rates below 10%. In addition, under this benign scenario, the US ends fentanyl tariffs on China, Canada, and Mexico. This scenario would also see the administration back down from all sector-specific Section 232 tariffs. Tariffs would still be elevated relative to recent history, but this scenario would not involve a major realignment of global trade.

A more aggressive scenario would see country-specific tariffs largely reverting to their Liberation Day levels. Under this scenario, sector-specific tariffs would continue to go into effect, and USMCA exemptions for Canada and Mexico would be allowed to lapse, reverting tariff rates to 25% for all imports from North America. In addition, more Section 232 sector-specific tariffs would be implemented.

If reciprocal tariffs are allowed to revert to Liberation Day levels, a recession would still be the most likely outcome, with GDP growth around -1.4% Q4/Q4.