US Tariffs Raise Domestic Inflation Expectations

The cost pressure from tariffs is likely to push up the prices of both imported finished goods and domestically produced goods through the supply chain. We use an Input-Output table analysis to estimate the magnitude and composition of the cost-push shock.

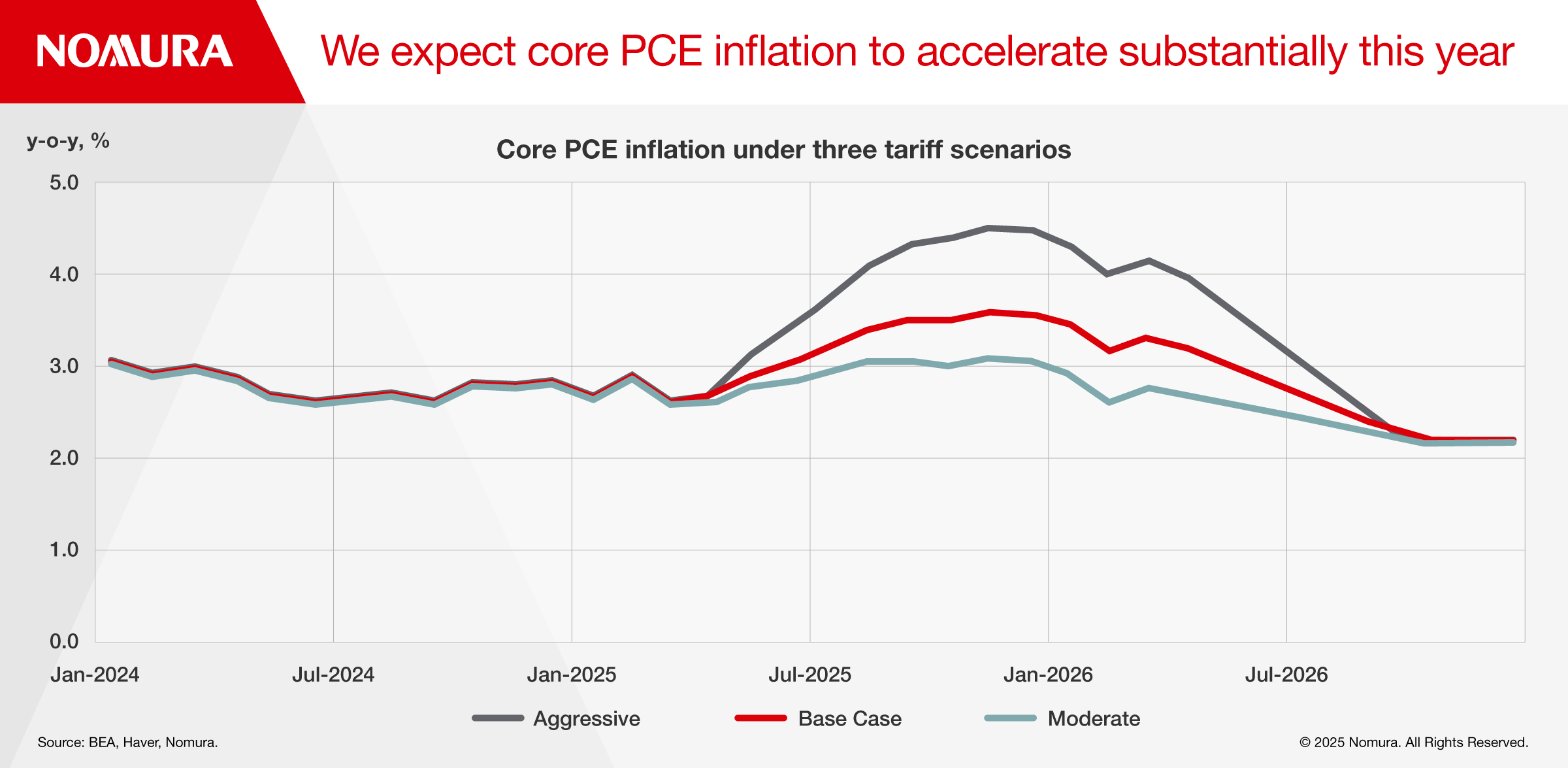

- Under our baseline scenario, we expect core personal consumptions expenditures (PCE) inflation to accelerate sharply to 3.6% y-o-y later this year.

- The cost pressure from tariffs is likely to push up the prices of both imported finished goods and domestically produced goods through the supply chain. We use an Input-Output table analysis to estimate the magnitude and composition of the cost-push shock.

- Beyond the impact on imported goods prices, we see risks of both positive and negative spillovers into domestic inflation dynamics.

- Focusing on the future trajectory of major components of the price index will be crucial to gauging whether tariffs lead to a one-off inflation spike or more persistent price pressure.

There are few historical precedents for the recent escalation in US trade restrictions. Beyond uncertainty over trade policy itself, the magnitude, breadth, and rapid implementation of tariffs all create uncertainty for the inflation outlook.

In this note, we lay out a model for the inflation impact from tariffs. Both the magnitude of the inflation shock as well as the composition among components will be important for gauging the risks of more persistent price pressure.

The cost shock from tariffs

To translate higher import prices into domestic inflation, we create an Input-Output table price model, which enables us to analyze the impact of higher import prices on domestic inflation by considering the indirect impact through inter-industry transactions in addition to the direct impact through import prices of finished consumer goods.

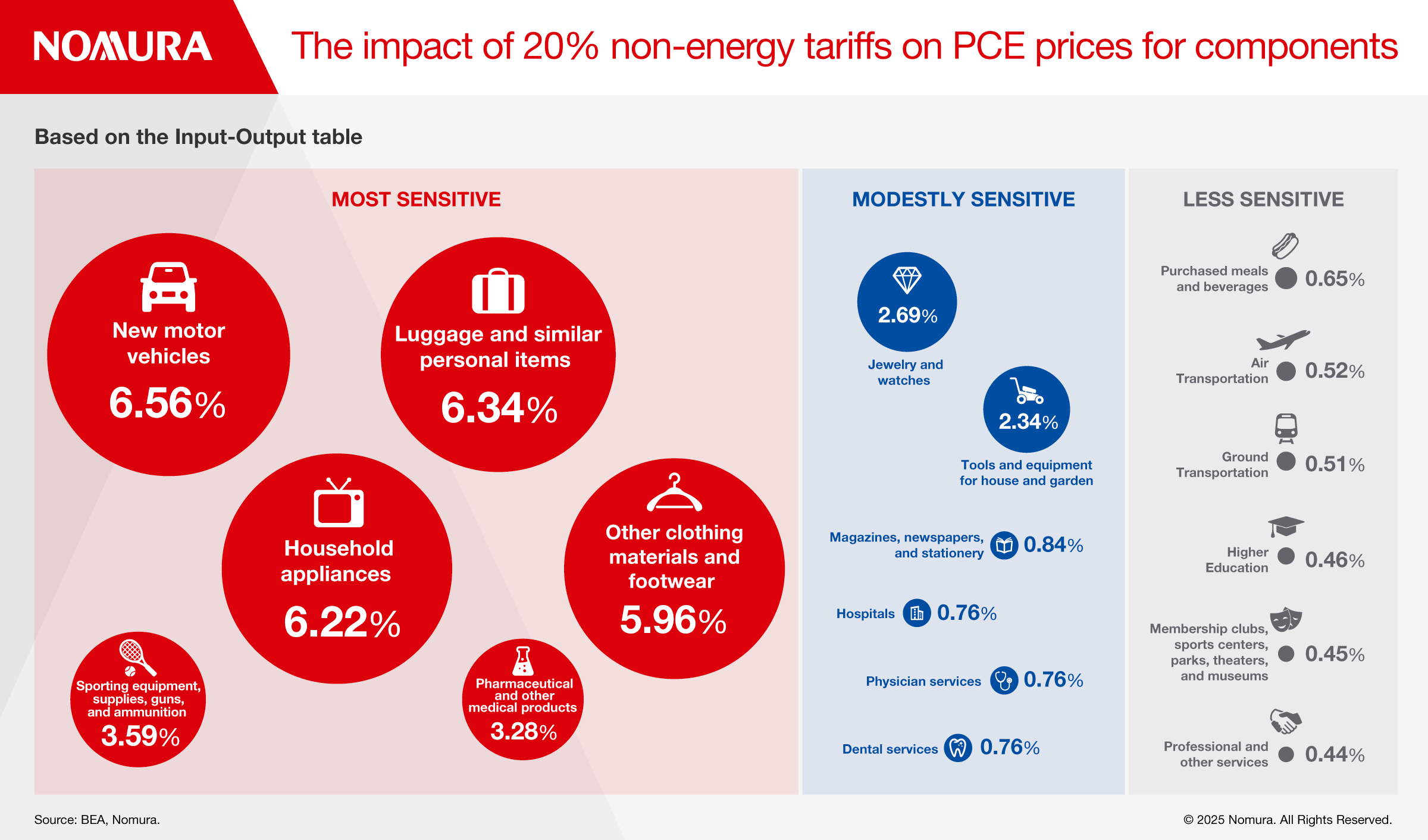

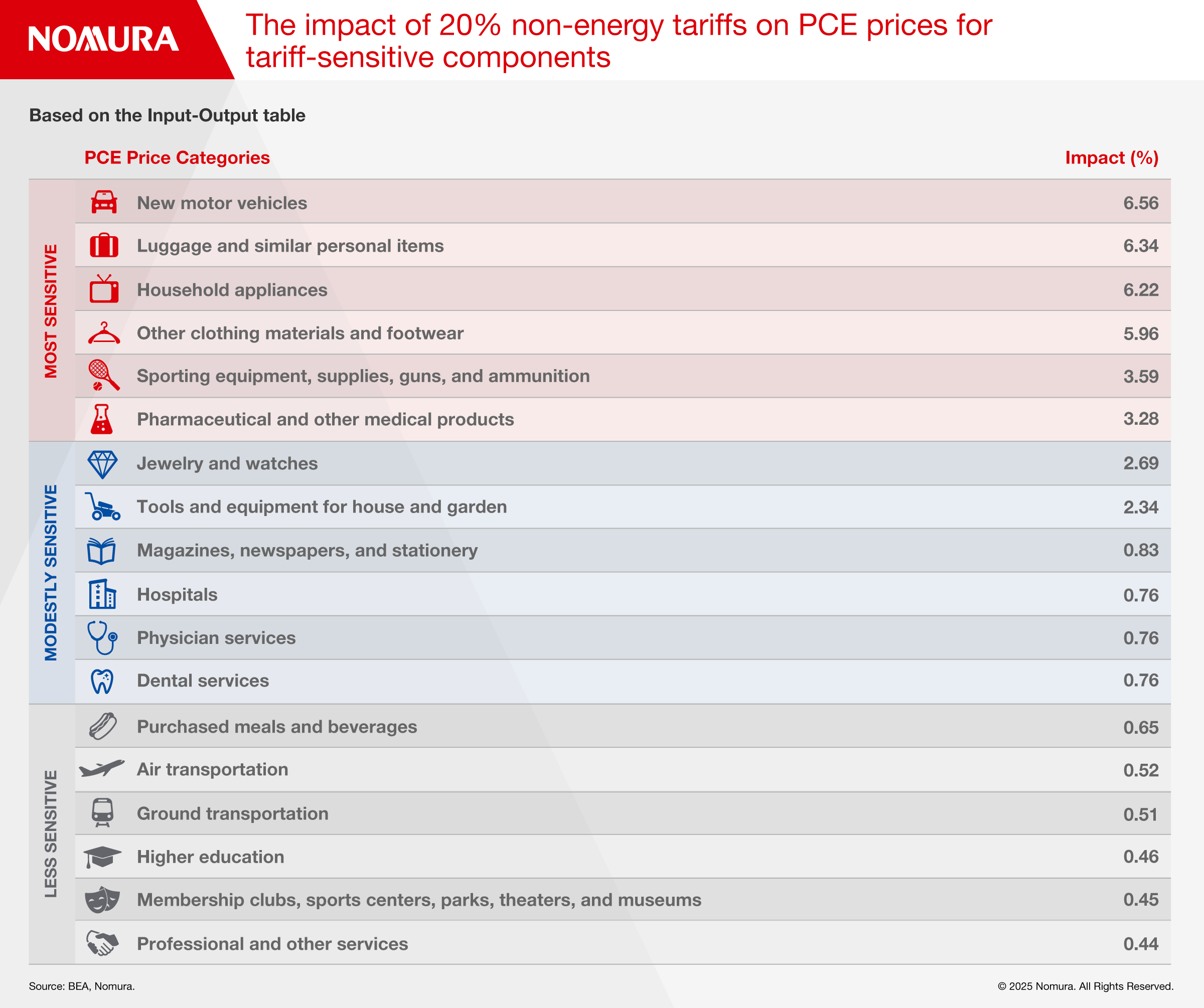

Core goods prices are more sensitive to changes in the tariff rate than service prices, but even among core goods prices, there is significant dispersion. For instance, new vehicle prices, one of the most trade-sensitive components, are affected due to higher prices of imported finished cars as well as imported parts through the supply chain. In contrast, some other goods are significantly less sensitive. For instance, we calculate the impact on new vehicle prices is eight times bigger than the impact on magazines and newspapers.

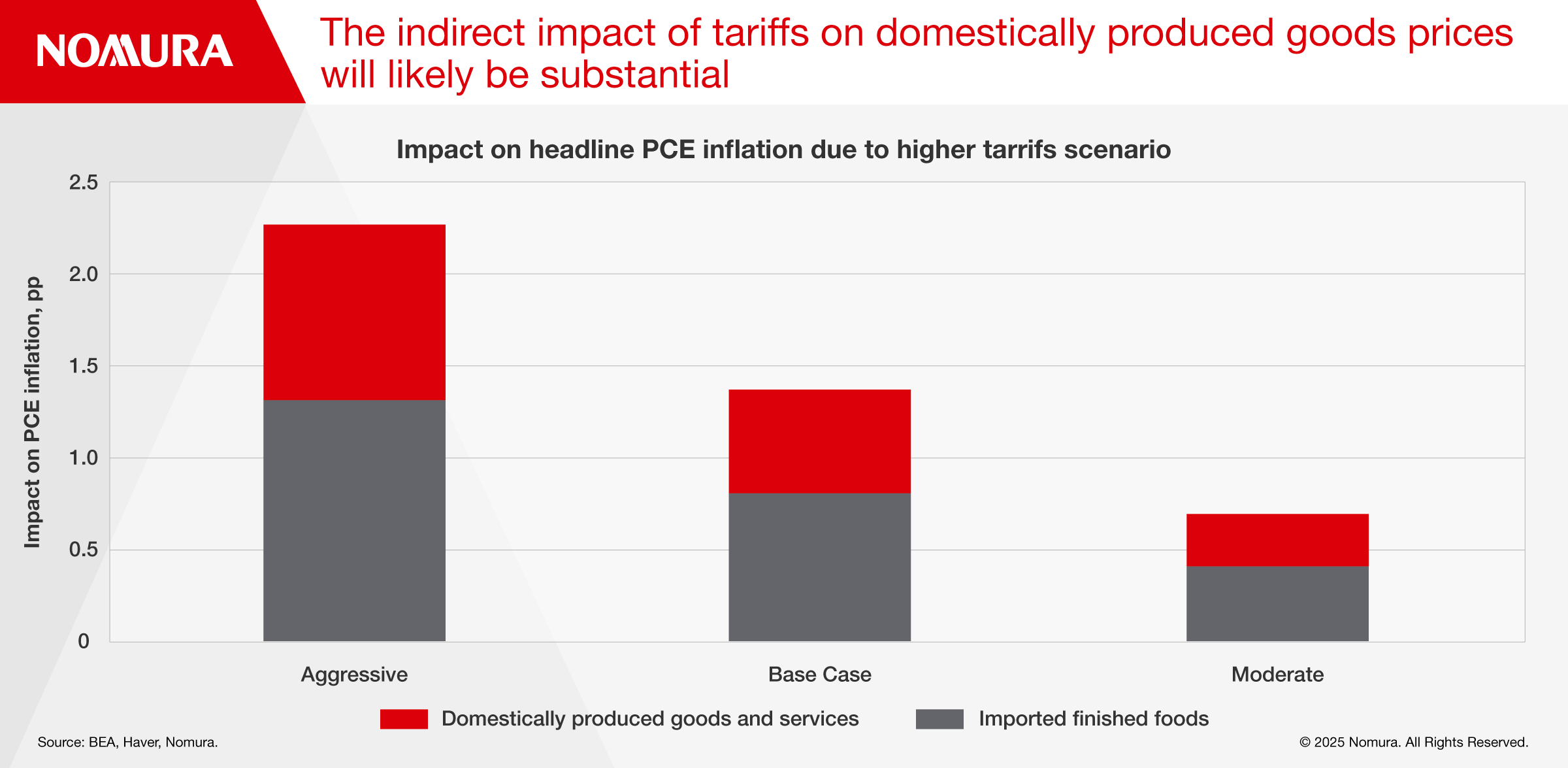

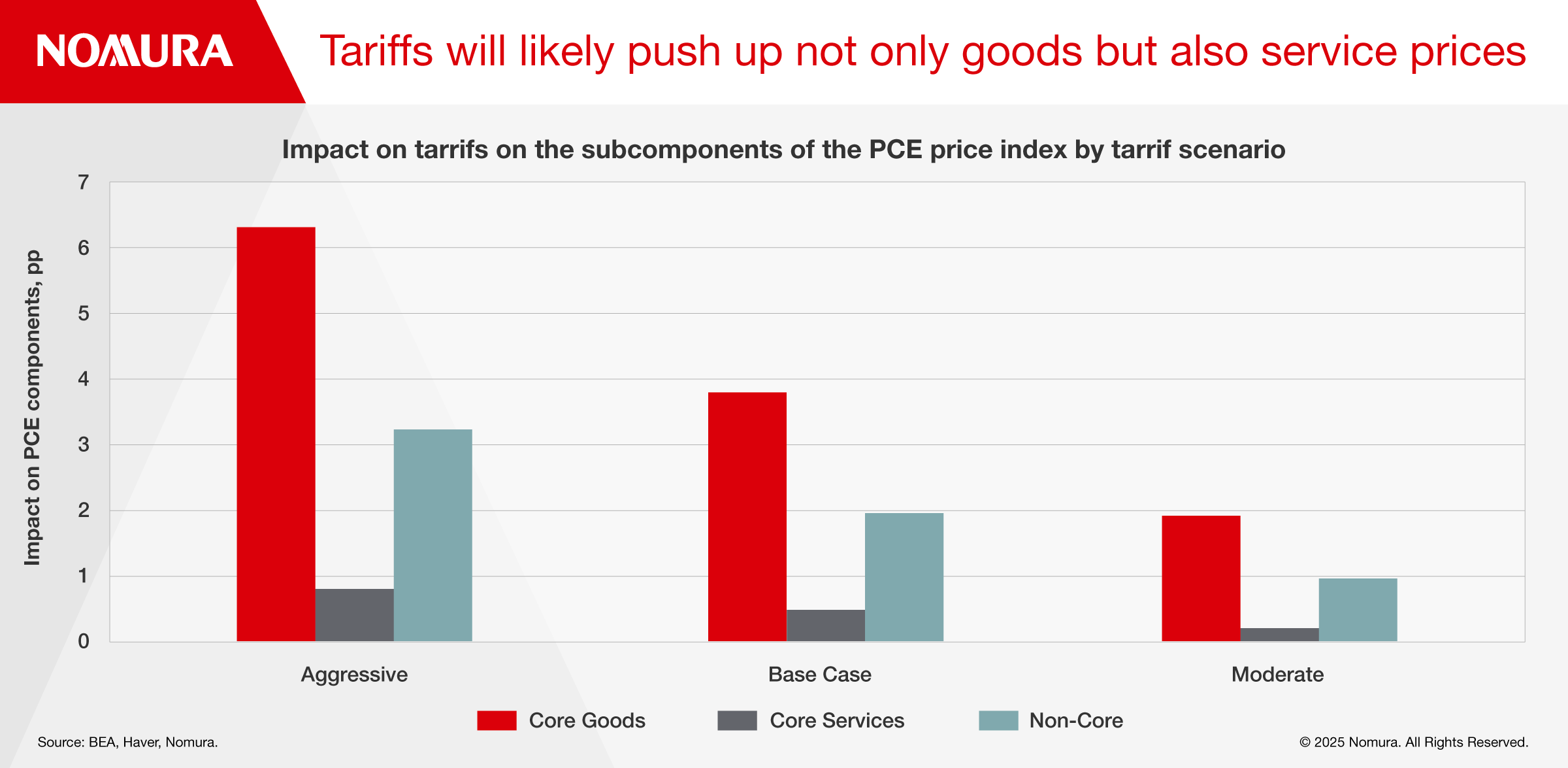

Using the Input-Output table, we impose shocks of 10%, 20%, and 33% increases in import prices for non-energy goods and estimate the impact on PCE inflation, corresponding to our “aggressive,” “base case,” and “moderate scenarios.” Under the base case, our model suggests 20% tariffs push up the PCE price index by 1.4pp with about 40% of the price shocks stemming through higher production cost increases for domestic producers. By expenditure type, PCE core goods and non-core components (primarily food prices) are very sensitive to higher import prices, but core service prices are also likely to increase modestly due to higher input costs.

Although the Input-Output table describes transactions between different sectors each year, we assume the price shocks caused by higher tariffs will largely materialize in Q2 and Q3 this year, considering the swift implementation of tariffs.

We incorporate our estimated shocks derived from the Input-Output table into our inflation outlook with minor adjustments. As a result, under our base-case scenario, we assume core PCE inflation will rise to 3.6% y-o-y in December 2025, while under the aggressive and moderate tariff scenarios, core PCE inflation would be 4.5% and 3.1% y-o-y, respectively (Fig. 3).

Interpreting inflation surprises

Beyond the value as a forecasting exercise, our framework also provides a benchmark for how to interpret inflation surprises in the months ahead. Beyond the magnitude of any inflation surprises, the composition of inflation will provide important clues as to whether tariffs are a one-off shock or a source of more persistent price pressure.

On the one hand, there is uncertainty about the pass-through of tariffs to directly impacted prices. We assume exporting businesses abroad do not significantly adjust to offset tariffs, but there is a possibility that more aggressive trade restrictions lead to cost cuts. The degree of shock absorption by retailers is also uncertain. Retailers absorbed some cost increases resulting from higher Chinese tariffs during Trade War 1.0 in 2018-19. However, the degree of shock absorption by retailers might be limited, as the universal nature of reciprocal tariffs should constrain the capability of domestic distributors to circumvent tariffs by increasing imports from non-targeted countries.

The more concerning risk, in our view, would be potential spillovers from tariffs into domestic goods and services. These types of surprises would have greater implications for the medium-term inflation outlook and Fed policy.

For goods producers, universal tariffs create an incentive for domestic producers to raise prices for domestically produced goods beyond what is implied by tariff-induced cost increases.

Used vehicle prices would be another instance of likely positive spillovers. These are not directly impacted by tariff costs, but would likely follow new vehicle prices higher. We have already seen some spillover effects on used vehicle prices, as dealers are raising prices in anticipation of a demand shift from new vehicle markets due to tariffs.

The table below shows the list of PCE price components in order of sensitivity to tariffs implied by the Input-Output table.

Beyond the aforementioned micro-level effects, tariffs also have the potential to affect inflation expectations. While the pandemic-induced inflationary pressures have not yet completely subsided, another inflation wave driven by tariffs could cause inflation expectations to become unanchored, making the inflationary shock more persistent.

Other potentially severe supply chain disruptions pose additional upside risks, too, but are not incorporated into our model. Even if an imported component is typically a small share of a product’s cost, supply disruptions could lead to outsize inflation impacts – like when auto prices rose sharply due to a shortage of semiconductors in 2021-22.

On the downside, macro headwinds could be caused by reduced aggregate demand in reaction to tariffs. This could make domestic retailers and wholesalers reluctant to pass on higher costs to their customers, but should also add disinflationary pressure to domestic goods and services. Sharp disinflation in less impacted goods and services could encourage the Fed to consider a return to pre-emptive rate cuts, since it would raise the risk that inflation may actually undershoot once the cost shock from tariffs has passed.

Contributor

Aichi Amemiya

Senior US Economist

David Seif

Chief Economist for Developed Markets

Jeremy Schwartz

Senior US Economist

Ruchir Sharma

US Economist

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.