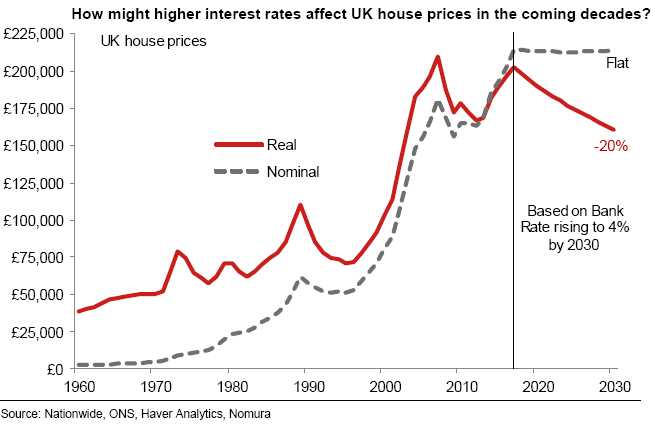

With predictions of a gradual rise in real interest rates, a fall in real house prices could happen. We believe real house prices could be 20% lower by 2030

The recapitalisation effect

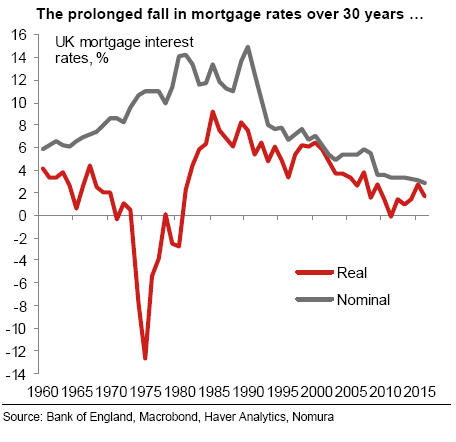

In the second half of the 1980s mortgage interest rates in real terms averaged over 7.5%. In contrast, in the five-year run-up to the global financial crisis they averaged less than half that, at 3.5%, and over the last five years they have halved again, averaging just 1.7%.

The persistent decline in mortgage interest rates over the past 30 years has been one of the most powerful influences that helped contribute to the more than fivefold rise in nominal (and 2.5-fold rise in real) house prices over that period.

What is more interesting is that following the sizable fall in interest rates and rise in house prices, the repayment-to-income ratio is now exactly in line with its long-run average. This indicates that, when it comes to affordability, the fall in mortgage rates has been completely offset by an equivalent rise in house prices known as the ‘recapitalisation’ effect.

From recapitalisation to decapitalisation Now imagine this process in reverse. How far do house prices have to fall by 2030 to keep the repayment-to-income ratio in line with its long-run average when interest rates rise?

To develop our framework, we made some assumptions:

Bank of England official nominal interest rates will rise linearly to 4% by 2030 (i.e., just over 25bp of hikes per year). This resting point for interest rates reflects a combination of long-term real GDP growth of 2% plus 2% inflation.

The spread of mortgage rates over Bank Rate will remain close to its current 230bp.

Average nominal household income will grow at 2.5% per year, rising to 0.75% y-o-y thereafter.

Based on these assumptions, if our aim was to keep the repayment-to-income ratio static at its current long-run average level of 23.5%, then nominal house prices would need to remain broadly unchanged each year between 2017 and 2030. That equates to an average 1.75% annual decline for each of those years. In level terms, nominal house prices would be unchanged relative to this year by 2030; in real terms that equates to a 20% decline over the period.

In other words, just as lower interest rates were 'recapitalised' into higher house prices over the past few decades, a normalisation in interest rates could result in a ‘real term decapitalisation’ of the UK housing market over the coming years.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.