Capex cycle

In 2023, Asia’s economic slowdown affected not just exports, but also gross fixed capital formation, or capex, which languished. A cyclical downturn in manufacturing typically results in less investment into machinery and equipment as firms postpone investment decisions amid higher economic and profit uncertainty. Open and tech-driven countries such as South Korea and Singapore have experienced the steepest declines in capex growth in the region, while the domestic-demand driven economies such as India, the Philippines and Indonesia registered strong capex growth due to limited export spillovers and an increase in public capex.

Looking ahead, there is some light at the end of the tunnel from capex leading indicators. According to Nomura analysis, capex growth troughed in Q3 2023 at -6.5% year-over-year and has since drifted higher to 1.7% as of January 2024. Excluding China and Japan, we project Asia capex growth of 4.1% year-over-year for 2024. The increase can be attributed to an upturn in the goods cycle, which bodes well for machinery and equipment investment.

Beneath the headlines, we expect the following divergences in real capex growth:

- Residential construction investment is likely to slow given the fading of property demand and tighter funding for developers.

- Fixed investment growth in Korea is likely to lag that of other open economies as higher facility investment including machinery and equipment is offset by weakness in construction investment.

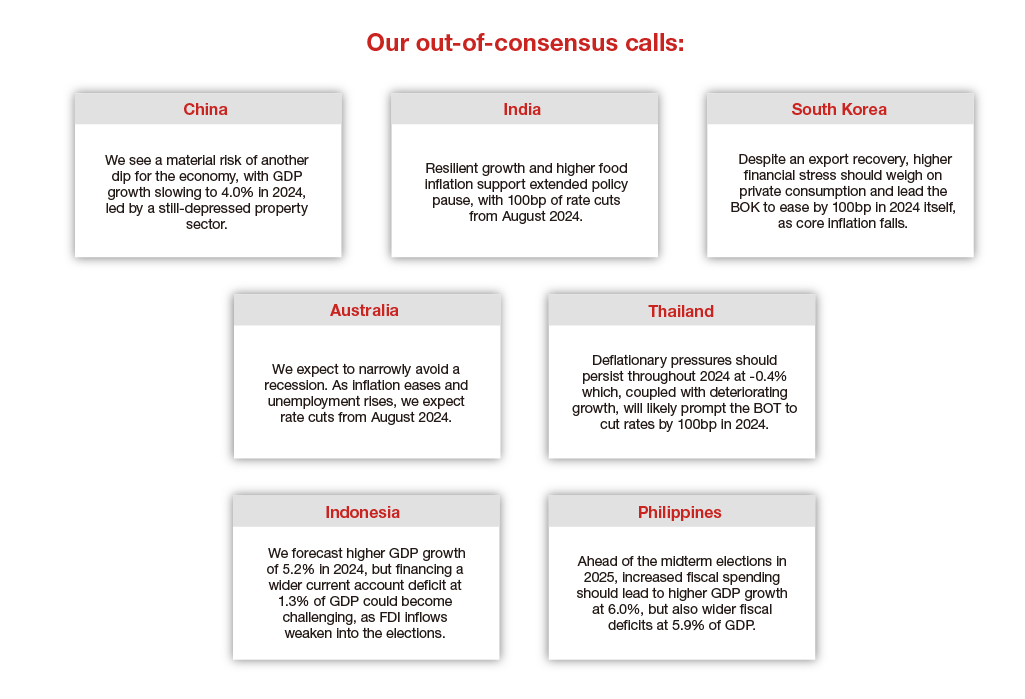

- We are most optimistic on the Philippines, expecting 12.1% year-over-year capex growth in 2024, versus 8.1% in 2023, as government infrastructure projects will likely benefit from a renewed push ahead of the mid-term elections in 2025.

- The budget delay in Thailand means a continued slump in government capital expenditure and a weak first half of 2024.

- In India, the election code of conduct precludes new public capex projects, which suggests a soft patch from March through June, but we still expect strong real fixed investment growth of 8% year-over-year in 2024.

- Finally, China will likely see lackluster real fixed asset investment growth with no signs of a turnaround in home sales and Beijing’s efforts to slow infrastructure investments in 12 heavily indebted regions.

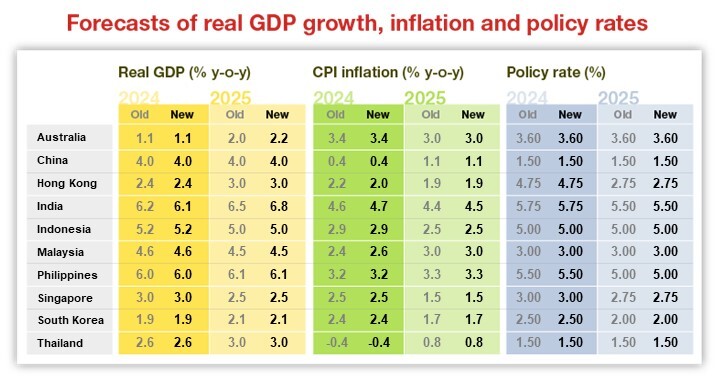

Despite a slowing China, we expect Asia ex-Japan’s GDP growth to rise to 3.9% year-over-year in 2024 from 3.6% in 2023. Alongside the ongoing rebound in exports, higher capex represents an additional tailwind to growth. We are above consensus on 2024 GDP growth in Singapore, Malaysia, the Philippines and Indonesia. Key risks to our view of a cyclical recovery is a resurgence in US inflation and US-China trade and tech tensions if Donald Trump is re-elected.

Capex trend

Beyond the cyclical capex outlook, longer-term trends might indicate an economy’s productivity growth. The investment rate, or nominal gross fixed capital formation as a share of nominal GDP, across most Asian economies has declined since 2010. While this might partly reflect the growing importance of services (which are less capital-intensive) in the economy, other factors are also at play: increased volatility, higher trade policy uncertainty, high debt in countries such as China, and balance sheet deleveraging in countries such as India.

South Korea, the Philippines, and India are among the Asian economies where investment rates increased between 2015 and 2023. The rise in Korea appears to have been driven by higher real estate investment, which doesn’t translate into economic productivity. However, the pickup in the Philippines and more recently in India has been driven by public infrastructure spending, which should boost potential growth if sustained. During the same period, the steepest falls in the investment rate took place in Malaysia, Hong Kong and Singapore. Alongside productivity-enhancing reforms, reversing the decline in investment is critical to lift potential growth in these economies.

We are most optimistic about the potential growth outlooks for India, the Philippines and Indonesia. All three have sound economic fundamentals and are stepping up public infrastructure spending, which should crowd in private investments. Favorable demographics, shifts in global value chains and commodity downstreaming are medium-term growth opportunities. For tech-driven Korea, rising artificial intelligence demand is a secular growth opportunity and firms are ramping up capex.

Bottomline: Watch out for a cyclical capex uptick in the open economies and a structural takeoff in the domestic-demand driven economies in Asia.

For more on our growth projections, read our full report.