Asia, currently the fastest-growing economic region, has always been a land of opportunity with significant scope for economic development. So the pertinent question is not "why Asia?", but "why Asia now?"

We believe a confluence of global push and regional pull factors are aligning, which should shine a positive light on Asia's medium-term outlook.

During the past year, US Federal Reserve tightening and US dollar appreciation have led investors to focus more on emerging market risk reduction, but as prospects of subdued global growth and Fed rate cuts come closer into view, we believe investors will look for new opportunities and place a higher premium on healthy economic fundamentals and sustainable growth.

Enter Asia.

During the global financial crisis and the pandemic, the continent by and large avoided large-scale quantitative easing and fiscal expansions, leaving the region in better stead in terms of fiscal sustainability, inflation challenges and health of the financial system.

Its balance of payments and foreign exchange reserve buffers are strong, and its governments are competing with one another to attract foreign investments by improving the domestic business climate, creating many new and exciting growth opportunities.

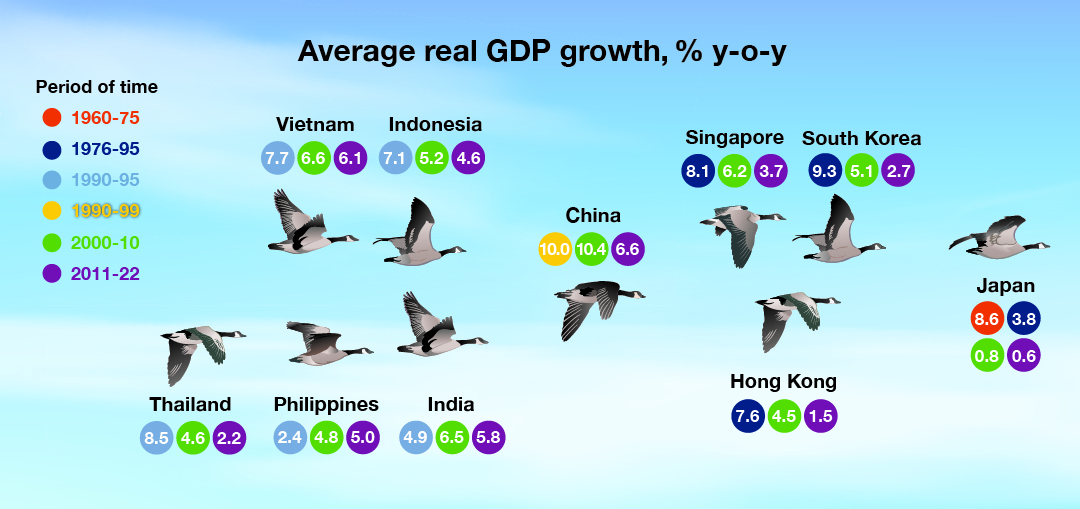

Asia's new flying geese are in the south

India and South-east Asia, in particular, are likely to be the fastest-growing economies this decade, as the "flying geese paradigm" is set to be in action once again.

This refers to Asia's hierarchy for economic development, where post-war Japan was the lead goose, but with its rapid development and rising costs, it relocated production and investment in the 1970s to the next flock of geese: South Korea, Taiwan, Hong Kong and Singapore.

Then in the early 1990s, as these economies began to rapidly catch up, they, along with Japan, helped set fly the next flock of geese, which included China.

However, China has now lost its low-cost comparative advantage which, along with geopolitical headwinds, has set the stage for Southeast Asia and India to become the region's new high-flying geese, unlocking their full growth potential.

To be fair, the shift in global supply chains is still at an early stage, but growing efforts by governments in these economies to accelerate infrastructure spending and execution should lead to higher foreign direct investment (FDI) inflows over the next three to five years.

The experience from North Asia shows that, once foreign trade and FDI reach critical mass, this also leads to stronger portfolio inflows.

Portfolio flows into Asia have historically originated mostly from the US and Europe, but with North Asia's high savings and a growing stock of financial wealth, coupled with our view that Southeast Asia and India are poised to become the region's new high-flying geese, we see scope for a significant rise in portfolio investments from the North to its own southern backyard.

India and Indonesia are also benefitting from other idiosyncratic growth drivers.

Digitalisation is enabling India to sustain its services-driven growth model. It is emerging as a popular destination for Global Capability Centres or offshore units of multinational corporations that provide support and high-end consulting in finance, IT and data analytics.

Indonesia is moving away from exports of unprocessed minerals towards downstreaming for metal ores, and this push towards more domestic value-add in metal exports is being followed by a greater push to develop an electric vehicle (EV) ecosystem.

In contrast to the south, North Asia has slower growth, but also new growth drivers.

Japan's economy is finally breaking out of its decades-long deflationary mindset. Alongside binding labour supply constraints, we think this will lead to a tectonic shift in the price-setting behaviour of Japanese companies, an improvement in their profit margins, and sustainable inflation.

The global artificial intelligence (AI) boom is creating opportunities for Taiwan and Korea, whose component manufacturers are the main suppliers of some crucial technologies and products for the hardware platforms needed for AI globally.

For the ageing economies in Asia, AI technology can also overcome slowing productivity and help to solve labour shortage problems.

China is a global leader in renewable energy technologies and supply chains, such as new-energy vehicles, lithium batteries and solar power generation.

In 2023, it is likely to lead in new solar installations, accounting for 43 per cent of global fittings.

EVs have now become an indispensable part of China's auto sector, with its share in overall auto production reaching nearly 30 per cent so far this year, the highest penetration globally.

Plans by industrialised countries to accelerate their carbon emission reduction should be a significant driver of China's renewable sector expansion.

Medium-term growth outperformance

We are under no illusion that China's economy is burdened with structural challenges and geopolitical headwinds, and that its medium-term growth will likely slow, but it will remain an economic juggernaut by size, contributing more than one-quarter of global growth.

Even with a slowing China, our medium-term (2024-2028) forecasts have real gross domestic product growth for Asia at 4.2 per cent year on year, outperforming other emerging markets -- Latin America (2.4 per cent), Central and Eastern Europe, Middle East and Africa -- or CEEMEA -- (3.2 per cent), and the US (1.8 per cent).

Asia offers a heterogeneous investment palette, yet investors have remained underinvested since the pandemic.

As market re-pricing shines a positive light on Asia, we expect this to change, with recognition that Asia is well on its way to reassuming the weight in the global economy that, on the basis of its population, it held in the 18th century.

Faster growth should attract more capital inflows, lift business confidence and drive domestic investment.

Right now, there is global uncertainty and gloom, but once the dust settles, we believe global investors will soon start to appreciate Asia's superior risk-adjusted returns.

The stage is set for Asia's medium-term outperformance.

This article was first published in Singapore’s Business Times on June 6, 2023 to coincide with the start of Nomura Investment Forum Asia.