Growth in most Asian economies should outperform their Western counterparts in 2024, driven by a semiconductor-led export tailwind and steady domestic demand. These drivers should facilitate a soft landing

for Asia, which is when real GDP growth falls gently following a policy tightening cycle - in contrast to our forecasts for mild recessions in US and Europe.

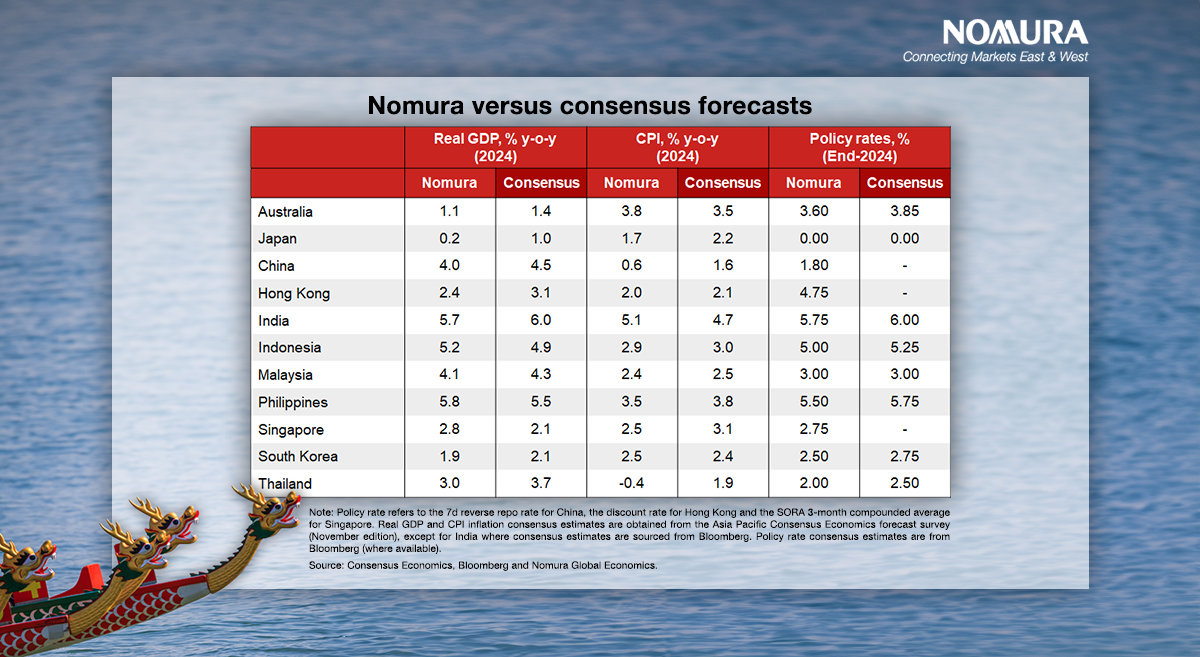

Asia is looking to enter its sweet spot in early 2024 due to the chip cycle recovery, although the region could see a more challenging second half of the year as the US recession unfolds, according to Nomura’s analysis. Inflation divergence

will be an important theme. Monetary policy will likely pause through Q1 to give way to rate cuts starting in Q2. Over the medium term, we see India, Indonesia and the Philippines as Asia’s rising stars.

These are the key themes as we head into 2024.

- A semiconductor-led export tailwind. Asia’s export growth downturn bottomed out in mid-2023. Semiconductors have since driven the turnaround. Nomura’s tech analysts expect global semiconductor shipments to increase by 17.8% year-on-year in 2024 after a 9.4% drag this year, powered by AI chips, the end of the inventory correction and higher memory prices. Export growth will likely be frontloaded in Q1 and parts of Q2, with softer momentum in the second half of the year.

- Asian economies should soft land. Despite the weak global backdrop, Asia’s growth should outperform that of developed markets due to the export tailwind and stable domestic demand. Asia’s labor market remains healthy, with ongoing job gains and steady real income growth. There is also consumption support in Japan, Thailand and Indonesia. Even in economies where rate hikes will likely bite, such as in Korea and Australia, overall growth should slow but not slump.

- A sweet spot in H1, followed by a choppier H2. We see Asia entering its sweet spot in the first half of 2024 due to an upturn in the export cycle and still-positive US growth. The second half of the year could become choppier as export growth momentum begins to roll over, US recession fears increase economic uncertainty, and US-China political tensions heat up ahead of the US presidential elections.

- China’s real turning point. Though Beijing has announced a multitude of easing measures, there is a risk of another economic dip by spring 2024. New home sales remain weak and we reckon that after spring 2024, Beijing could fund major property developers to deliver unfinished pre-sold homes, marking a real turning point for China’s property sector. Structurally, China’s economy faces challenges from demographics, debt and geopolitics, which we expect to slow its GDP growth to an average 3.9% over 2024 to 2028.

- The economics of politics. It’s a busy political calendar in the first half of 2024 as several Asian economies head into elections. The election results could have medium-term implications for country-specific economic outlooks, such as that of Indonesia, India, the Philippines and Korea. Interestingly, despite elections, and in a sign of prudent policymaking, we don’t expect any fiscal populism.

- Brace for inflation divergence. On aggregate, we expect consumer inflation to moderate across all Asian economies in 2024. We also see inflation divergence as an important theme, depending on labor market tightness, the stage of the business cycle, the size of fiscal subsidies and exposure to food and energy shocks. We see inflation on the higher end for Australia, Singapore, the Philippines and South Korea. Meanwhile, we see headline deflation persisting in Thailand and underlying inflation remaining low in Indonesia.

- Monetary policy easing is next, but we expect Asia to ease by less than the Fed. The rate hiking cycle is likely over. We expect an extended pause until Q1 followed by rate cuts starting in Q2, led by Thailand and Indonesia. In Japan, we expect the central bank to end negative interest rate policy in January 2024, and scrap yield curve control in Q2. Since Asian central banks hiked by less than the Fed, the region should also see less monetary policy easing.

- It’s still Asia’s time to shine. Beyond the cyclical view, we believe that Asia has stronger economic fundamentals, pro-reform governments and many growth opportunities, such as shifting supply chains and public infrastructure spending in India and Southeast Asia, green and electric vehicle opportunities in Korea and China, and downstreaming in Indonesia. Asia is well-placed to attract large capital inflows. We see India, Indonesia and the Philippines as the fastest growing economies this decade.

For more on our 2024 macroeconomic outlook, read our full report.

Ting Lu, Euben Paracuelles, Jeong Woo Park and Kyohei Morita also contributed to this report.

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.